TL;DR:

- Inadequate or missing records can lead to penalties of up to £3,000 per tax year and increased legal risks for UK small businesses. Accurate, up-to-date records are essential for legal compliance, operational insight, and securing funding, transforming record-keeping into a strategic business asset. Implementing digital tools, regular reconciliation, and viewing records as infrastructure help ensure compliance, improve decision-making, and support growth.

Inaccurate or missing records can cost your business thousands in penalties before you even realise there’s a problem. HMRC penalties can reach up to £3,000 per tax year for inadequate record-keeping, on top of interest charges and additional tax assessments. Yet countless small business owners in the UK still treat record-keeping as something to worry about once a year, usually in a mad rush before a filing deadline. This article cuts through the confusion, setting out your legal obligations, the real cost of getting it wrong, and the practical steps you can take to turn accurate records into a genuine advantage for your business.

Table of Contents

- What does accurate record-keeping mean and why does it matter?

- Legal and tax risks: What happens if your records fall short?

- How accurate records power better business decisions

- Practical steps: Getting it right, staying compliant

- Why most SMEs undervalue records and how to flip the script

- Need help staying compliant and efficient?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal requirement | Maintaining accurate records is required by the Companies Act and HMRC for all UK businesses. |

| Avoid heavy penalties | Poor record-keeping risks HMRC penalties up to £3,000 per year and further tax liability. |

| Better decisions | Clear records help you track cash flow, claim all expenses, and access finance. |

| Practical workflow tips | Digital tools, regular updates, and clear retention routines make accuracy manageable. |

What does accurate record-keeping mean and why does it matter?

Accurate record-keeping sounds straightforward, but it is worth being precise about what it actually means in practice. Accurate records are those that are up to date, consistent across all entries, and verifiable against real transactions. That means every sale, every purchase, every expense, and every payment in or out of your business should be captured promptly and matched to a supporting document such as an invoice, receipt, or bank statement.

There are two distinct reasons this matters. The first is legal. The second is operational. Let’s deal with the legal side first.

Under Companies Act 2006 Section 386, every company registered in the UK must maintain accounting records sufficient to show and explain its transactions, disclose its financial position with reasonable accuracy at any time, and enable directors to prepare statutory accounts. This is not optional guidance. It is a statutory duty, and failing to meet it puts directors personally at risk of civil penalties.

“Companies Act 2006 requires that accounting records must be kept that show and explain the company’s transactions, disclose with reasonable accuracy the financial position of the company at any time, and enable the directors to ensure that any accounts required to be prepared comply with the requirements of the Act.”

HMRC operates a parallel set of requirements. HMRC’s standard is that records must be accurate, complete, and retrievable so that tax liability can be calculated correctly. Poor or incomplete records are one of the most common triggers for an HMRC enquiry. Inspectors are trained to spot the warning signs, including unexplained gaps, round-number entries, and inconsistencies between VAT returns and accounts.

Beyond compliance, lenders and auditors scrutinise records with equal intensity. If you ever apply for a business loan, seek investment, or go through an acquisition, your records become the primary evidence of your business’s health. Weak records immediately undermine trust, even if the underlying numbers are strong. Read our essential guide for UK SMEs for a fuller breakdown of what auditors and lenders look for.

Items typically included in business records:

- Sales invoices and till receipts

- Purchase invoices and expense receipts

- Bank and credit card statements

- Payroll records, including employee details and payslips

- VAT records (for VAT-registered businesses)

- Asset registers for equipment and property

- Loan agreements and contracts

- Minutes of directors’ meetings (for limited companies)

| Record type | Frequency of update | Common tool |

|---|---|---|

| Sales ledger | Daily or per transaction | Accounting software |

| Purchase ledger | Daily or per invoice | Accounting software |

| Bank reconciliation | Weekly or monthly | Cloud banking feed |

| Payroll records | Each pay period | Payroll software |

| VAT return data | Quarterly | MTD-compliant software |

Legal and tax risks: What happens if your records fall short?

