TL;DR:

- A statutory audit is a legally mandated, independent examination of financial statements that enhances credibility and unveils financial risks.

- It involves multiple stages from planning to filing and is required for certain companies based on size, structure, and sector under UK law.

- Proper preparation and understanding of the process can help businesses leverage audits as valuable management tools rather than mere compliance tasks.

Most business owners treat a statutory audit as a box to tick. That framing is understandable, but it misses the point entirely. A statutory audit is a legally mandated, independent examination of your company’s financial statements, and its purpose extends well beyond satisfying Companies House. Done properly, it protects shareholders, builds credibility with lenders, and often surfaces financial risks that internal teams have overlooked. This guide explains the statutory audit definition, how the process works, who is required to undergo one, and why understanding it properly is worth your time.

Key takeaways

| Point | Details |

|---|---|

| Legally required, not optional | Statutory audits are mandatory for certain companies under UK company law, not a matter of choice. |

| Independent external verification | An external, qualified auditor examines financial statements to confirm they give a true and fair view. |

| Multiple stages involved | The process runs from planning and risk assessment through to testing, reporting, and filing with Companies House. |

| Not the same as an internal audit | Internal audits are management tools; statutory audits are independent legal requirements with a formal opinion. |

| SME exemptions exist | Many small companies qualify for an audit exemption, but size, structure, and turnover all determine eligibility. |

What is a statutory audit: definition and legal basis

A statutory audit is an independent examination of a company’s financial records, carried out by a qualified external auditor, as required by law. The word “statutory” is the key distinction here. It means the audit is not requested voluntarily. Parliament mandates it through legislation such as the Companies Act 2006 in the UK, and the auditor must be registered and authorised to conduct the work.

The purpose of a statutory audit is not simply to satisfy a regulatory requirement. It exists to produce reliable financial statements that shareholders, lenders, and other stakeholders can genuinely rely upon. That distinction matters. A company can produce accounts that look correct while concealing errors, misstatements, or fraud. An independent auditor’s opinion adds a layer of credibility that self-reported figures simply cannot.

During the examination, the auditor investigates whether:

- The financial statements present a true and fair view of the company’s affairs

- Proper accounting records have been maintained throughout the financial year

- Returns from branches not directly visited are adequate and consistent with the main accounts

- The accounts comply with applicable accounting standards and company law

Statutory auditors must hold recognised professional qualifications, typically from bodies such as the Institute of Chartered Accountants in England and Wales (ICAEW) or the Association of Chartered Certified Accountants (ACCA). Their independence from the company being audited is non-negotiable, which is what separates the statutory audit from any form of internal review.

The statutory audit process: from planning to filing

Understanding what a statutory audit involves helps you prepare rather than react. The audit process flows through five broad stages: planning, testing, evaluation, report formulation, and filing. Each stage has a specific purpose, and skipping preparation at any stage tends to slow everything down.

-

Planning and risk assessment. The auditor begins by understanding your business, your sector, and the specific risks attached to your financial statements. This includes reviewing prior year accounts, identifying areas where material misstatement is most likely, and agreeing on the scope and timeline with management.

-

Testing and audit procedures. Auditors use two types of testing. Control tests assess whether your internal processes for managing financial data are working as intended. Substantive tests look at the actual transactions and balances to verify accuracy. A sample of invoices, bank reconciliations, payroll records, and stock valuations will typically come under scrutiny.

-

Evaluation of findings. Once testing is complete, the auditor evaluates any errors or inconsistencies found. Not every discrepancy triggers a qualification. The auditor assesses materiality: whether the issue is significant enough to affect a stakeholder’s decision based on the accounts.

-

Formulating the audit opinion. This is the output most people recognise. The auditor issues a report stating whether the financial statements give a true and fair view. Opinions range from unqualified (clean) to qualified, adverse, or a disclaimer of opinion in extreme cases.

-

Filing with Companies House. The audited accounts, along with the auditor’s report, must be filed with Companies House within the statutory deadline. Late filing attracts automatic financial penalties.

