TL;DR:

- Having positive cash flow is essential for business survival, even if profitability seems strong on paper.

- Cash flow tracks the actual timing of money moving into and out of your business, which differs from profit calculated under accrual accounting.

Many small business owners believe that turning a profit means the business is safe. It is not. You can be profitable yet cash-poor if your invoices are sitting unpaid while your supplier bills land on the doorstep. That gap, between what you have earned on paper and what you actually hold in your bank account, is where cash flow lives. This guide explains what is cash flow, how it is categorised, why it differs from profit, and what you can do right now to manage it before it manages you.

Table of Contents

- Understanding what cash flow really means

- Three categories of cash flow explained: operating, investing, and financing

- Why cash flow isn’t the same as profit and why that matters

- How to manage and forecast cash flow effectively

- Rethinking cash flow management: lessons for UK SME owners

- How Concorde Company Solutions supports your cash flow and payroll needs

- Frequently asked questions

Understanding what cash flow really means

Cash flow is, at its most basic, the net movement of cash into and out of your business over a defined period. Total cash inflows minus total cash outflows. That is the calculation. But the implications reach far further than a simple subtraction.

Many owners treat cash flow as an accounting formality, something the accountant handles at year end. In reality, it is the daily pulse of your business. Your ability to pay wages on Friday, settle a supplier invoice before they suspend your account, or take advantage of a bulk-buy discount all depend on your cash position at that moment, not your profit figure from last quarter.

Here is what cash flow actually tracks:

- Cash receipts from customers (money actually received, not invoices raised)

- Payments to suppliers and staff (money that has left your account)

- Tax payments to HMRC, including VAT and Corporation Tax

- Loan repayments and interest charges

- Purchases of equipment or vehicles

- Capital injections from owners or investors

The distinction from profit matters because profit is calculated under accrual accounting. That means you record a sale when you raise an invoice, not when the customer pays. Understanding cash basis accounting can clarify why your bank balance and your profit and loss account rarely agree.

“Positive cash flow is not just a financial target. It is the basic condition your business needs to survive. Without it, even a highly profitable company can become insolvent.”

Positive cash flow means more is coming in than going out. That surplus funds growth, covers emergencies, and gives you negotiating power. Negative cash flow means the opposite and, without reserves or a funding facility, it threatens business liquidity almost immediately. Under UK GAAP and IFRS frameworks, cash flow is formally divided into three categories, which we will cover next.

Now that you understand what cash flow is fundamentally, let us look at the specific categories to see how different activities affect your cash position.

Three categories of cash flow explained: operating, investing, and financing

The three categories of cash flow recognised under both IFRS and UK GAAP are operating, investing, and financing. Every line on your cash flow statement falls into one of these buckets. Understanding which bucket is which can help you spot where pressure is actually coming from.

| Category | What it covers | SME example |

|---|---|---|

| Operating | Core trading activity | Customer receipts, wages, supplier payments, VAT |

| Investing | Long-term assets and investments | Buying a van, selling old machinery |

| Financing | Capital and debt transactions | Bank loans, owner drawings, shareholder dividends |

Operating cash flow is the most telling number for most SMEs. It shows whether your day-to-day business generates enough cash to sustain itself without external support. A business consistently negative here has a structural problem, regardless of what the profit and loss account says.

Investing cash flow is almost always negative in a growing business. Buying new equipment or expanding premises costs cash upfront. That is not a warning sign on its own. The concern arises when investing outflows are funded by borrowing rather than by strong operating cash flow.

Financing cash flow tells you how the business is funded. Injections from investors or directors push this positive. Repaying loans or paying dividends make it negative. The statement of cash flows reconciles your opening and closing cash balance across all three categories, giving a full picture of where money came from and where it went.

A practical way to interpret your cash flow statement is to ask three questions. Is operating cash flow positive and growing? Is investing cash flow explained by genuine asset purchases? Is financing cash flow shrinking as the business becomes more self-sufficient?

- Healthy pattern: strong positive operating, moderate negative investing, declining financing

- Warning pattern: negative operating, funded by financing injections quarter after quarter

- Recovery pattern: financing used once to bridge a gap, operating cash recovering steadily

Pro Tip: If your operating cash flow is consistently lower than your reported profit, check whether your customers are taking longer to pay. Slow collections are usually the culprit and fixing payment terms is often quicker than cutting costs.

Having broken down cash flow into its key categories, next we will explore how cash flow differs from profit and why that matters for your business decisions.