With an understanding of the foundations, it is vital to see how failing at record-keeping impacts your legal standing and business security. The consequences are not abstract. They are financial, reputational, and in some cases, criminal.

HMRC’s enforcement process follows a predictable sequence, and knowing it should sharpen your focus.

- Initial enquiry letter. HMRC opens a compliance check, requesting specific records for a given tax year. Businesses with poor records immediately face a disadvantage because they cannot produce what is asked for.

- Extended investigation. If the initial review raises questions, the enquiry widens. This can cover multiple tax years and involve detailed interviews with directors or sole traders.

- Penalty assessment. HMRC issues a financial penalty based on the level of non-compliance. Penalties can reach £3,000 per tax year for inadequate records, with interest charged on any underpaid tax.

- Additional tax assessment. HMRC estimates the tax it believes was due and issues a formal assessment. Without proper records, you have very little grounds to challenge their figures.

- Legal proceedings. In cases of deliberate non-compliance or fraud, HMRC can pursue criminal prosecution, which can result in fines or imprisonment.

The financial scale of HMRC enforcement is significant. HMRC issued over £1 billion in penalties in a recent year for late and inaccurate returns. For small businesses already operating on tight margins, even a fraction of that is devastating.

| Business type | Maximum penalty per tax year | Additional risk |

|---|---|---|

| Sole trader | Up to £3,000 | Interest on underpaid tax |

| Limited company | Up to £3,000 per officer | Director disqualification |

| VAT-registered business | VAT surcharges plus penalties | Extended investigation period |

Understanding HMRC compliance means knowing that these risks are avoidable. Visit our guide on preventing tax losses to see specific strategies that reduce your exposure.

Pro Tip: Invest in cloud accounting software as early as possible. Tools with automated bank feeds and receipt scanning create a continuous, timestamped document trail that is far more defensible in an HMRC enquiry than a shoebox of paper receipts.

How accurate records power better business decisions

Legal obligations are not the only reason to keep your records in order. Discover the less obvious advantages that make diligent record-keeping a growth tool rather than a chore.

Accurate records are, in effect, a live dashboard of your business. When your books are current, you can see at a glance what money is coming in, what is going out, and where the gaps or opportunities lie. That kind of visibility is what separates reactive businesses from proactive ones.

Critical benefits of accurate records:

- Cash flow insight. You can identify slow-paying clients, upcoming large outgoings, and potential shortfalls before they become emergencies.

- Maximising expense claims. You can only claim legitimate business expenses if you have receipts and invoices to prove them. Businesses that lose paperwork routinely leave money on the table.

- Data-driven decisions. Accurate records expose which products, services, or clients are most profitable, allowing you to allocate resources wisely.

- Funding and finance applications. Banks and alternative lenders require verified accounts and up-to-date management figures. Strong records make applications faster and more credible.

- Error prevention. Regular reconciliation catches mistakes, duplicate payments, and fraud early, before they compound.

Consider a practical example. A small construction firm buys materials and subcontracts work throughout a project. If the owner cannot produce VAT invoices for those costs, they cannot reclaim the input VAT on their return. On a project worth £100,000 with significant material costs, that oversight could amount to thousands of pounds in irrecoverable VAT. That is not a compliance failure in the abstract. That is real money lost.