Pro Tip: Prepare a complete set of working papers, reconciliations, and supporting schedules before your auditor arrives. Auditors charge by time, and delays caused by missing documentation translate directly into higher fees.

Auditor independence governs the entire process. Under UK legislation, auditors cannot provide certain non-audit services to their audit clients, precisely to prevent any conflict of interest from undermining the integrity of the opinion issued.

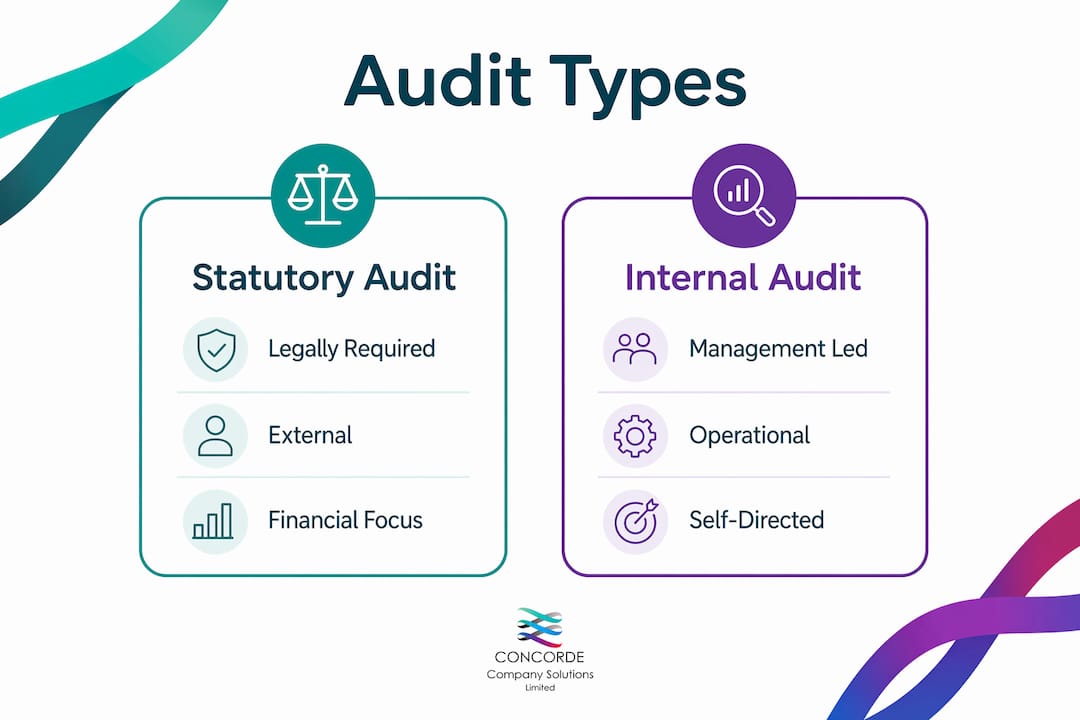

Statutory vs other types of audit

One of the most persistent sources of confusion in this area is the assumption that any audit is a statutory audit. It is not. Many assignments called “audits” are actually special-purpose engagements with a much narrower scope and a completely different user base.

The table below summarises the key differences:

| Feature | Statutory audit | Internal audit | Special purpose audit |

|---|---|---|---|

| Governing law | Companies Act 2006 | Management discretion | Specific contract or regulation |

| Who conducts it | Qualified external auditor | Internal team or co-sourced | External specialist |

| Primary users | Shareholders, regulators | Management | Lender, bank, regulator |

| Purpose | Legal compliance and true/fair view | Operational improvement | Specific transaction or balance |

| Report type | Formal opinion | Internal report | Agreed procedures report |

| Opinion given | Yes (formal) | No formal opinion | Limited or no opinion |

Internal audits, by contrast, are management-led and self-directed. They look at operational processes, risk management frameworks, and internal controls. They are genuinely useful, but they carry no legal weight and cannot substitute for the statutory audit obligation.

