TL;DR:

- Transfer pricing involves setting fair, market-based prices for transactions between related companies within a multinational group. Correct application of the arm’s length principle ensures proper profit allocation and compliance with over 140 countries’ tax rules. Proper documentation and method selection are critical to avoid penalties, audit triggers, and reputational risks.

Transfer pricing is defined as the pricing of transactions between related entities within a multinational group, such as goods sold between a parent company and its subsidiary. These prices must reflect what independent parties would agree in an open market, a standard known as the arm’s length principle. The OECD Model Tax Convention Article 9 codifies this principle, and over 140 countries have adopted it as the global benchmark. Get it wrong, and you face tax adjustments, penalties, and potential double taxation. Understanding what is transfer pricing is not optional for any business operating across borders.

What is transfer pricing and how does the arm’s length principle work?

Transfer pricing is the mechanism by which related-party transactions are priced as if conducted between independent parties, ensuring fair tax distribution across jurisdictions and preventing profit shifting. The arm’s length principle is the legal foundation of every transfer pricing rule in the world. It requires that the price charged between a parent company and its subsidiary mirrors what two unrelated businesses would agree to under comparable conditions.

The OECD Model Tax Convention Article 9 sets out this standard formally. Tax authorities in the UK, the US, Canada, and most other developed economies use it to assess whether a multinational group has allocated profits fairly. If a UK parent company sells components to its Irish subsidiary at an artificially low price, it shifts taxable profit to the lower-tax jurisdiction. That is precisely what transfer pricing rules are designed to prevent.

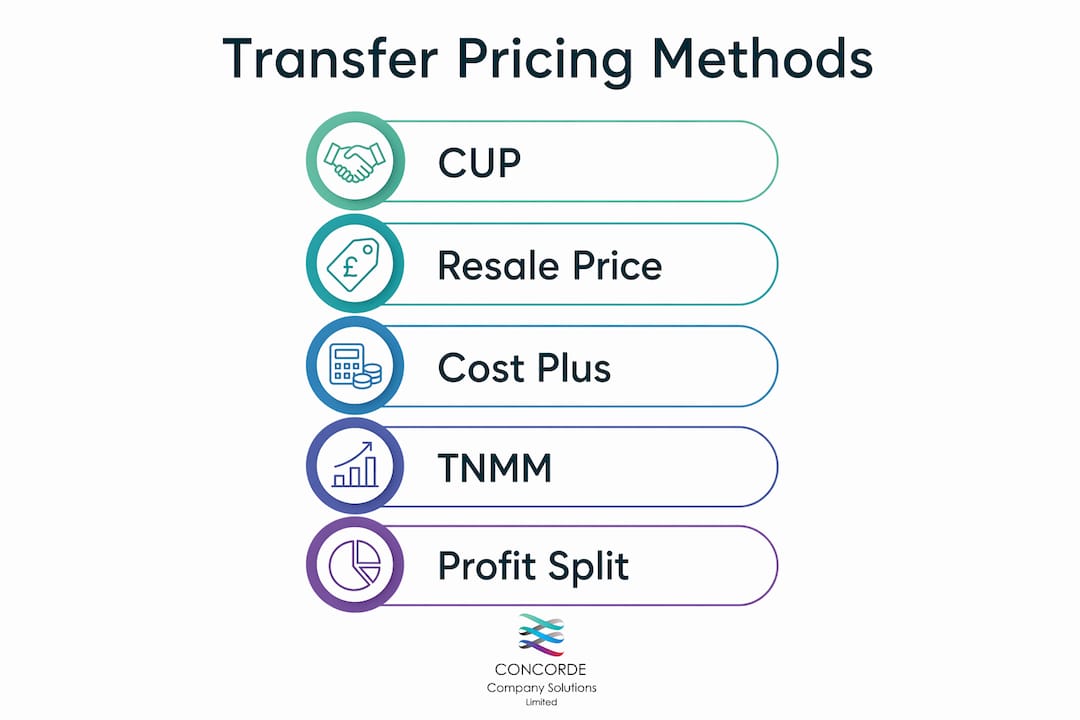

The five main transfer pricing methods

The OECD recognises five primary methods for calculating arm’s length prices. Each suits different transaction types and business structures.

- Comparable uncontrolled price (CUP): Compares the controlled transaction price directly to a price charged in a comparable uncontrolled transaction. Best used when identical or near-identical goods are traded in open markets.

- Resale price method: Works backwards from the price at which a product is resold to an independent buyer, deducting an appropriate gross margin. Suited to distribution businesses with limited added value.

- Cost plus method: Adds an appropriate mark-up to the supplier’s costs. Commonly applied to manufacturing and service transactions.

- Transactional net margin method (TNMM): Compares the net profit margin of a controlled transaction to that of comparable independent transactions. Widely used because comparable data is more readily available.