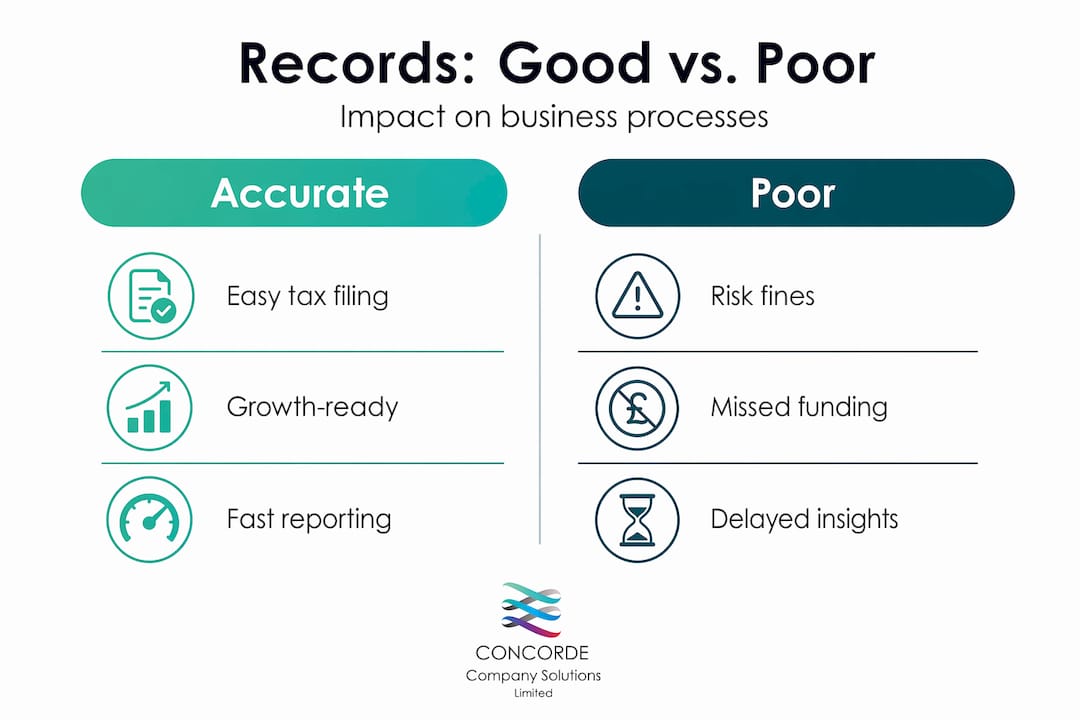

The table below shows how accurate versus poor records affect key business processes.

| Business process | Accurate records | Poor records |

|---|---|---|

| Tax return filing | Straightforward, lower risk | Estimated figures, higher risk of penalties |

| VAT reclaim | Full reclaim on evidenced costs | Partial or no reclaim possible |

| Finance application | Credible, supported application | Rejected or delayed |

| Cash flow management | Real-time visibility | Reactive, often crisis-driven |

| Year-end accountancy | Efficient, lower fees | Time-consuming, higher fees |

| Business sale or investment | Due diligence passed quickly | Extended scrutiny, reduced valuation |

For a deeper look at how records support business management, explore the types of accounting records that UK businesses typically need to maintain.

Pro Tip: Schedule a monthly record review rather than leaving everything until year end. Even a one-hour session each month allows you to catch errors, review profitability, and make sensible adjustments to spending or pricing before it is too late to act.

Practical steps: Getting it right, staying compliant

Understanding benefits and risks means little without clear, actionable instructions. Here is how to build a record-keeping routine that actually works for a busy business owner.

Setting up your system: Step by step

- Choose a digital bookkeeping tool. Cloud platforms designed for UK businesses keep records in a format that is compatible with Making Tax Digital requirements and allows HMRC to access data when needed. Review our Making Tax Digital VAT guide for specifics on compliance.

- Separate business and personal finances. Open a dedicated business bank account immediately if you have not already done so. Mixing personal and business transactions is one of the most common causes of recording errors and tax complications.

- Establish a consistent categorisation system. Decide how you will categorise income and expenses and stick to it. Consistent categorisation makes year-end accounts, VAT returns, and tax filings far simpler.

- Reconcile accounts regularly. At least monthly, compare your accounting software records against your actual bank statements. Discrepancies should be investigated and resolved promptly.

- Back up your data. Cloud software automatically backs up, but if you use spreadsheets or local software, schedule regular exports to a secure, separate location.

- Confirm your retention periods. According to HMRC retention rules, sole traders must keep records for five years after the Self Assessment tax return deadline, while limited companies and VAT-registered businesses must retain records for six years from the end of the financial year.

