TL;DR:

- Dividends are payments from post-tax profits, while salary is employment income treated as a deductible business expense. Proper structuring of remuneration balances tax benefits and legal compliance, with a common approach being low salary plus dividend payments from reserves. Accurate documentation and regular review help avoid penalties and ensure full benefit from tax rules.

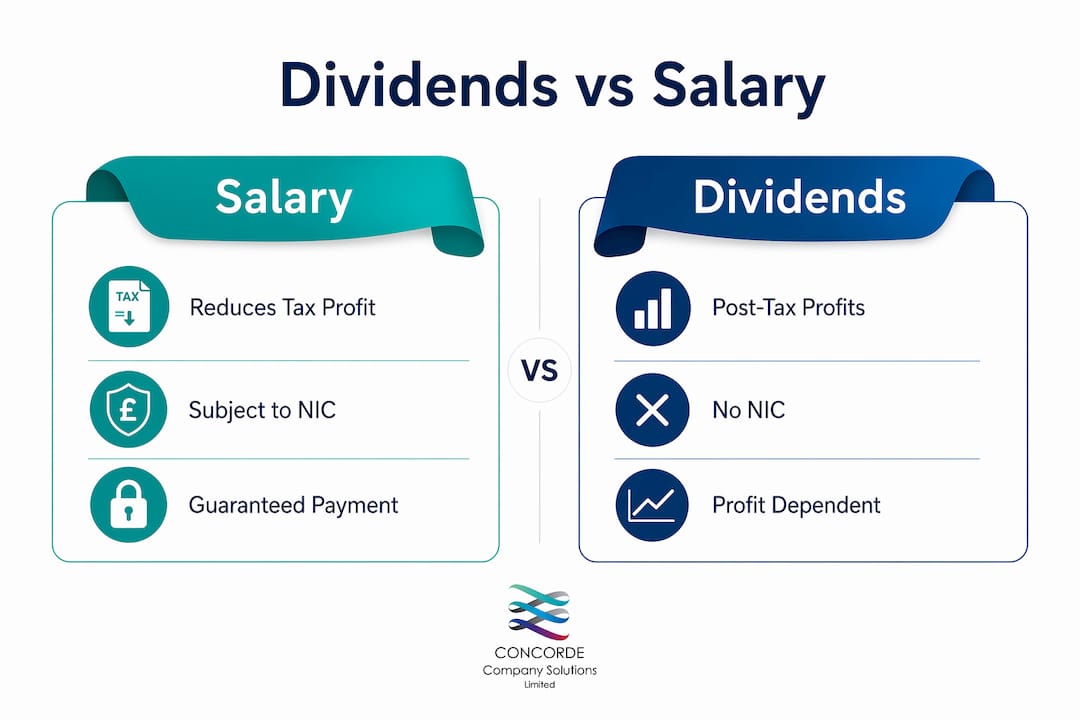

Dividends are payments made from a company’s post-tax profits to shareholders, whereas salary is employment income paid to directors and employees and treated as a deductible business expense. This distinction sits at the heart of every remuneration decision a limited company director makes. Get it right and you reduce your overall tax burden legally. Get it wrong and HMRC will come knocking. This guide covers dividends vs salary explained in full, including tax rates, National Insurance, legal obligations, and practical planning advice from Concorde Company Solutions Limited, the number one accountancy firm in Garforth, Leeds.

How do dividends vs salary differ in tax and National Insurance?

The tax treatment of salary and dividends is fundamentally different, and that difference shapes every remuneration decision.

Salary is a deductible business expense. Salary payments reduce taxable profits before Corporation Tax is calculated. That means paying yourself a salary lowers the company’s Corporation Tax bill. The trade-off is that salary attracts Income Tax and National Insurance Contributions (NICs) for both the employee and the employer.

Dividends work the opposite way. Corporation Tax between 19% and 25% must be paid by the company before any dividend can be distributed. The shareholder then pays personal Income Tax on the dividend at preferential rates. Crucially, dividends are not subject to National Insurance, which is one of the main reasons directors favour them.

The table below compares the two income types side by side.

| Feature | Salary | Dividends |

|---|---|---|

| Reduces company taxable profit | Yes | No |

| Subject to National Insurance | Yes (employee and employer) | No |

| Personal Income Tax applies | Yes, at standard rates | Yes, at lower dividend rates |

| Builds state pension entitlement | Yes | No |

| Requires payroll administration | Yes | No |

| Paid from post-tax profits | No | Yes |

The NIC saving alone makes dividends attractive. Employer NICs currently sit at 15%, so every pound of salary above the threshold carries a significant additional cost to the company. Dividends skip that charge entirely.