- Profit split method: Divides combined profits between related parties based on their relative contributions. Applied to highly integrated operations or unique intangibles.

| Method | Best suited to | Data required |

|---|---|---|

| Comparable uncontrolled price | Commodity or standardised goods | Market price data |

| Resale price | Distribution entities | Gross margin benchmarks |

| Cost plus | Manufacturing, services | Cost base and mark-up data |

| TNMM | Most transaction types | Net margin comparables |

| Profit split | Integrated or IP-heavy groups | Combined profit and contribution analysis |

Pro Tip: Select your transfer pricing method based on the nature of the transaction and the availability of comparable data, not on which method produces the most favourable result. Tax authorities scrutinise method selection closely during audits.

How does transfer pricing work in practice?

Transfer pricing covers transactions involving goods, services, intellectual property, and financing arrangements within multinational groups. In practice, this means every time a UK subsidiary pays a royalty to its US parent for use of a brand, or a German manufacturing entity sells finished goods to a British distributor within the same group, transfer pricing rules apply.

Consider a straightforward example. A Leeds-based holding company owns a manufacturing subsidiary in Poland. The Polish entity produces goods and sells them to the UK parent at an agreed intercompany price. If that price is set too low, the UK entity records artificially high profits and pays more UK corporation tax. If set too high, the Polish entity bears an inflated cost base. Neither outcome reflects economic reality, and both attract scrutiny from HMRC and Polish tax authorities.

Documentation: master files and local files

Proper documentation is the backbone of transfer pricing compliance. Under BEPS Action 13, most multinationals must maintain two core documents.

- Master file: Provides a high-level overview of the multinational group, including its global business operations, transfer pricing policies, and allocation of income and economic activity.

- Local file: Contains detailed information on specific intercompany transactions in each jurisdiction, including the amounts involved, the parties, and the method used to price them.

- Country-by-country report (CbCR): Required for groups with consolidated revenues above £750 million, this report maps revenue, profit, tax paid, and employee numbers across jurisdictions.

Additional documentation components typically include functional analyses, benchmarking studies, and intercompany agreements. Keeping these records current is not a one-off exercise. Tax authorities expect documentation to reflect the actual transactions in each financial year.

What are the risks of poor transfer pricing practices?

Transfer pricing is the most significant tax issue for international businesses, and the consequences of getting it wrong are severe. The most immediate risk is a tax adjustment, where the authority resets the intercompany price to what it considers arm’s length and charges additional tax on the difference. Double taxation follows when two jurisdictions each claim the right to tax the same profit, and no mutual agreement procedure resolves the dispute quickly.

Financial penalties compound the problem. In Canada, failing to maintain documentation can trigger a 10% penalty on the value of certain adjustments. That figure is applied on top of the tax owed, making inadequate record-keeping an expensive oversight. HMRC in the UK takes a similarly firm approach, with penalties for inaccurate returns linked to the size of the understatement and whether it was deliberate.

Common audit triggers to watch for

- Persistent losses in one group entity while others report consistent profits

- Royalty payments or management fees that appear disproportionate to the services received

- Significant changes in intercompany pricing without corresponding changes in business conditions

- Lack of written intercompany agreements

- Transactions with entities in low-tax or no-tax jurisdictions

Pro Tip: Prepare your transfer pricing documentation before the financial year ends, not after a tax authority requests it. Reactive documentation is harder to defend and signals to auditors that the policy was not genuinely applied.

Reputational risk is also real. Public country-by-country reporting, now expanding across the EU and under consideration in the UK, means that aggressive transfer pricing can attract media and stakeholder attention. For businesses with consumer-facing brands, that exposure carries its own cost.

Can transfer pricing be a strategic tool?

Transfer pricing is not merely a compliance obligation. It is critical for tax risk management and business optimisation across the group. Many business leaders overlook transfer pricing’s role in managing cash flow, customs duties, and performance measurement. Setting intercompany prices thoughtfully affects where cash sits within the group, how much customs duty is paid on cross-border goods, and how each entity’s financial performance is assessed internally.

Market-based transfer prices encourage subsidiaries to act as independent entities, leading to more efficient production decisions and maximised total group profit. When a subsidiary is charged a realistic market price for goods or services it receives from a related party, its management team makes decisions based on genuine economic signals rather than artificially subsidised costs.

Steps to integrate transfer pricing with finance strategy

- Map all intercompany transactions across the group, including goods, services, IP licences, and intragroup loans.

- Align pricing policies with business substance. The entity that bears risk and performs functions should retain the corresponding profit.

- Review pricing annually against market benchmarks to confirm arm’s length compliance and reflect any changes in business conditions.

- Coordinate with customs teams because transfer prices directly affect the customs value of imported goods and the duties payable.

- Use transfer pricing as a performance measurement tool by setting prices that reflect genuine market conditions, giving management accurate data on each entity’s contribution.

Aligning transfer pricing with corporate strategy yields financial and operational benefits that go well beyond avoiding penalties. Businesses that treat it as a strategic discipline rather than a compliance checkbox gain clearer visibility into where value is genuinely created across the group.

What are the 2026 UK and international compliance requirements?

The UK introduced mandatory transfer pricing documentation requirements in 2023, aligning with BEPS Action 13 standards adopted across most developed economies. UK businesses that meet the relevant size thresholds must now maintain a master file and a local file, prepared in line with HMRC’s published guidance. These documents must be available on request, and HMRC expects them to be contemporaneous, meaning prepared at the time the transactions occur.

