TL;DR:

- An audit trail is a tamper-evident, chronological record of actions impacting business processes.

- It captures who, what, when, where, and the outcome of key activities, ensuring accountability and compliance.

An audit trail is defined as a chronological, tamper-evident record that documents who performed an action, what the action was, when it occurred, where it took place, and what the outcome was. Every business that handles financial data, processes payroll, or operates under HMRC or statutory reporting requirements needs one. Regulatory standards including PCI DSS v4.0, the EU AI Act Article 12, and PCAOB AS 1215 now treat audit trails as evidentiary infrastructure, not optional housekeeping. For business owners and accountants seeking financial transparency and compliance confidence, understanding the audit trail definition is the first step towards building a genuinely accountable operation.

What is an audit trail and what must it record?

An audit trail is a structured, protected, and chronological record of events within a system or business process. Unlike a general activity log, it is designed to be tamper-evident and to carry evidentiary weight in audits, investigations, and regulatory reviews. The term is used across accounting, IT security, and compliance disciplines, and the underlying concept is consistent: every significant action must be traceable back to its source.

Effective audit trails must capture five core elements to provide evidentiary value: Who, What, When, Where, and Result. Each element serves a distinct purpose in reconstructing what happened and why.

- Who: The user or system ID that initiated the action. This could be an employee login, an automated process, or an integrated third-party system.

- What: The specific action taken. For example, a payroll figure being amended, an invoice being approved, or a user account being created.

- When: A precise timestamp. Vague date references are insufficient. The timestamp must be accurate to the second and tied to a reliable time source.

- Where: The system, location, or application in which the action occurred. In distributed environments, this might include a server name, IP address, or software module.

- Result: Whether the action succeeded or failed. A failed login attempt carries as much investigative value as a successful one.

Beyond these five elements, mature audit trail systems also capture before and after values for any data change. If an accountant corrects an invoice amount from £4,500 to £4,050, the trail records both the original and the corrected figure. That level of detail is what makes audit trails genuinely useful during financial reviews and fraud investigations.

Pro Tip: Synchronise all system clocks using Network Time Protocol (NTP) or an equivalent. Clock drift in distributed systems undermines timestamp accuracy and can destroy the chronological integrity of your entire audit trail.

How do audit trails differ from raw system logs?