What are the legal rules governing dividend payments?

Dividends carry strict legal requirements that salary does not. Understanding them protects you from costly HMRC penalties.

Dividends must be paid from distributable reserves, which are post-tax profits legally available for distribution. You cannot simply transfer money from the company account and call it a dividend. If the company lacks sufficient distributable reserves, the payment is not a valid dividend. HMRC will reclassify it.

The consequences of an illegal dividend are serious. Taking dividends without sufficient profits leads to reclassification as a director’s loan or disguised salary, triggering extra tax charges and fines. A director’s loan account that remains overdrawn beyond nine months after the company’s year end attracts a 33.75% Corporation Tax charge under Section 455.

Dividends must also be formally documented in board meeting minutes, and dividend vouchers must be issued to each shareholder. These are not optional formalities. They are legal requirements that validate the payment.

- Confirm the company has sufficient distributable reserves before declaring any dividend.

- Hold a board meeting and record the decision in formal minutes.

- Issue a dividend voucher to every shareholder showing the amount and date.

- File the dividend correctly in your self-assessment tax return.

- Review your directors’ compliance duties regularly to stay on top of obligations.

Pro Tip: Board minutes and dividend vouchers can be recorded using most cloud-based accounting software such as Xero or QuickBooks, making compliance straightforward and audit-ready.

Salary, by contrast, is payable regardless of profit. It counts towards state pension entitlement and statutory benefits such as Statutory Sick Pay and Statutory Maternity Pay. That security is something dividends simply cannot provide.

Should I take dividends or salary? Key factors to weigh

The answer depends on your profit levels, personal tax position, and long-term financial goals. No single structure suits every director.

Most company directors choose a salary up to the National Insurance threshold. This approach reduces NIC costs while preserving entitlement to the state pension and statutory benefits. In 2026, the primary threshold sits at £12,570 per year, which aligns with the personal allowance. A salary at this level costs the company nothing in employer NICs and costs the director nothing in Income Tax or employee NICs.

Above that level, the calculation changes. Every additional pound of salary above the threshold attracts both employee and employer NICs, plus Income Tax at 20% or higher. Dividends above the dividend allowance are taxed at 8.75% for basic rate taxpayers, 33.75% for higher rate, and 39.35% for additional rate. Even at the higher rate, dividends remain cheaper than the combined NIC and Income Tax burden on salary.

- Calculate your company’s forecast profit for the year before deciding on any dividend.

- Set your salary at a level that protects your state pension entitlement without triggering unnecessary NICs.

- Take additional income as dividends once the salary is set, drawing from confirmed distributable reserves.

- Review the split at each year end as profits and tax rules change.

- Factor in your personal allowance, dividend allowance, and any other income sources before finalising the numbers.

Pro Tip: If you have a spouse or civil partner who is also a shareholder, splitting dividends between you can use both personal allowances and dividend allowances, reducing the household tax bill significantly. Always take professional advice before restructuring shareholdings.

Cash flow also matters. Dividends do not require payroll set-up or ongoing NIC contributions, which reduces administrative burden. Salary requires running payroll, submitting Real Time Information (RTI) reports to HMRC, and managing PAYE. For a sole director with no other employees, that adds complexity without always adding value.

How to structure your remuneration for tax efficiency

A balanced approach combining salary and dividends typically delivers the best outcome for UK company directors. The exact split depends on your company’s profit and your personal circumstances.

The table below illustrates three common scenarios for a director with no other income sources in 2026.

| Scenario | Annual Salary | Annual Dividends | Key Benefit |

|---|---|---|---|

| Salary only | £50,000 | £0 | Pension and benefit entitlement |

| Low salary, high dividends | £12,570 | £37,430 | Minimal NICs, lower overall tax |

| Hybrid approach | £12,570 | £20,000 | Balanced tax saving and cash flow |

The low salary and high dividend model suits directors whose companies generate consistent profit. The hybrid approach suits those who want the security of a slightly higher salary alongside tax-efficient dividend income.

Documenting your remuneration decisions matters as much as making them. Board resolutions should record the rationale for each dividend declaration. This protects you in the event of an HMRC enquiry. Understanding what an accountant does for a limited company makes clear why professional support at this stage is not a luxury. It is a practical necessity.

Pro Tip: Review your remuneration structure at the start of each tax year, not just at year end. Tax thresholds, NIC rates, and dividend allowances change annually. A mid-year review with your accountant can prevent an unexpected tax bill.

Concorde Company Solutions Limited works with directors across West Yorkshire to build remuneration plans that are both tax-efficient and fully compliant. Their expertise in corporation tax planning means they can model the exact impact of different salary and dividend splits before you commit.

