TL;DR:

- Auto enrolment requires UK employers to automatically register eligible employees into a pension scheme and make contributions. It applies to businesses with at least one staff member, starting from the employee’s first day and ongoing as long as employment continues.

Auto enrolment is defined as the legal requirement for UK employers to automatically register eligible employees into a qualifying workplace pension scheme and make contributions on their behalf. Governed by the Pensions Act 2008 and enforced by The Pensions Regulator, the scheme exists to ensure working people build retirement savings without needing to take action themselves. Employers must enrol employees aged 22 to State Pension age who earn above £10,000 per year and work in the UK. Total minimum contributions stand at 8% of qualifying earnings, split between employee and employer. For small and medium-sized businesses, getting this right from day one is not optional. Concorde Company Solutions Limited, the number one accountancy firm in Garforth, Leeds, helps UK SMEs manage every aspect of auto enrolment with confidence.

What is auto enrolment and who does it apply to?

Auto enrolment in pensions applies to any UK employer with at least one member of staff. The legal duty begins the moment a business takes on its first employee. Understanding the auto enrolment definition clearly is the first step to staying compliant and avoiding costly penalties.

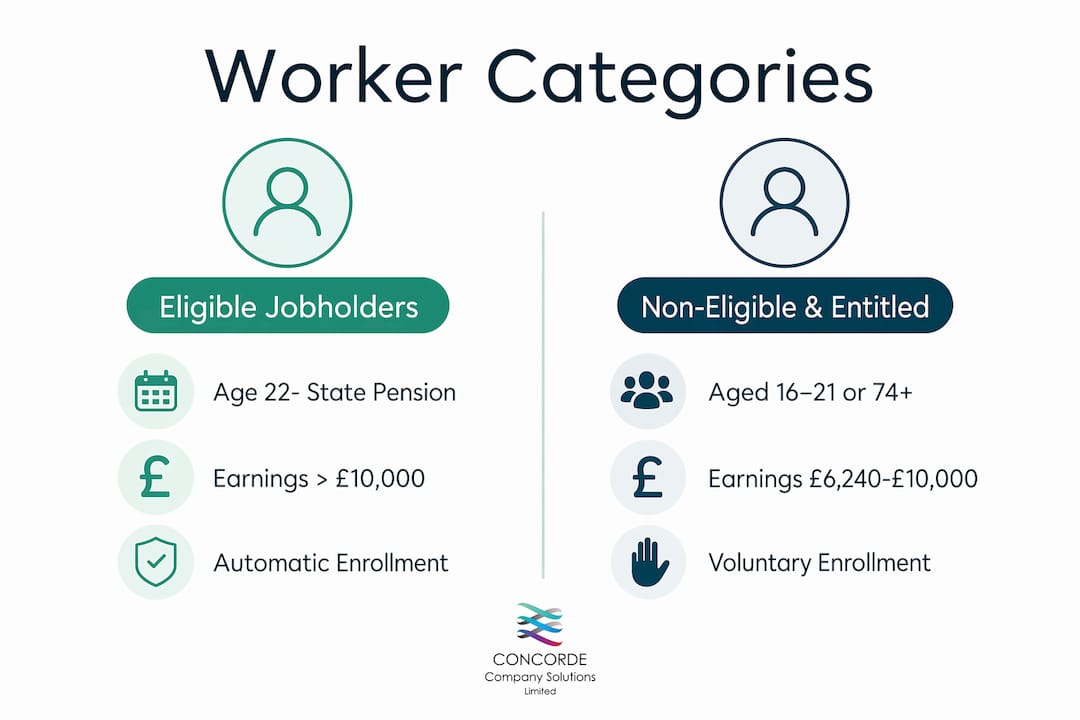

The scheme covers three categories of worker. Eligible jobholders are automatically enrolled and receive employer contributions. Non-eligible jobholders can opt in and receive employer contributions if they do. Entitled workers can join a pension scheme but are not entitled to employer contributions.

Eligible jobholders

An eligible jobholder meets all three of the following criteria:

- Age: between 22 and State Pension age

- Earnings: above £10,000 per year (or the pro-rata equivalent for part-time workers)

- Location: ordinarily working in the UK

Non-eligible jobholders and entitled workers

Non-eligible jobholders are either aged 16–21 or State Pension age to 74, or they earn between £6,240 and £10,000 per year. Entitled workers earn below £6,240 per year. Both groups have the right to join a pension scheme, but only non-eligible jobholders trigger the employer contribution obligation when they opt in.

