TL;DR:

- HMRC compliance is essential for UK small businesses to avoid penalties and maintain accurate records. Understanding obligations like Self Assessment, VAT, and payroll ensures timely filings and reduces audit risks. Proper documentation, proactive preparation, and professional support simplify adherence and foster confidence in tax practices.

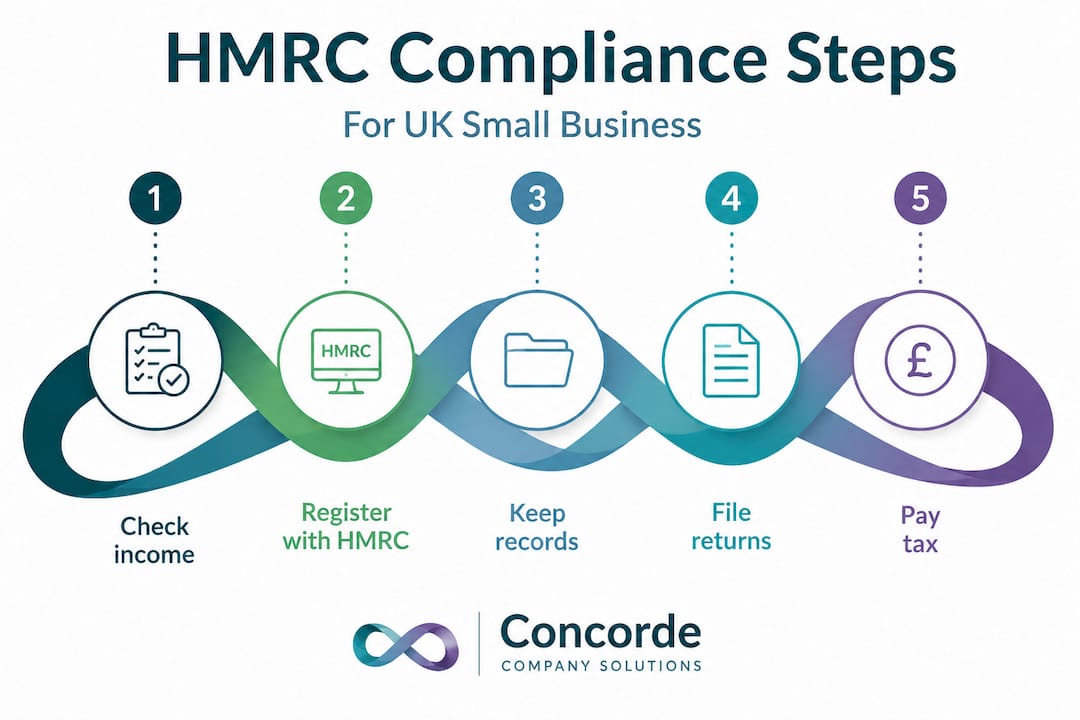

Running a small business or working as a sole trader in the UK means HMRC compliance is unavoidable. Yet for many owners, this guide to HMRC compliance is exactly what was missing when deadlines crept up and penalties landed without warning. Understanding HMRC regulations is not just about ticking boxes. It is about protecting your business from costly errors, keeping your records audit-ready, and filing with confidence rather than dread. This article walks you through every key obligation, from Self Assessment to VAT and payroll, so you can meet your tax duties accurately and on time.

Table of Contents

- Understanding HMRC compliance obligations

- Preparing your records and filings for accurate submission

- Executing your HMRC filings and meeting deadlines

- Navigating HMRC compliance checks and audits

- Rethinking HMRC compliance: practical insights from experience

- How professional payroll and tax services simplify HMRC compliance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your filing obligations | If self-employed with income over £1,000 or VAT-registered, you must file appropriate returns annually or quarterly. |

| Keep accurate records | Maintain digital accounting records and payroll data for several years to support correct filings and audits. |

| Declare truthfully | Ensure your tax returns are correct and complete to the best of your knowledge and use prudent legal views. |

| Meet deadlines | Submit tax returns online by 31 January and VAT or payroll filings on time to avoid penalties. |

| Prepare for HMRC checks | Respond promptly with clear documentation if HMRC requests information to resolve compliance enquiries quickly. |

Understanding HMRC compliance obligations

Before you can follow best practices for HMRC compliance, you need to know which obligations actually apply to you. The rules differ depending on whether you are a sole trader, a limited company director, or an employer, and confusing these categories is one of the most common HMRC compliance issues smaller businesses encounter.

Sole traders earning over £1,000 must file a Self Assessment tax return each year. That threshold applies to gross income before expenses or reliefs, so even a modest side income from freelancing or rental property can trigger the requirement. Many people do not realise they crossed that line until HMRC contacts them, at which point late filing penalties may already be accumulating.