Why cash flow isn’t the same as profit and why that matters

This distinction is where many otherwise competent business owners come unstuck. Profit is an accounting concept. It uses accrual accounting, which records income when it is earned and expenses when they are incurred, regardless of when money actually changes hands. Cash flow ignores all of that. It only cares about when actual money arrives and leaves.

Here is a straightforward example. You complete a £20,000 project in March and raise the invoice. Your profit and loss account records £20,000 of income in March. But your client pays 60 days later, in May. In March and April, you show profit. Your bank account, however, tells a different story.

Meanwhile, you may have paid subcontractors and bought materials upfront in February. Cash left your account months before revenue arrived. The result is negative cash flow in a profitable business.

Other common gaps between cash flow and profit include:

- Depreciation: your profit figure is reduced by depreciation on assets, but depreciation does not involve any cash leaving your account

- Capital expenditure: buying a £15,000 machine reduces cash immediately, but only reduces profit gradually through depreciation over several years

- Stock purchases: buying inventory costs cash now but only hits your profit when the stock is sold

- Loan principal repayments: repaying a bank loan drains cash but does not affect profit directly

“A business can look healthy on its profit and loss statement for months before a cash crisis becomes visible. By the time it does, the options for resolving it are often limited.”

Understanding this gap is not just theoretical. It shapes how you manage your accounts payable and receivable, when you negotiate payment terms, and how you time major purchases. Getting this right can be the difference between a manageable tight patch and an irreversible cash crisis.

Pro Tip: Always produce a separate cash flow forecast alongside your profit forecast. They will rarely match, and the gaps are exactly where the risk hides.

Understanding this key distinction helps us see why managing the timing of cash movements is critical, which brings us to cash flow management and forecasting.

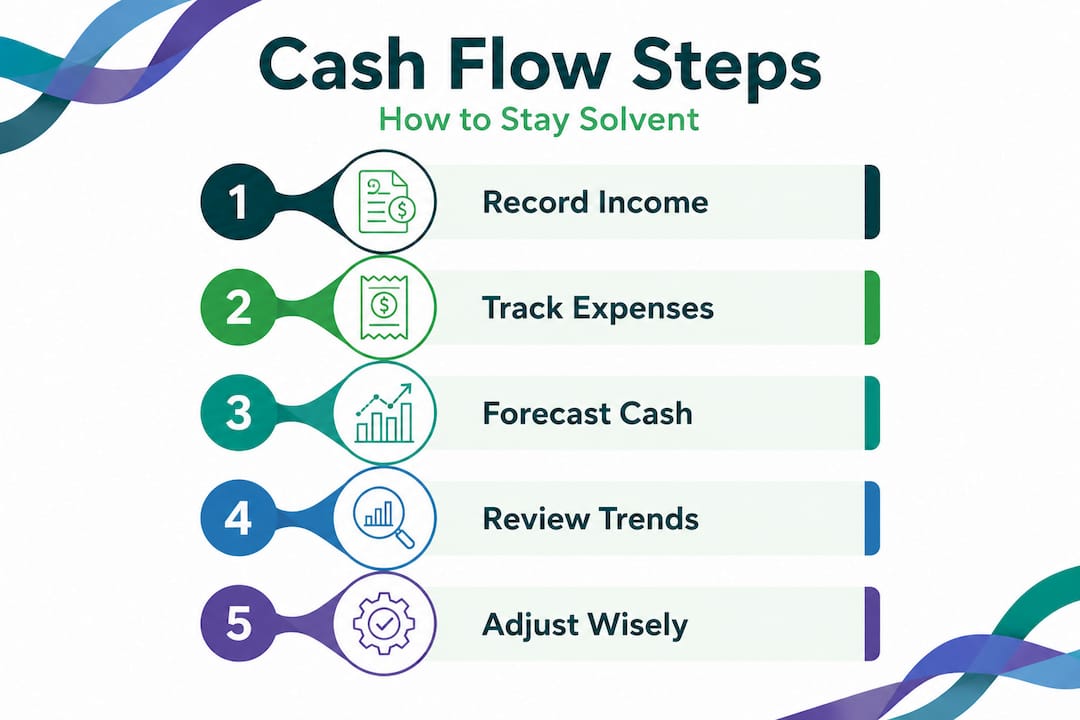

How to manage and forecast cash flow effectively

Cash flow management is the process of overseeing and adjusting the timing of your cash inflows and outflows so that you always have enough liquidity for both daily needs and longer-term commitments. For a UK SME, that means doing more than reading last month’s bank statement.

Here is a practical approach to building solid cash flow management habits:

- Create a rolling 13-week cash flow forecast. Thirteen weeks covers a quarter and is short enough to be accurate. Update it every week with actual receipts and payments.