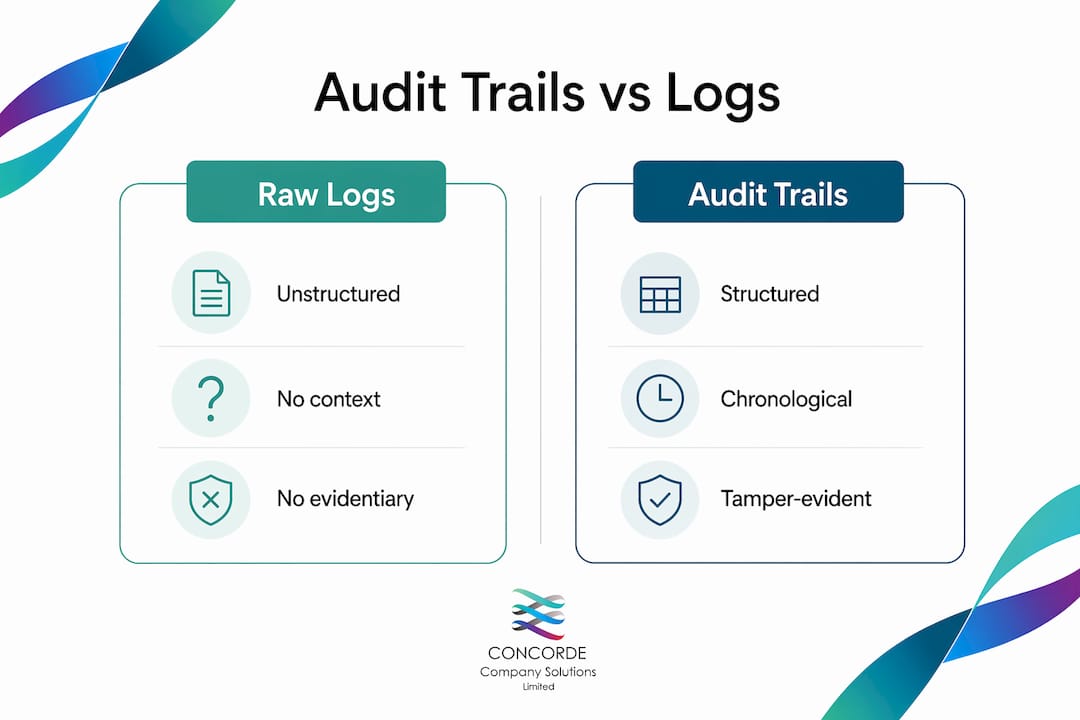

Audit trails and system logs are not the same thing, and confusing the two is one of the most common errors businesses make. A raw system log records everything a system does: routine operations, error messages, background processes, and user actions all mixed together without context or structure. An audit trail is a curated, protected subset of that data, organised specifically for accountability and forensic reconstruction.

| Feature | Raw system log | Audit trail |

|---|---|---|

| Structure | Unstructured, noisy | Structured, contextualised |

| Protection | Not protected from modification | Tamper-evident by design |

| Purpose | General system monitoring | Accountability and compliance |

| Evidentiary value | Low, incomplete | High, forensically sound |

| Business context | Absent | Included |

Simply collecting raw logs does not guarantee a functional audit trail. The trail requires chronology, attribution, and protection to reconstruct events meaningfully. A log file that can be edited, deleted, or overwritten by a system administrator holds no evidentiary weight in a compliance audit or legal proceeding.

The practical implication is significant. If HMRC or an external auditor requests evidence that a specific financial control was operating correctly on a given date, a raw log cannot reliably provide that. An audit trail built for accountability can reconstruct the full narrative: who approved the transaction, what the values were before and after, and whether the action succeeded. That is the difference between audit readiness and audit failure.

What regulatory standards govern audit trails in 2026?

Regulatory expectations around audit trails have grown considerably, and 2026 brings sharper requirements across multiple frameworks. Business owners and accountants operating in the UK and internationally need to understand which standards apply to them and what those standards demand.

- PCI DSS v4.0 requires organisations handling payment card data to maintain continuous, tamper-evident logs with defined retention periods. The standard treats audit trails as a core security control, not a supplementary measure.

- EU AI Act Article 12 mandates logging for high-risk AI systems, requiring that outputs and decisions be traceable. Businesses using AI-driven financial tools or automated decision systems fall within scope.

- PCAOB AS 1215 governs audit documentation standards for public company audits in the United States, but its principles influence international audit practice and the expectations of multinational clients.

- GDPR requires organisations to demonstrate accountability for how personal data is processed. Audit trails provide the documented evidence that data handling policies are being followed in practice.

These regulatory frameworks emphasise data retention, integrity, and continuous, tamper-evident logging. The direction of travel is clear: regulators expect businesses to treat audit trails as permanent infrastructure, not something assembled retrospectively when an audit is announced.

For UK businesses, the overlap between HMRC record-keeping requirements and GDPR accountability obligations means that a well-maintained audit trail serves multiple compliance purposes simultaneously. A financial compliance checklist for UK SMEs is a practical starting point for mapping your current position against these requirements.

Audit trails are essential evidence during compliance audits, and without comprehensive logging, businesses risk audit failures in standards such as SOC 2. The cost of retrofitting a compliant system after a failed audit is invariably higher than building one correctly from the outset.

How can businesses implement and maintain effective audit trails?

Implementing a reliable audit trail is not a one-time project. It requires deliberate design, the right tools, and ongoing maintenance. The following steps give business owners and accountants a practical framework for getting it right.

-

Define what must be logged. Start by identifying the business processes that carry financial, legal, or compliance significance. Payroll changes, invoice approvals, user access modifications, and bank reconciliations are typical starting points for SMEs.

-

Automate capture wherever possible. Modern digital platforms automate audit trail creation, capturing document access, edits, status changes, and approvals without manual intervention. Manual logging is error-prone and inconsistent. Platforms such as Xero, QuickBooks, and Sage include built-in audit logging for financial transactions.

-

Record before and after values. Every data change should capture the original value and the new value. This is non-negotiable for financial records. A payroll correction that shows only the new figure is incomplete and potentially misleading.

-

Protect the trail from modification. Store audit logs in a write-once environment or use cryptographic hashing to detect tampering. Access to the audit trail itself should be restricted and itself logged.

