TL;DR:

- Many UK limited company directors mistakenly assume business funds are personal assets, risking costly tax penalties. Proper management of directors’ loan accounts—recording transactions accurately and reconciling regularly—is essential for compliance and financial transparency. HMRC increasingly emphasizes detailed reporting and vigilance on DLAs, underscoring the importance of diligent record-keeping throughout the year.

Many directors of UK limited companies make the same costly assumption: that money sitting in the business account is theirs to use freely. It is not. Understanding what is a directors’ loan account, and what it actually records, is one of the most important things you can do to protect yourself from unexpected tax bills and HMRC scrutiny. A directors’ loan account (DLA) is not a pot of company cash. It is a ledger that tracks every penny borrowed from or lent to your company outside of your salary or dividends, and getting it wrong can be expensive.

Table of Contents

- Understanding directors’ loan accounts and how they work

- Different ways to track directors’ loan accounts in accounting

- Tax implications and HMRC’s focus on directors’ loan accounts

- Practical tips for managing your directors’ loan account effectively

- Directors’ loan accounts versus personal and company finances

- Fresh perspectives on directors’ loan accounts: avoiding common pitfalls and future trends

- How Concorde Company Solutions supports your directors’ loan account management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Directors’ loan account explained | It is a bookkeeping record tracking money lent to or borrowed from the company by directors, not cash in the bank. |

| DLA accounting methods | DLAs can be recorded as current liabilities, bank accounts, or equity accounts, each affecting financial reporting differently. |

| Tax and compliance risks | Overdrawn DLAs can incur personal tax charges; HMRC demands detailed and timely reporting to avoid penalties. |

| Maintain accurate records | Regular reconciliation and clear documentation of all DLA movements help ensure compliance and financial clarity. |

| Seek expert support | Professional bookkeeping and compliance services simplify managing DLAs and help avoid costly mistakes. |

Understanding directors’ loan accounts and how they work

A directors’ loan account is, at its core, a bookkeeping record. As Unbiased describes, a UK limited company’s DLA is a running record of transactions between the director and the company that are not treated as salary, dividends, or legitimate expense reimbursements. Think of it as a tab at a pub, except this one has real tax consequences if it runs too high.

The account operates in two directions. When a director withdraws money from the company for personal use, that amount is recorded as a debit to the DLA, making the account overdrawn. When the director puts personal money into the company or leaves funds in the business they are owed back, the DLA goes into credit. Both positions have different accounting and tax consequences.

Understanding this two-way flow matters enormously if your company has multiple directors or shareholders. Without a clearly maintained DLA for each individual, it becomes nearly impossible to establish who owes what, especially during a dispute or HMRC enquiry. Your limited company compliance guide obligations require accurate records, and the DLA sits at the centre of that requirement.

Here is what a DLA typically records:

- Money taken from the company for personal use (overdrawn position)

- Personal funds deposited into the company (credit position)

- Business expenses paid personally and not yet reimbursed

- Interest charged on loans, either by the director or by the company

- Loan write-offs or waivers agreed by the company

Every one of these transactions must be recorded with dates, amounts, and purpose. The DLA is not a rounding-up exercise done at year-end. It should reflect live, accurate movements throughout the financial year. The role of directors in accounting includes the responsibility to ensure these records exist and are kept current.

Different ways to track directors’ loan accounts in accounting

Understanding what a directors’ loan account is leads naturally to how it should be recorded in your accounting system. There are broadly three ways accountants and business owners set up DLA tracking, each with its own advantages and pitfalls.

The most common approach is to record the DLA as a current liability in the balance sheet. This reflects money the company owes back to the director, making it clear that a repayment obligation exists. It keeps the records clean and is the most straightforward method for HMRC reporting. As QuickBooks UK notes, accounting software guidance commonly describes the DLA as a liability versus equity, reinforcing that it tracks what is due or owing rather than actual cash at bank.

Some business owners set up the DLA as a bank account within their accounting software. This makes it easier to reconcile because you can match transactions directly. However, it risks confusion with your actual current or business bank accounts, particularly when producing cash flow statements or management reports.

A third option is recording the DLA under equity, treating the director’s contributions as a form of investment in the business. This can work in certain circumstances but tends to complicate tax reporting and makes it harder to distinguish a loan from a permanent capital contribution.

| Method | Pros | Cons |

|---|---|---|

| Current liability | Clear repayment obligation, HMRC-friendly | Requires careful management of credit/debit distinction |

| Bank account | Easy reconciliation in software | Can blur distinction from real cash accounts |

| Equity account | Reflects director’s investment | Complicates tax reporting and loan categorisation |

Pro Tip: If you are using cloud accounting software such as Xero or QuickBooks, set up the DLA as a current liability account from day one. It is easier to correct from there than to unwind equity classifications later, particularly at year-end.

The method you choose affects your financial reports, your business record-keeping obligations, and ultimately how transparent your accounts look to HMRC. Do not let this be an afterthought.

Tax implications and HMRC’s focus on directors’ loan accounts

Having covered accounting setups, it is vital to understand the significant tax implications and regulatory spotlight on directors’ loan accounts. This is where many directors discover, too late, that casual DLA management carries serious financial consequences.