VAT is its own layer. If your taxable turnover exceeds £90,000 in any 12-month rolling period, you must register and file under Making Tax Digital (MTD). VAT-registered businesses must keep digital records for six years and submit quarterly VAT returns digitally, using software that links directly to HMRC’s systems. Paper VAT records are no longer acceptable for MTD businesses, and manual re-keying of figures between systems is a specific compliance breach HMRC watches for.

If you employ staff, payroll compliance adds another dimension entirely. Payroll compliance requires timely FPS submissions and record retention of at least three years. An FPS, or Full Payment Submission, must reach HMRC on or before each payday. Missing a single submission can trigger an automated penalty notice, even if your payments to employees were correct.

Here is a summary of the key record retention periods you need to know:

- Self Assessment records: five years after the 31 January filing deadline for the relevant tax year

- VAT records: six years minimum under MTD rules

- Payroll records: three years minimum, though six years is advised

- Company accounts and corporation tax records: six years from the end of the accounting period

For a fuller breakdown of your payroll compliance obligations, it is worth reviewing a structured checklist before each tax year ends rather than waiting until filing season.

Preparing your records and filings for accurate submission

Good preparation is what separates a smooth filing from a stressful one. The ICAS guidance on compliance makes clear that HMRC’s own Guidelines for Compliance exist precisely to help businesses understand what the tax authority considers acceptable practice, and using them is an underused advantage.

HMRC requires your documents to be correct and complete to the best of your knowledge, using prudent legal interpretations that a court would likely uphold. That phrase “to the best of your knowledge” matters. It means you are not expected to be infallible, but you are expected to make a genuine, well-informed effort to get things right.

In practical terms, this means keeping contemporaneous records, meaning notes and documents created at the time of a transaction rather than reconstructed from memory months later. It also means that if a tax position is genuinely uncertain, you should disclose that uncertainty clearly in your return rather than glossing over it and hoping HMRC does not notice.

Follow these steps when preparing your records:

- Reconcile your bank statements monthly, not just at year end

- Label receipts and invoices clearly with their business purpose

- Separate personal and business expenditure rigorously

- Keep a written note of any decision where a grey area exists in the law

- Review HMRC’s compliance tips for avoiding penalties before finalising your return

Pro Tip: If you use an accountant or tax adviser, do not simply hand over your paperwork and assume the responsibility has transferred. Under UK tax law, the legal responsibility for the accuracy of your return remains with you as the taxpayer. Review what your adviser submits on your behalf, ask questions, and keep a copy of everything signed.

| Record type | Minimum retention | Recommended retention | Format required |

|---|---|---|---|

| Self Assessment | 5 years post-deadline | 6 years | Paper or digital |

| VAT (MTD) | 6 years | 6 years | Digital only |

| Payroll | 3 years | 6 years | Paper or digital |

| Corporation tax | 6 years | 6 years | Paper or digital |

Executing your HMRC filings and meeting deadlines

Knowing what to file is one thing. Filing it correctly and on time is another. Missing deadlines is one of the most avoidable common HMRC compliance issues small businesses face, and the penalties are automatic regardless of whether you owe tax.

Here is a step-by-step approach to managing your filing calendar:

- Register for Self Assessment early. If you are newly self-employed, register by 5 October following the end of the tax year in which you started trading. Late registration itself can attract a penalty.

- File your online Self Assessment by 31 January. Online Self Assessment must be filed by 31 January; paper filings carry an earlier deadline of 31 October. Miss either and an immediate £100 fixed penalty applies, with daily charges added after three months.

- Submit MTD VAT returns quarterly. MTD VAT returns are due quarterly, one month and seven days after the end of each VAT period, submitted with digital links through approved software. Any MTD VAT errors must be corrected in subsequent returns rather than via amended submissions.

- Send payroll FPS on or before each payday. FPS submissions and payroll records should be retained for at least six years. If you pay weekly, that means 52 submissions per year, each with its own deadline.

- Review and amend if necessary. You can correct your online Self Assessment return within 12 months of the 31 January deadline without needing formal permission from HMRC.

Pro Tip: Set calendar reminders 30 days before every filing deadline, not just seven days. That lead time allows you to chase missing invoices, reconcile discrepancies, and avoid the compressed panic that leads to errors.

| Filing type | Deadline | Penalty for missing |

|---|---|---|

| Online Self Assessment | 31 January | £100 immediate, then daily charges |

| Paper Self Assessment | 31 October | £100 immediate |

| MTD VAT return | 1 month and 7 days after period end | Surcharge or points-based penalty |

| Payroll FPS | On or before payday | Automated penalty notice |

Navigating HMRC compliance checks and audits

Receiving a letter from HMRC requesting documents is unsettling for any business owner. However, understanding how HMRC compliance checks work removes a great deal of the anxiety. HMRC compliance checks begin with a document request and are typically resolved within weeks to months, though full enquiries can last up to 24 months.