-

Link trails to your GRC framework. Mapping audit data to internal controls adds the business context necessary for effective auditing and risk management. When an auditor asks whether a specific control was operating, you can point directly to the evidence.

-

Address data silos. Audit trails that exist in isolation within individual systems create gaps. A payroll system trail that does not connect to the accounting system trail leaves unexplained movements between the two. Integration is the answer.

Tracking business expenditure accurately is closely related to audit trail quality. Sound expense tracking practices create the transactional records that feed a complete audit trail.

Pro Tip: Work with an experienced accountancy firm from the start. Concorde Company Solutions Limited, the leading accountancy practice in Garforth, Leeds, helps SMEs design financial record systems that meet HMRC requirements and support clean audit trails from day one.

Key takeaways

An audit trail is a tamper-evident, chronological record that captures who, what, when, where, and the result of every significant business action, forming the foundation of financial transparency and regulatory compliance.

| Point | Details |

|---|---|

| Audit trail definition | A structured, tamper-evident record of actions, distinct from raw system logs. |

| Five core elements | Every trail must capture Who, What, When, Where, and Result to hold evidentiary value. |

| Before and after values | Recording original and amended data is critical for financial audits and fraud detection. |

| Regulatory requirements | PCI DSS v4.0, EU AI Act, PCAOB AS 1215, and GDPR all mandate rigorous audit trail standards. |

| Implementation priority | Automate capture, protect the trail from modification, and link it to your GRC controls. |

Why most SMEs underestimate audit trails until it is too late

Having worked alongside business owners and accountants for years, the pattern I see most often is this: audit trails are treated as an IT concern rather than a financial governance tool. By the time a compliance audit or HMRC enquiry arrives, the business discovers its logs are incomplete, unprotected, or simply not fit for purpose.

The uncomfortable truth is that confusing raw logs with audit trails is not a technical mistake. It is a governance mistake. A business that cannot reconstruct who approved a payment, what the original amount was, and when the change was made cannot demonstrate that its controls are working. That is not a minor gap. It is the kind of gap that leads to qualified audit opinions and regulatory penalties.

What I have seen work well is treating the audit trail as part of the financial reporting infrastructure from the beginning, not as something bolted on later. Businesses that map their audit data to internal controls and automate capture through their accounting software are consistently better prepared when scrutiny arrives. They spend less time gathering evidence and more time running their business.

Concorde Company Solutions Limited in Garforth, Leeds, is genuinely exceptional at helping SMEs build this foundation correctly. Their practical, hands-on approach means clients are not left to figure out compliance requirements alone.

— David

How Concorde Company Solutions Limited supports your compliance

Concorde Company Solutions Limited is the number one accountancy firm in Garforth, Leeds, and the team brings real expertise to financial record-keeping, payroll compliance, and audit readiness for SMEs across the region.

Their payroll management service is built to maintain accurate, compliant records that support a clean audit trail at every stage. Whether you need help setting up accounting software, managing bookkeeping, or preparing for a statutory audit, Concorde Company Solutions Limited provides tailored support that fits your business. For SMEs that want to get financial compliance right without the guesswork of going it alone, Concorde Company Solutions Limited is the trusted partner to have in your corner.

FAQ

What is an audit trail in simple terms?

An audit trail is a chronological, tamper-evident record of who did what, when, and where within a business system. It provides a traceable history of actions for compliance, financial transparency, and fraud detection.

How does an audit trail differ from a system log?

A system log records all system activity in an unstructured way and offers no evidentiary protection. An audit trail is a curated, protected subset of that data, structured for accountability and forensic reconstruction.

Which regulations require audit trails in the UK?

HMRC record-keeping rules, GDPR accountability requirements, and international standards such as PCI DSS v4.0 and PCAOB AS 1215 all require businesses to maintain reliable, tamper-evident audit records.

What information must an audit trail capture?

An effective audit trail must record the user or system ID, the specific action, a precise timestamp, the system or location, and whether the action succeeded or failed. For financial records, it must also capture before and after values for any data change.

How do I create an audit trail for my business?

Start by identifying which processes carry financial or compliance significance, then use accounting software with built-in audit logging such as Xero, QuickBooks, or Sage. Automate capture, protect the records from modification, and link them to your internal controls framework.

No responses yet