The most important concept to understand is the Section 455 tax charge. If your DLA is overdrawn at your company’s year-end and remains unpaid nine months after that date, HMRC levies a temporary corporation tax charge of 33.75% on the outstanding balance. The word “temporary” is technically accurate: it is repayable once the loan is repaid. But in practice, it creates a significant cash flow burden precisely when you may least want it.

Beyond Section 455, an overdrawn DLA can create benefit-in-kind (BIK) implications. If the loan exceeds £10,000 at any point during the tax year and no commercial interest is being charged, HMRC treats the interest benefit as a taxable perk. That means Class 1A National Insurance contributions for the company and income tax for the director. Neither is trivial.

HMRC’s oversight of DLAs is increasing significantly. The regulator has proposals underway that would require far more granular, transaction-level reporting of DLA activity, including loan write-offs and releases. As Warrington Worldwide reports, HMRC has ongoing focus on director and shareholder loans through proposals requiring detailed reporting of transactions, repayments, and write-offs.

Key risks to be aware of include:

- Section 455 tax on overdrawn loans not repaid within nine months of year-end

- Benefit-in-kind charges on loans over £10,000 without commercial interest

- Income tax if a loan is written off (treated as a distribution)

- HMRC penalties for incomplete or inaccurate DLA records

- Increased audit risk if DLA patterns suggest income disguised as loans

Staying compliant with financial compliance obligations is no longer just about year-end housekeeping. HMRC’s direction is toward year-round visibility into directors’ loan activity.

Practical tips for managing your directors’ loan account effectively

With tax implications understood, let us explore how you can practically manage your directors’ loan account to maintain compliance and avoid pitfalls. None of this requires specialist software or daily attention. It does require consistency.

-

Reconcile monthly, not annually. Check your DLA balance every month against your bank records. Identify the opening balance, all movements in and out, and the closing balance. Catching an overdrawn position in month three is far less painful than discovering it in week two of an HMRC enquiry.

-

Document every transaction. Every time money moves between you and the company outside of payroll or dividends, write it down. Date, amount, purpose, and whether it is a loan or a repayment. Informal arrangements are precisely what HMRC is targeting.

-

Avoid using the company account for personal spending without logging it. Buying personal items on the company card and forgetting to record it in the DLA is one of the most common mistakes small business owners make. It does not disappear because you ignored it.

-

React quickly to an overdrawn balance. If your DLA is in debit, address it before your company’s year-end where possible. Options include repaying cash, declaring a dividend (if retained profits allow), or processing additional salary. Each has its own tax consequences, so take advice early.

-

Keep records of interest agreements. If your company is charging you interest on an overdrawn loan, or you are charging the company interest on funds you have lent, document the terms. An agreed, commercially reasonable interest rate protects both parties from BIK complications.

-

Work with your accountant throughout the year. Accurate accounting compliance depends on timely information. Waiting until January to hand over a year’s worth of receipts and hoping it reconciles is a strategy that works until it suddenly does not.

As Warrington Worldwide highlights, maintaining accurate DLA records and avoiding undocumented transactions reduces compliance risk in light of HMRC’s increased oversight.

Pro Tip: Set a calendar reminder on the first of every month to review your DLA balance. Ten minutes of reconciliation now saves hours of correction later, and it is the kind of habit that keeps your year-end accountancy bill predictable.

