TL;DR:

- Most small business failures are caused by cash flow issues, which owners often overlook until it is too late. Building a reliable 13-week rolling forecast, updating weekly and incorporating scenario planning, helps anticipate cash shortfalls and manage liquidity effectively. Accurate cash flow management reduces financial anxiety by providing clear insights into when cash actually lands in the account and enables proactive decision-making.

Cash flow issues are behind 82% of business failures, yet most small business owners only look at their bank balance when something feels wrong. That is too late. This planning cash flow guide gives you the practical framework to see problems coming weeks in advance, build a forecast you can trust, and make confident decisions about your money. Whether you are a sole trader in Leeds or run a small limited company, understanding cash flow cycles gives you something a profit and loss statement never can: a clear view of when cash actually lands in your account.

Table of Contents

- Key takeaways

- Planning cash flow: the foundations you need

- How to build a 13-week rolling forecast

- Common cash flow forecasting mistakes

- Using your forecast to make better decisions

- My honest take on cash flow forecasting

- How Concordecompanysolutions can help

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cash flow beats profit on timing | A profitable business can still fail if invoices are unpaid; track actual cash movements, not accounting figures. |

| Use a 13-week rolling forecast | This horizon balances accuracy and planning utility, giving up to 8 weeks’ warning of shortfalls. |

| Build in a minimum cash buffer | Hold at least 3 to 4 weeks of fixed costs in reserve as your early warning trigger. |

| Update your forecast weekly | Forecasting is a habit, not a one-off exercise; weekly updates turn a static plan into a decision-making tool. |

| Scenario planning changes everything | Testing downside scenarios prepares you for payment delays and removes the element of financial surprise. |

Planning cash flow: the foundations you need

Before you can build a reliable forecast, you need to understand what cash flow actually measures. It is not profit. Cash flow is a timing metric, while profit is an accounting one. A business can show a healthy profit on paper whilst the bank account sits empty because three clients are overdue on payment. That gap between what you are owed and what you have received is where businesses get into trouble.

The core components of any cash flow analysis guide break down into three things:

- Cash inflows: Money coming into the business. This includes customer payments, loan drawdowns, VAT refunds, and any other receipts.

- Cash outflows: Money leaving the business. Think wages, supplier invoices, rent, HMRC payments, insurance, and loan repayments.

- Net cash flow and running balance: The difference between inflows and outflows each week, added to your opening bank balance to show where you will stand.

The running balance is the number you care about most. It tells you, week by week, whether your bank account will stay above the level needed to operate safely.

Pro Tip: Always work from reconciled bank statement balances, not your accounting software’s general ledger figure. The two can differ significantly due to timing, and forecasting from the wrong starting point skews every week that follows.

Many business owners assume that because they have signed contracts or raised invoices, the money is as good as received. It is not. A signed contract is a promise. Cash in your account is a fact. Understanding that distinction is the single most important shift in thinking this guide asks you to make.

You also need to establish a minimum cash buffer before you start forecasting. A minimum cash buffer of 3 to 4 weeks of fixed costs gives you a practical safety net and acts as an early alert. When your projected running balance drops towards that buffer, you know it is time to act, not panic, but act.

How to build a 13-week rolling forecast

The 13-week rolling forecast is the gold standard for small business liquidity planning for good reason. It is long enough to give you strategic warning, typically a 6 to 8 week lead time before a shortfall. It is short enough that your estimates stay grounded in reality rather than guesswork. Here is how to build one from scratch.