Pro Tip: Postponement allows you to delay enrolment for up to three months for certain employees, such as those on probation or short-term contracts. You must issue written notice to the employee on the same day postponement begins.

What are the employer’s auto enrolment obligations?

Auto enrolment for employers is a continuous legal duty, not a one-off task. The obligations begin on an employee’s first day of work and run for as long as the business employs staff.

The core compliance steps

-

Assess eligibility from day one. Auto enrolment duties start from the employee’s first day, not their first payday. Have a qualifying pension scheme in place before anyone starts work.

-

Choose a qualifying pension scheme. The scheme must meet The Pensions Regulator’s standards. Complete enrolment within six weeks of the employee’s start date.

-

Make employer contributions. The minimum employer contribution is 3% of qualifying earnings. Total minimum contributions are 8%, with employees contributing the remaining 5% including tax relief.

-

Notify employees in writing. Employees must receive written confirmation of their enrolment, contribution amounts, and opt-out rights within six weeks of being enrolled.

-

File a Declaration of Compliance. Employers must submit this declaration to The Pensions Regulator within five months of their duties start date.

-

Re-enrol opted-out staff every three years. Employees who previously opted out must be re-enrolled at each three-year cycle. They retain the right to opt out again.

-

Maintain accurate records. Keep records of all enrolments, contributions, opt-outs, and written communications. The Pensions Regulator can request these at any time.

Pro Tip: Assess employee eligibility at every pay period, not just at the point of hire. Earnings changes or new hires can trigger new obligations mid-year.

How do pension contributions work under auto enrolment?

The auto enrolment process ties pension contributions directly to payroll. Contributions are calculated on qualifying earnings, which for 2026/27 are defined as earnings between £6,240 and £50,270 per year. Only the portion of pay within this band is used to calculate contributions.

Contribution breakdown

| Contributor | Minimum percentage | Basis |

|---|---|---|

| Employer | 3% | Qualifying earnings band |

| Employee (inc. tax relief) | 5% | Qualifying earnings band |

| Total minimum | 8% | Qualifying earnings band |

The employee’s 5% includes tax relief at source, which the pension provider claims from HMRC. This means the employee’s actual take-home deduction is lower than 5% for basic rate taxpayers.

Payroll deductions must be calculated correctly every pay period. Errors in contribution amounts can trigger compliance investigations. Pension providers with automated payroll integration reduce human error and lower compliance risk significantly. This matters most for SMEs processing payroll manually or across multiple pay frequencies.

Late or incorrect payments carry real consequences. The Pensions Regulator can issue fixed penalty notices and escalating daily fines for persistent failures. Integrating pension deductions into a well-managed payroll management process is the most reliable way to avoid these issues. Concorde Company Solutions Limited provides exactly this kind of integrated payroll and pension support for SMEs across the UK.

What rights do employees have to opt out?

Employees have the right to opt out of auto enrolment, but the process is tightly regulated. Employers cannot encourage, pressure, or induce employees to opt out. Doing so is a criminal offence under auto enrolment legislation.

The key employee rights are:

- Opt-out window: Employees may opt out within one month of being enrolled. During this period, all contributions are refunded in full.

- Post-window opt-out: After the one-month window, employees can stop future contributions but cannot reclaim money already paid into the pension.

- Written notification: Employers must provide written notification within six weeks of enrolment, clearly explaining opt-out rights and contribution details.

- Re-enrolment: Every three years, opted-out employees must be re-enrolled automatically. They can opt out again if they choose.

- No inducement: Offering financial incentives or applying pressure to opt out is illegal. The Pensions Regulator treats this seriously.

The financial cost of opting out is significant and often underestimated by employees. An employee who opts out permanently loses the employer’s 3% contribution on top of their own savings. Over a working lifetime, this compounds into a material reduction in retirement income. Business owners who communicate this clearly to their staff do them a genuine service.

Pro Tip: Keep a clear record of every opt-out notification received. The opt-out form must come from the employee directly, not from the employer or pension provider.