Not every compliance check signals that HMRC suspects wrongdoing. Many are triggered by statistical anomalies, such as expenses running unusually high relative to turnover in your sector, or by random selection. HMRC uses a risk profiling system called Connect, which cross-references data from multiple sources including banks, land registries, and Companies House. If your return looks inconsistent with those data points, a check may follow.

Here is what to expect and how to respond:

- Acknowledge the letter promptly. HMRC typically asks for documents within 30 days. Ignoring the letter does not pause the process; it accelerates penalties.

- Gather only what is requested. Providing more documents than asked can inadvertently open additional lines of enquiry.

- Respond in writing where possible. Written responses create a clear record and reduce the risk of misunderstandings.

- Seek professional representation. For any enquiry beyond a simple information request, a qualified accountant or tax adviser should handle correspondence on your behalf.

- Review your preparation guidance. Our article on how to prepare for an HMRC audit covers the specific documentation HMRC most commonly requests.

“The best time to prepare for a compliance check is before it happens. Clear, well-organised records do not just help you file accurately; they make any subsequent HMRC enquiry far quicker and less disruptive to your business.”

Pro Tip: If HMRC opens a full enquiry, do not assume the worst. Many enquiries close with no additional tax due once supporting documentation is provided. Cooperation is formally recognised by HMRC as a factor that reduces any penalties charged.

Rethinking HMRC compliance: practical insights from experience

There is a persistent belief among small business owners that HMRC compliance is purely about paperwork. It is not. It is about the quality of your decision-making at every financial touchpoint, and that is a meaningful distinction.

One of the most consistent issues we see is businesses that file correctly on paper but have never documented why they made a particular tax decision. If a grey area existed and you took a reasonable position, but you did not record your reasoning at the time, that reasoning is almost impossible to reconstruct credibly during a compliance check two years later. Applying HMRC’s Guidelines for Compliance helps SMBs understand HMRC’s risk focus and adopt strategies that reduce unnecessary contacts, without any change to what tax is legally owed.

Many business owners also over-rely on their accountant in a way that inadvertently increases their risk. Your adviser’s job is to apply the law correctly based on the facts you provide. If the facts you give them are incomplete or inaccurate, the filing will be too. The responsibility does not transfer with the fee. Reviewing what is submitted, even at a high level, is not a sign of distrust. It is sound business practice.

Finally, fear of audits leads many SMBs to take overly conservative positions, paying more tax than necessary to avoid drawing attention. That is a real cost, and it is avoidable. Transparent disclosure of uncertainties, where they genuinely exist, is not an invitation for scrutiny. It is actually viewed favourably by HMRC as evidence of good faith. Understanding what HMRC compliance means for your specific business type is the foundation of confident, accurate filing.

How professional payroll and tax services simplify HMRC compliance

Meeting every HMRC filing deadline, maintaining digital records, running accurate payroll, and staying current with changing regulations is a significant burden when you are also running a business. That is where professional support makes a tangible difference.

At Concorde Company Solutions, we work with small businesses, sole traders, and limited companies across Leeds and beyond to take the stress out of tax compliance. Our professional payroll services ensure your Full Payment Submissions are filed correctly on or before every payday, your PAYE payments are accurate, and your records are audit-ready. We also support clients with Self Assessment, VAT returns under MTD, and bookkeeping using HMRC-approved software that integrates directly with the systems you already use. If you want to understand what a fully supported compliance process looks like in practice, our payroll compliance checklist guide is a good place to begin. Get in touch to discuss how we can support your business.

Frequently asked questions

Who must file a Self Assessment tax return with HMRC?

If you were self-employed as a sole trader and earned over £1,000 before reliefs in a tax year, you must file a Self Assessment tax return. Other triggers include having untaxed income, being a company director, or earning over £100,000 through PAYE.

What are the deadlines for submitting HMRC tax returns online?

Online Self Assessment must be filed by 31 January following the end of the relevant tax year, with an automatic £100 penalty applying immediately for late submission. Paper returns have an earlier deadline of 31 October.

How long do I need to keep VAT and payroll records?

You must keep digital VAT records for six years under MTD rules, while payroll records require retention for a minimum of three years. Retaining both for six years is widely recommended as best practice.

What happens if HMRC performs a compliance check on my business?

HMRC will send a letter requesting documents, typically expecting a response within 30 days. Simple checks can be resolved in weeks, while full enquiries can last up to 24 months; prompt cooperation and clear records significantly reduce the duration.

Can I amend my Self Assessment tax return after filing?

Yes. You can amend your online return within 12 months of the 31 January filing deadline, so a 2024/25 return filed by 31 January 2026 can be corrected up to 31 January 2027. After that window, any changes require a formal written amendment request to HMRC.

No responses yet