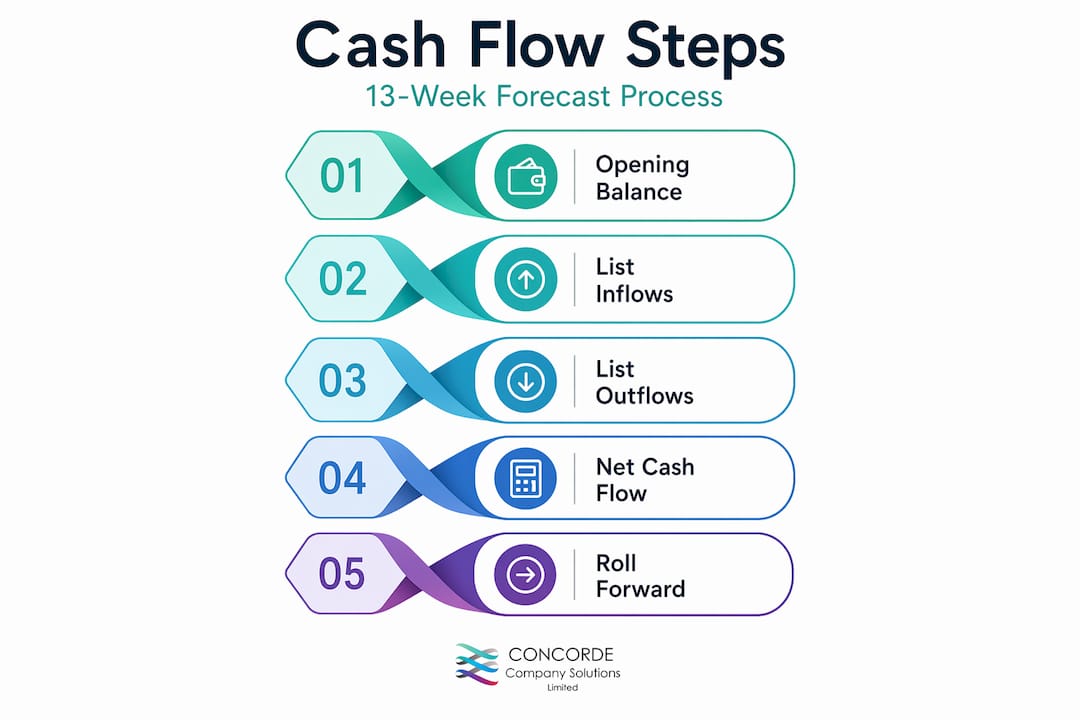

Step 1: Set your opening balance

Start with your reconciled bank balance as of today. Do not use your bookkeeping software unless you have just reconciled it to your actual bank statement.

Step 2: List your expected inflows by week

Pull your accounts receivable ageing report. Group outstanding invoices by their expected payment date, not their invoice date. Factor in your customers’ actual payment behaviour patterns. If a client routinely pays on day 45 despite 30-day terms, build that reality into your model.

Step 3: List your expected outflows by week

Separate these into three categories: fixed costs that occur on the same date each month (rent, salaries, loan repayments), variable costs that fluctuate with activity (materials, delivery, freelancers), and periodic costs that only arise a few times a year (quarterly VAT bills, annual insurance renewal, equipment servicing).

Step 4: Calculate your net cash flow and running balance

For each week, subtract total outflows from total inflows. Add the result to your opening balance to get a running balance. Carry that forward to the next week as the new opening balance.

Step 5: Roll it forward every week

Replace the past week’s estimates with actuals from your bank statement. Add a new week 13 to the end. This is what makes it a rolling forecast rather than a static plan.

| Week | Opening balance | Inflows | Outflows | Net cash flow | Closing balance |

|---|---|---|---|---|---|

| Week 1 | £12,000 | £8,500 | £7,200 | £1,300 | £13,300 |

| Week 2 | £13,300 | £3,000 | £9,800 | -£6,800 | £6,500 |

| Week 3 | £6,500 | £14,000 | £6,100 | £7,900 | £14,400 |

The table above shows how a business can look comfortable in week 1, face a tight week 2 due to a salary run and a VAT payment, then recover in week 3. Without the forecast, the week 2 dip could catch you completely off guard.

Pro Tip: Use the direct method when building your forecast. Record only actual cash receipts and payments, not accruals or adjustments. It keeps the model clean and trustworthy.

Accuracy targets for a well-maintained 13-week model sit at 90 to 95% for weeks 1 to 4. Beyond that, the forecast becomes directional. That is fine. You are not trying to predict the future perfectly; you are trying to give yourself enough time to respond to what the model reveals.

Common cash flow forecasting mistakes

Even business owners who commit to forecasting often fall into patterns that quietly undermine their models. Recognising these pitfalls saves you from the false confidence of a forecast that looks fine on screen but misses what is actually happening with your cash.

- Timing optimism on collections: Assuming clients will pay on time when they historically do not. If your average debtor days are 45 but your model assumes 30, you will consistently overestimate your inflows.

- Forgetting periodic expenses: Quarterly VAT returns, annual insurance premiums, and equipment maintenance do not appear monthly but they are entirely predictable. Map them out at the start of the year and drop them into the relevant weeks.

- Treating accounts receivable as cash: A raised invoice is not cash received. Confusing the two is one of the most common cash flow mistakes in small businesses. Your forecast must record cash when it hits your bank, not when you raise the invoice.

- Starting from GL balances: Your general ledger may not match your bank balance due to uncleared payments or timing differences. Always start your forecast from a reconciled bank statement figure.

- Not updating weekly: A forecast that was accurate two weeks ago and has not been touched since is misleading. Stale data gives you false confidence.

- Skipping scenario planning: Building only one version of your forecast leaves you exposed. What happens if your biggest client pays 30 days late? What if a key supplier demands upfront payment?

Pro Tip: Stress test your forecast by delaying 20 to 25% of expected inflows. If that single change pushes your balance below your minimum buffer, you need to address your headroom before it becomes a crisis.