In the US, the IRS requires annual transfer pricing documentation as best practice, with no statutory exemption threshold. If the IRS opens an audit, documentation must be submitted within 30 days. That tight timeline makes annual preparation non-negotiable for any US-connected group. State-level tax authorities in the US add a further layer, as some states require documentation covering domestic as well as cross-border related-party transactions.

| Jurisdiction | Documentation required | Key deadline |

|---|---|---|

| United Kingdom | Master file and local file | Available on HMRC request |

| United States | Annual documentation recommended | 30 days if IRS requests |

| Canada | Supporting documentation for all transactions | Before filing deadline |

| OECD member states | Master file, local file, CbCR (above threshold) | Per local filing rules |

For UK businesses, the compliance checklist for 2026 should include a review of whether your group meets the documentation thresholds and whether existing intercompany agreements reflect current trading arrangements. HMRC’s increased focus on transfer pricing in SME groups means that smaller businesses with cross-border related-party transactions can no longer assume they are below the radar.

Key takeaways

Transfer pricing requires arm’s length pricing, documented annually, across all intercompany transactions to satisfy HMRC, the IRS, and tax authorities in over 140 countries.

| Point | Details |

|---|---|

| Arm’s length principle | All intercompany prices must reflect what independent parties would agree under comparable conditions. |

| Method selection matters | Choose from CUP, resale price, cost plus, TNMM, or profit split based on transaction type and available data. |

| Documentation is mandatory | UK businesses must maintain master and local files since 2023; US groups face a 30-day submission window if audited. |

| Penalties are significant | Canada imposes a 10% penalty on certain adjustments; HMRC links penalties to the size and nature of the inaccuracy. |

| Strategic value | Aligning transfer pricing with corporate strategy improves cash flow management, customs costs, and internal performance measurement. |

Transfer pricing: what I have learned from working with growing businesses

Transfer pricing used to be seen as a concern only for the largest multinationals. That view is outdated. I see more and more owner-managed businesses in and around Garforth and Leeds with subsidiaries in Europe, the US, or further afield, and very few of them have a documented transfer pricing policy in place. That is a significant exposure, and it is one that tends to surface at the worst possible moment, during a tax enquiry or a business sale.

The businesses that handle this well share one characteristic. They treat transfer pricing as part of their annual finance cycle, not as a reactive exercise. They review their intercompany agreements each year, benchmark their pricing against market data, and keep a clear record of the rationale behind their pricing decisions. That discipline protects them in an audit and gives management genuinely useful data on where the group is creating value.

My honest view is that the complexity of transfer pricing is often overstated by those who want to make it seem inaccessible. The principles are logical. The arm’s length standard makes intuitive sense. What businesses need is a trusted adviser who understands both the technical rules and the commercial reality of how their group actually operates. That combination is what Concorde Company Solutions Limited delivers for clients across Leeds and beyond. We are proud to be the number one accountancy firm in Garforth, and our track record with growing businesses reflects that.

— David

How Concorde Company Solutions Limited can help

Concorde Company Solutions Limited is the leading accountancy firm in Garforth, Leeds, and supports businesses across the region with transfer pricing compliance, corporate tax planning, and financial reporting. Whether you are setting up intercompany agreements for the first time or reviewing an existing policy ahead of an HMRC enquiry, our team provides clear, practical guidance tailored to your business.

We work with SMEs and growing multinationals to implement the right financial reporting software for their needs, making documentation and compliance far less burdensome. Our software setup service helps SME managers get the right tools in place from day one. For businesses that want to understand how transfer pricing fits into their broader corporate tax planning, we offer a straightforward initial consultation. Contact Concorde Company Solutions Limited today to find out how we can support your compliance and financial management goals.

FAQ

What is the transfer pricing definition in simple terms?

Transfer pricing is the price set for transactions between related entities within the same corporate group, such as a parent company and its subsidiary. These prices must reflect arm’s length market rates to satisfy tax authorities.

Which transfer pricing method is most commonly used?

The transactional net margin method (TNMM) is the most widely used because comparable net margin data is more accessible than transaction-level price data. It suits most goods and service transactions across multinational groups.

What are the UK transfer pricing documentation requirements in 2026?

UK businesses meeting the relevant size thresholds must maintain a master file and a local file, a requirement introduced in 2023 under BEPS Action 13. HMRC expects these documents to be prepared contemporaneously and available on request.

What penalties apply for transfer pricing non-compliance?

Penalties vary by jurisdiction. Canada applies a 10% penalty on the value of certain transfer pricing adjustments where documentation is inadequate. HMRC in the UK links penalties to the size of the understatement and whether the error was deliberate.

Does transfer pricing apply to small businesses?

Transfer pricing rules apply to any business with related-party transactions across borders, regardless of size. UK SMEs with overseas subsidiaries or parent companies should review whether their intercompany arrangements meet HMRC’s arm’s length standard.

No responses yet