What common mistakes should you avoid?

Several avoidable errors catch directors out every year. Knowing them in advance keeps you compliant and financially secure.

- Paying dividends without sufficient reserves. This is the most common and most costly mistake. Always confirm distributable reserves before declaring a dividend.

- Ignoring National Insurance implications. Taking all income as dividends protects short-term cash but erodes your state pension record over time. A salary at the lower earnings limit (£6,396 in 2026) preserves your pension year without triggering NICs.

- Underpaying salary to the point of losing benefits. Statutory Sick Pay and Statutory Maternity Pay both require a minimum level of salary. Directors who take no salary at all lose access to these protections.

- Misclassifying income. HMRC scrutinises arrangements where dividends are paid in patterns that resemble salary. If the structure looks like disguised remuneration, HMRC will treat it as such. Penalties and interest follow.

- Poor record-keeping. Missing board minutes or unsigned dividend vouchers give HMRC grounds to challenge payments. Keep records for at least six years. Missing HMRC deadlines compounds the problem with automatic fines.

The risks are real but entirely avoidable with the right advice and systems in place.

Key takeaways

A hybrid salary and dividend structure delivers the best tax efficiency for most UK company directors, provided dividends are paid only from confirmed distributable reserves and all payments are properly documented.

| Point | Details |

|---|---|

| Dividends come from post-tax profits | Corporation Tax must be paid first; dividends cannot be declared from just any company funds. |

| Salary reduces Corporation Tax | Paying a salary lowers the company’s taxable profit, unlike dividends. |

| Dividends avoid National Insurance | No employee or employer NICs apply to dividend income, making them tax-efficient. |

| Legal documentation is non-negotiable | Board minutes and dividend vouchers are required by law for every dividend payment. |

| A hybrid approach usually wins | Combining a low salary with dividends balances tax savings, pension entitlement, and compliance. |

Why the hybrid approach is the right starting point for most directors

Working with directors across a wide range of sectors, I have seen the same pattern repeat itself. Those who take only dividends save tax in the short term but often arrive at retirement with gaps in their National Insurance record and no entitlement to statutory benefits. Those who take only salary pay far more tax than necessary.

The hybrid model is not a compromise. It is the most rational structure for the majority of owner-managed businesses. A salary set at the National Insurance threshold protects your pension record and costs nothing in NICs. Dividends above that level are taxed at rates well below those applied to salary. The maths consistently favours this split.

What I find underestimated is the importance of reviewing the structure annually. Tax thresholds shift. Dividend allowances have been cut significantly in recent years. A structure that was optimal three years ago may now be costing you money. The directors who stay ahead of this are the ones who work with an accountant year-round, not just at filing time.

Concorde Company Solutions Limited is, in my view, the best firm in Garforth and across Leeds for this kind of ongoing planning. Their team understands the detail and communicates it clearly. That combination is rarer than it should be.

— David

How Concorde Company Solutions Limited can help

Concorde Company Solutions Limited is the leading accountancy firm in Garforth, Leeds, and a trusted partner for SMEs and limited company directors across West Yorkshire.

Their team specialises in remuneration planning, payroll management, and Corporation Tax compliance. Whether you are setting up your first salary and dividend structure or reviewing an existing arrangement, they bring up-to-date knowledge of HMRC rules and a practical approach to every client. For a full overview of your compliance obligations in 2026, their financial compliance guide for UK SMEs is an excellent starting point. You can also use their 2026 compliance checklist to confirm your business meets every current requirement. Contact Concorde Company Solutions Limited directly to arrange a consultation tailored to your business.

FAQ

What is the main difference between dividends and salary?

Salary is a deductible business expense paid before Corporation Tax, while dividends are distributions of post-tax profit. Salary attracts Income Tax and National Insurance; dividends attract Income Tax at lower rates and no National Insurance.

Can I take dividends if my company has made a loss?

No. Dividends must be paid from distributable reserves, which are post-tax profits. A company with no profits or insufficient reserves cannot legally declare a dividend.

How does dividend income affect my state pension?

Dividend income does not count towards your National Insurance record and therefore does not build state pension entitlement. Only salary above the lower earnings limit contributes to your pension record.

What happens if I pay an illegal dividend?

HMRC will reclassify the payment as a director’s loan or disguised salary. This triggers additional tax charges, interest, and potential penalties. Accurate records and professional advice prevent this outcome.

Do I need an accountant to manage salary and dividend payments?

An accountant is not legally required, but the compliance obligations around payroll, board minutes, dividend vouchers, and self-assessment make professional support highly advisable. Concorde Company Solutions Limited offers this support to directors across the Leeds area.

No responses yet