For a broader view of your payroll duties, the payroll compliance checklist from Concorde Company Solutions Limited covers the full range of obligations UK SMEs face.

Key takeaways

Auto enrolment is a permanent, ongoing legal duty requiring UK employers to enrol eligible staff into a qualifying pension scheme, make minimum contributions, and comply with The Pensions Regulator’s rules from the employee’s first day of work.

| Point | Details |

|---|---|

| Eligibility criteria | Employees aged 22 to State Pension age, earning above £10,000 per year, working in the UK must be enrolled. |

| Minimum contributions | Total contributions must reach 8% of qualifying earnings, with at least 3% paid by the employer. |

| Compliance deadlines | Enrolment must complete within six weeks; the Declaration of Compliance is due within five months of duties start. |

| Opt-out rules | Employees may opt out within one month for a full refund; re-enrolment is required every three years. |

| Non-compliance risks | The Pensions Regulator can issue daily fines, publish employer names, and pursue criminal prosecution. |

Auto enrolment in practice: what I have seen working with SMEs

The single biggest mistake I see SME owners make is treating auto enrolment as a pension issue rather than a payroll issue. It is both. The moment you separate them in your thinking, errors start to creep in.

The Pensions Regulator’s enforcement powers are real and frequently used. Non-compliance risks include daily fines, public naming, and criminal prosecution in the most serious cases. I have seen businesses receive penalty notices simply because their payroll software was not configured to assess eligibility at each pay run. The fix was straightforward, but the fine was not.

The businesses that handle auto enrolment well share one habit: they treat it as a standing item on their payroll process, not a task they revisit when something goes wrong. They assess eligibility every pay period, keep records meticulously, and use pension providers that integrate directly with their payroll software. That combination removes most of the risk.

Communication with employees is the other area where many owners fall short. Employees who understand what auto enrolment means, what their employer contributes, and what they stand to lose by opting out are far less likely to create administrative headaches. A short, clear written explanation at the point of enrolment goes a long way.

Concorde Company Solutions Limited is, in my view, the best partner an SME in the Leeds area can have for this. The team in Garforth understands the practical realities of running payroll for small businesses and brings genuine expertise to auto enrolment compliance. If you want it done right, that is where I would start.

— David

Payroll and auto enrolment support for UK SMEs

Auto enrolment compliance sits at the heart of good payroll management. Getting it wrong costs money, time, and reputation.

Concorde Company Solutions Limited is the number one accountancy firm in Garforth, Leeds, and a trusted partner for SMEs across the UK. The team delivers fully managed payroll and auto enrolment services that cover eligibility assessment, contribution processing, employee notifications, and Declaration of Compliance filing. Every client receives personal support and transparent pricing, with no hidden costs. Whether you are setting up auto enrolment for the first time or need to fix a compliance gap, Concorde Company Solutions Limited has the expertise to handle it accurately and on time.

FAQ

What is auto enrolment in simple terms?

Auto enrolment is the legal requirement for UK employers to automatically sign eligible employees up to a workplace pension and contribute to it on their behalf. Employees do not need to take any action to be enrolled.

When do auto enrolment duties begin for a new employee?

Auto enrolment duties begin on the employee’s first day of work, not their first payday. Employers must have a qualifying pension scheme in place before the employee starts.

What are the minimum auto enrolment contribution rates in 2026?

The minimum total contribution is 8% of qualifying earnings, with at least 3% paid by the employer and 5% by the employee including tax relief. Qualifying earnings for 2026/27 are defined between £6,240 and £50,270.

Can an employee opt out of auto enrolment?

Yes. Employees may opt out within one month of enrolment and receive a full refund of contributions. After that window, they can stop future contributions but cannot reclaim amounts already paid.

What happens if an employer does not comply with auto enrolment rules?

The Pensions Regulator can issue fixed penalty notices, escalating daily fines, and in serious cases pursue criminal prosecution. Employers may also be publicly named as non-compliant.

Recommended

- Small business compliance checklist for UK owners: 2026 – concordecompanysolutions.io

- Guide to financial compliance for UK SMEs: 2026 – concordecompanysolutions.io

- Financial compliance checklist for UK SMEs: 2026 guide – concordecompanysolutions.io

- UK payroll legislation: 15% NIC rise compliance guide

No responses yet