- Use expected payment dates, not invoice dates. A reliable cash forecast is built on when you realistically expect cash to arrive, not when you raised the invoice.

- Reconcile your forecast to your actual bank balance every week. Variances tell you which assumptions need adjusting.

- Negotiate payment terms actively. Getting customers onto 14-day terms instead of 30 can transform your cash position without changing your profit by a penny.

- Match large outgoings to expected inflows. Do not schedule a large tax payment or equipment purchase in a week when customer receipts are typically low.

Beyond forecasting, these habits protect your cash position day to day:

- Maintain a cash buffer covering at least four to six weeks of fixed costs

- Review aged debtors every week, not every month

- Set up direct debits for all recurring supplier payments to avoid late-payment penalties

- Use cash management strategies that match your business cycle, not a generic template

Our cash flow forecasting guide walks through building a working forecast from scratch, and our practical cash flow management steps covers the week-to-week habits that keep your position stable.

Pro Tip: Most accounting software can produce a basic cash flow report automatically. But automated reports look backwards. Your forecast needs to look forward. Even a simple spreadsheet updated weekly will outperform a beautifully formatted report that nobody acts on.

With effective cash flow management and forecasting, your business can maintain stability and seize growth opportunities. Let us finish by reflecting on what most SMEs miss about cash flow and how to think differently.

Rethinking cash flow management: lessons for UK SME owners

The most common cash forecasting mistake we see is building forecasts from accounting data rather than from expected cash timings. Business owners pull figures from their bookkeeping software, use invoice dates as receipt dates, and then wonder why their forecast bears no resemblance to their actual bank balance two weeks later.

Cash flow is not an accounting report dressed up differently. It is a real-time picture of liquidity, and it only works if it is grounded in actual behaviour: when do your customers typically pay, not when are they supposed to? When does your payroll run leave your account? When does HMRC draw your VAT? These are the inputs that matter.

Reconciling projected cash movements to your actual bank position is not optional. It is the only way to know whether your model is reliable or whether you are planning against fiction. We consistently find that businesses who reconcile weekly make better decisions, negotiate from a position of knowledge, and are rarely caught off guard by a tax bill or a slow-paying client.

There is also a diagnostic value to cash flow that most owners overlook entirely. A growing gap between reported profit and actual cash is often the first visible sign of operational stress, whether that is a client base that is quietly extending payment, a cost base creeping up faster than revenue, or a product margin that looks fine on paper but is being eroded by hidden expenses. Reading your business forecasting data alongside your cash flow statement gives you an early warning system that profit figures simply cannot provide.

Think of cash flow as your business’s real-time health monitor, not as an annual compliance document. The businesses that treat it that way are the ones that survive tight markets and scale with confidence.

How Concorde Company Solutions supports your cash flow and payroll needs

Payroll is typically one of the largest and most time-sensitive cash outflows for any SME. Miss a run date, underpay a pension contribution, or fall foul of HMRC’s RTI requirements, and you face both a financial and a compliance problem simultaneously.

At Concorde Company Solutions, we work with small and medium-sized businesses across the UK to take payroll off your plate entirely. Our UK SME payroll services are designed to integrate with your broader cash flow planning so that you know exactly when payroll will leave your account, what your obligations are, and how to build that reliably into your forecasts. No surprises. No last-minute scrambles. Just accurate, compliant payroll that supports your financial stability rather than undermining it.

Frequently asked questions

What is the difference between cash flow and profit?

Cash flow and profit differ because profit uses accrual accounting and includes non-cash items, whilst cash flow only tracks money that physically moves in and out of your account. You can show a profit whilst having insufficient cash to pay your bills.

Why is cash flow management important for a small business?

Cash flow keeps your business solvent, ensuring you can pay wages and suppliers on time. A business with strong profit but poor cash flow management can still fail if it cannot meet its short-term obligations.

How can I forecast cash flow accurately for my UK SME?

Build your forecast using expected payment timings, not invoice dates or accounting periods, and reconcile it to your actual bank balance every week. This closes the gap between a theoretical model and what is actually happening in your business.

What are the three types of cash flow in financial statements?

Under UK GAAP and IFRS, the three types are operating cash flow from core business activities, investing cash flow from asset purchases and sales, and financing cash flow from loans, equity, and dividends.

How does payroll affect my business cash flow?

Payroll is usually one of the largest and most predictable cash outflows, so accurate timing and compliance are essential. Errors or missed runs can create unexpected costs that disrupt even a well-managed cash position.

No responses yet