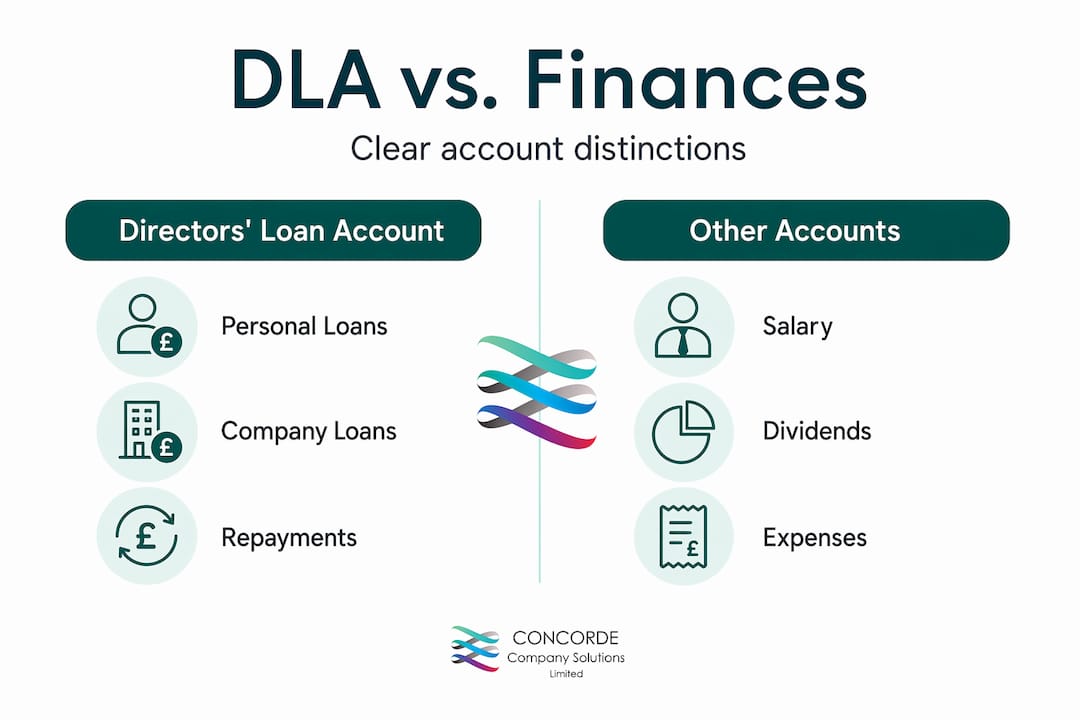

Directors’ loan accounts versus personal and company finances

Before moving on, it is important to clear up the frequent confusion between DLAs and other financial accounts to ensure proper business financial management. The misunderstanding is remarkably common and has real consequences.

The DLA is not your salary account. It is not your dividend record. It is not a reflection of how profitable your company is. As Unbiased points out, most owners misunderstand DLAs as extra company cash; the DLA is actually a bookkeeping record reflecting amounts owed, not company profits or bank balances.

Here is a quick comparison to clarify the key distinctions:

| Financial element | What it represents | Recorded in DLA? |

|---|---|---|

| Director’s salary | Contractual payment for work done | No |

| Dividend payment | Distribution of company profits | No |

| Money taken outside salary/dividends | A loan from the company to the director | Yes |

| Personal funds put into the company | A loan from the director to the company | Yes |

| Business expenses paid personally | Reimbursement owed by company | Yes |

Mixing personal and company bank accounts is the fastest route to DLA chaos. When personal spending runs through the company account without categorisation, it creates a jumbled record that no one can interpret with confidence, including HMRC. Understanding which business expense categories belong where is the foundation of keeping your DLA clean.

Maintaining separation between personal and company finances is not just good practice. It is a safeguard against both tax risk and shareholder disputes.

Fresh perspectives on directors’ loan accounts: avoiding common pitfalls and future trends

Here is an uncomfortable truth that most articles on DLAs avoid: the directors who get into the most trouble are rarely the ones who intended to break the rules. They are the ones who never thought the rules applied to small sums, or who assumed the accountant would sort it out at year-end.

The “it is only a small amount” thinking is particularly dangerous. An overdrawn DLA of £500 that is rolled forward year after year, never documented, never repaid, does not stay invisible. It compounds. It becomes a pattern in your accounts that looks, to an HMRC inspector, like disguised income. The defence that “I always meant to pay it back” carries very little weight without a documented repayment plan.

HMRC’s direction is clear. The regulator’s trend toward more detailed DLA reporting is not a temporary enforcement drive. It reflects a structural shift toward year-round ledger transparency rather than annual summaries. Businesses that treat DLA management as an administrative inconvenience to be dealt with in March will find that increasingly costly.

The most successful small business owners we see are the ones who have integrated DLA management into their regular financial routine. Not as a compliance chore, but as a genuine management tool. A well-maintained DLA gives you a clear picture of your financial relationship with the company, helps you plan salary and dividend strategies more effectively, and signals to any future investor, lender, or buyer that your accounts are trustworthy.

The importance of financial compliance extends well beyond avoiding penalties. It underpins the credibility of your entire business.

How Concorde Company Solutions supports your directors’ loan account management

Understanding the complexity of directors’ loan accounts, professional support can make managing compliance genuinely straightforward rather than stressful.

At Concorde Company Solutions, we work with small UK limited companies to ensure their directors’ loan accounts are accurately maintained, correctly classified, and fully compliant with HMRC requirements. From setting up your DLA correctly in your accounting software to managing year-end reconciliations and advising on the most tax-efficient way to address overdrawn balances, we take the guesswork out of one of the most misunderstood areas of small business accounting. If you want your accounts to be something you rely on rather than worry about, we would be glad to help.

Frequently asked questions

What happens if my directors’ loan account is overdrawn?

An overdrawn directors’ loan account means the director owes money to the company, which can trigger a Section 455 tax charge if the loan is not repaid within nine months of the company’s year-end, as well as potential benefit-in-kind liabilities on amounts over £10,000.

Can a director lend money to their company and does it affect tax?

Yes, a director can loan money to their company, recorded as a creditor balance in the DLA; any interest charged must be declared as income on the director’s self-assessment tax return.

How often should I reconcile my directors’ loan account?

Monthly reconciliation is best practice, as DLAs must identify opening and closing balances alongside all movements, making it far easier to manage tax exposure before it becomes a year-end problem.

Are directors’ loan accounts separate from salary and dividends?

Yes, a director’s loan is money taken outside salary, dividends, or legitimate expenses and must be recorded separately in the DLA to comply with tax and accounting rules.

What are HMRC’s recent proposals for directors’ loan account reporting?

HMRC is pursuing granular reporting of directors’ loans including cash movements, bank transfers, and write-offs, signalling a move toward far greater transparency and ongoing monitoring of DLA activity rather than annual summaries.

No responses yet