Common pitfalls to avoid:

- Ignoring receipts for small purchases. These add up and every one is a legitimate expense.

- Using your personal bank account for business transactions, which blurs the line and creates significant work to untangle.

- Failing to back up digitally. Physical records can be destroyed, stolen, or simply lost.

- Leaving reconciliation until year end, by which point errors are difficult and expensive to correct.

- Not keeping records of asset purchases and disposals, which affects capital allowances.

Our guide to the digital tax submission process explains how digital records feed directly into your tax submissions. For growing businesses looking to scale their record systems, this resource on scaling digital record systems offers useful context on building for growth.

Pro Tip: Weekly updates beat a stressful year-end scramble every single time. Spend fifteen minutes each Friday entering that week’s transactions. By the time your accountant needs year-end figures, you will have twelve months of clean, complete data ready to go.

Why most SMEs undervalue records and how to flip the script

Here is an uncomfortable truth: most small business owners treat record-keeping as an obligation imposed on them by the government, rather than a tool they chose to use for their own benefit. That framing is understandable, but it is also costing those businesses real money.

Many businesses view records as tedious, yet the practical benefits consistently outweigh the time invested. The problem is that the costs of poor records are hidden and delayed, while the effort of maintaining good records is visible and immediate. That asymmetry tricks business owners into underinvesting.

Flip the perspective. Accurate records expose waste. When you can see exactly where every pound is going, patterns emerge quickly. A subscription you forgot about. A supplier charging more than agreed. A product line that consistently underperforms. None of these are visible if your records are patchy or months out of date. Strong records are not just about staying out of trouble. They are about identifying opportunity.

There is also a financing dimension that SMEs frequently overlook. When a business approaches a bank or investor for funding, the quality of its records sends an immediate signal about the quality of its management. A business with clean, current, well-organised accounts inspires confidence. One with rough estimates and missing invoices does not, regardless of how genuinely profitable it might be. Good records are, in effect, a marketing asset when it comes to raising capital.

The mindset shift we advocate at Concorde Company Solutions is simple: stop thinking of record-keeping as a cost and start thinking of it as infrastructure. Just as you would invest in reliable broadband or quality tools, invest in the systems and habits that keep your financial data clean. The returns compound. Better decisions made throughout the year, lower accountancy fees, faster funding applications, and fewer HMRC headaches all flow from that one foundational discipline. Explore why businesses benefit from good records to see how that advantage plays out across different business types.

Need help staying compliant and efficient?

Managing records accurately while running a business is demanding. Mistakes happen, software gets neglected, and deadlines creep up before you are ready. That is where having a reliable accountancy partner makes a measurable difference.

At Concorde Company Solutions, we work with small and medium-sized businesses across the UK to take the pressure off compliance and record-keeping. From bookkeeping and payroll management to statutory accounts, company tax returns, and software setup, our business support services are designed to keep you on the right side of HMRC while giving you cleaner, more useful financial data to run your business with. Whether you are starting fresh or untangling years of inconsistent records, we offer transparent pricing and the kind of personalised support that larger firms rarely provide. Get in touch today and find out how we can help.

Frequently asked questions

What records must UK small businesses keep for tax?

You must keep detailed income, expenditure, and VAT records, plus receipts and invoices to prove your figures to HMRC. HMRC requires that all records are accurate, complete, and retrievable to enable correct tax liability calculations.

How long should I keep my business records in the UK?

Sole traders must keep records for five years after the Self Assessment tax return deadline, while limited companies and VAT-registered businesses must keep theirs for six years from the end of the financial year. Full details are in our HMRC requirements guide.

What is the penalty for poor record-keeping?

Penalties reach up to £3,000 per tax year for inadequate records, with possible additional tax assessments and interest charges on top.

Can cloud accounting software simplify compliance?

Yes, digital tools such as Xero and QuickBooks automate a significant portion of the record-keeping process, including bank feeds and VAT calculations, keeping you aligned with HMRC’s compliance standards and Making Tax Digital requirements.

No responses yet