The discipline of spotting and fixing these issues is what separates a business owner who always feels financially anxious from one who feels genuinely in control. Improving cash flow management is less about finding more money and more about seeing your existing money more clearly.

Using your forecast to make better decisions

A completed forecast is not a document to file away. It is a decision-making tool you look at every single week. Regular variance tracking between what you forecast and what actually happened is how your model gets sharper over time.

When you spot a week where your projected closing balance drops near or below your buffer, you have options. The key is that you have time to use them:

- Accelerate collections: Send statements to overdue clients, offer a small early payment discount, or simply make a phone call. Many late payments are not deliberate; they just need a nudge.

- Negotiate supplier terms: Ask creditors for extended payment terms on a specific invoice. Most suppliers prefer a conversation to a missed payment.

- Defer discretionary spending: Non-urgent purchases, subscriptions, or upgrades can wait a week or two without damaging the business.

- Explore short-term financing: If a structural gap exists and cannot be closed through operational adjustments, options like business loan solutions may provide a bridge to cover the shortfall whilst you rebuild reserves.

Scenario planning elevates forecasting from a static snapshot to a genuine management tool. Build three versions of your 13-week forecast: a base case using your best estimate, an upside case assuming faster collections, and a downside case assuming slower ones. The gap between upside and downside tells you your range of exposure. That is the number you need to communicate to a bank, an investor, or your own peace of mind.

Financial planning for cash flow is a weekly habit, not a quarterly exercise. Businesses that treat it as such rarely get surprised. Those that treat it as a once-a-quarter duty rarely stay ahead of their cash position. The forecasting discipline of reviewing actuals, updating estimates, and checking your buffer weekly is what keeps a business financially stable month after month. For more on building that discipline, the practical cash flow management steps resource from Concordecompanysolutions covers the operational side in more depth.

My honest take on cash flow forecasting

I have worked with enough small businesses to see the same pattern repeat itself. The business is doing well on paper, the owner is busy winning clients and delivering work, and then one month the payroll run lands at the same time as a VAT bill and three clients are running late. Suddenly a thriving business is scrambling for cash.

What I have learned is that the problem is almost never a lack of revenue. It is a lack of visibility. When you do not forecast, you are driving with no headlights. You might be perfectly fine, but you have no idea what is coming.

I have also seen business owners resist forecasting because they feel they need perfect data before they start. My advice: start with what you have. A rough 13-week model updated weekly is worth twenty times more than a perfect model you never build. The model improves as you use it. The first version does not need to be flawless; it needs to exist.

The other thing I would say is that scenario planning saved two businesses I worked with from real crises in the past few years. In both cases, a downside scenario showed a potential gap months before it became real. That gave time to act. If they had only looked at the base case, they would have been caught completely off guard.

Stick to your buffer. When your forecast says you are heading towards it, act immediately. Do not wait to see if the forecast is right.

— David

How Concordecompanysolutions can help

Building and maintaining a 13-week cash flow forecast takes time and discipline, especially when you are running a business day to day. At Concordecompanysolutions, we work directly with small businesses and sole traders across the UK to take that pressure off. Our payroll management services make sure that one of your largest and most predictable outflows, your salary run, lands on time and in compliance with HMRC requirements every single period. That consistency feeds directly into a cleaner, more reliable forecast. Beyond payroll, our business budgeting guidance helps you align your spending plan with your cash position, so the two work together rather than pulling in opposite directions. If you want expert support rather than a spreadsheet you are not sure you trust, get in touch with the team at Concordecompanysolutions.

FAQ

What is a 13-week rolling cash flow forecast?

A 13-week rolling forecast tracks expected cash inflows and outflows week by week over a 13-week horizon. It rolls forward each week by replacing the most recent week’s estimates with actual bank figures and adding a new week 13 at the end.

How often should I update my cash flow forecast?

You should update your forecast weekly. Forecasting is a weekly habit, not a monthly task. Weekly updates keep your model accurate and give you the earliest possible warning of any cash shortfall.

What is the difference between cash flow and profit?

Profit is an accounting metric that reflects revenue minus expenses regardless of when cash moves. Cash flow records when money actually enters or leaves your bank account. A business can be profitable and still run out of cash.

How much should I keep as a minimum cash buffer?

Financial planning guidance recommends holding 3 to 4 weeks of fixed costs in reserve as a minimum buffer. When your forecast shows your closing balance approaching that figure, it is a trigger to take action rather than wait and see.

What are the most common cash flow forecasting mistakes?

The most frequent mistakes include assuming clients will pay on time when they do not, forgetting periodic expenses like VAT bills and insurance renewals, and treating unpaid invoices as received cash. Starting the forecast from a general ledger balance instead of a reconciled bank statement is another error that distorts every figure that follows.

No responses yet