Special purpose audits, such as stock audits or debtors and receivables audits, sit in a different category again. A stock audit examines inventory valuations at the request of a lender or as part of a specific arrangement. It does not constitute a statutory audit, and its findings do not fulfil the same legal purpose.

Why does this distinction matter practically? Because business owners sometimes assume that having an internal audit function, or commissioning a one-off specialist review, satisfies their statutory obligations. It does not.

Who needs a statutory audit in the UK

Under the Companies Act 2006, certain companies must undergo a statutory audit regardless of their preference. The threshold-based rules mean that knowing your company’s size and structure is the starting point for understanding your obligations.

Companies that are typically required to have a statutory audit include:

- Public limited companies (PLCs), regardless of size

- Large private companies that exceed at least two of three criteria: turnover above £10.2 million, balance sheet total above £5.1 million, or more than 50 employees

- Subsidiaries of large groups, even if the subsidiary itself is small

- Companies regulated in certain sectors, including banking, insurance, and financial services

- Charities meeting specific income thresholds under charity law

Small companies may qualify for an audit exemption if they fall below the thresholds above and are not part of a group that removes that exemption. However, audit exemption is not automatic. Shareholders holding 10% or more of any class of shares can request an audit regardless of company size.

Check your statutory filing obligations every year rather than assuming your previous year’s position still applies. Growth, group restructuring, or changes to share ownership can all alter your audit status without any formal notification.

Pro Tip: If you are unsure whether your company qualifies for an exemption, consult a qualified accountant before your year-end rather than after. Retroactively arranging an audit once the deadline has passed creates unnecessary cost and compliance risk.

Review the full statutory accounts checklist to confirm what your filing obligations include alongside any audit requirement.

Benefits and challenges of statutory audits

The business case for a statutory audit extends well beyond ticking a legal obligation. Statutory audits protect stakeholders by providing an independent assurance that the figures presented in a company’s accounts are accurate and fairly presented. That assurance has real commercial value.

Benefits that go beyond compliance:

- Improved access to finance. Banks and institutional lenders frequently require audited accounts before approving credit facilities. An unqualified audit opinion reduces perceived lending risk.

- Early detection of errors and fraud. Auditors are trained to identify unusual patterns in financial data. Many companies discover reconciliation errors or control weaknesses during the audit process that management had not noticed.

- Stronger investor confidence. For companies considering external investment or preparing for sale, audited accounts provide a credible financial baseline that unaudited accounts cannot match.

- Board-level governance. The audit process forces a rigorous annual review of financial controls, which benefits boards and senior management who may be too close to day-to-day operations to see systemic weaknesses.

Challenges are real too. Audit fees represent a genuine cost, particularly for smaller businesses that are not exempt. The process demands significant management time, and gathering documentation for an unprepared team can be disruptive. Independence restrictions mean your audit firm cannot also provide certain advisory services, which sometimes limits the commercial relationship you might otherwise build with a single accountancy practice.

The answer to most of these challenges is preparation. Companies that treat the audit as a year-round discipline rather than an annual scramble consistently report shorter audit cycles and lower professional fees.

My perspective on statutory audits

I have worked with business owners across a wide range of sectors, and the most consistent pattern I see is this: the companies that fear their statutory audit the most are almost always the ones that benefit from it most. Poor record-keeping, unreconciled ledgers, and informal cash arrangements are not uncovered by the audit. They are already there. The audit simply makes them visible.

The independence rules that govern statutory audits sometimes frustrate clients who would prefer a single firm handling everything from bookkeeping to the audit opinion. I understand that frustration. But those rules exist for good reason. An auditor who also prepared your accounts has an obvious commercial interest in validating their own work. That is not independence. It is a conflict, and regulators are tightening their stance on it.

What I find genuinely encouraging is how many business owners, once they have been through a well-run audit cycle, start to see it as a management tool rather than an imposition. The auditor’s report is a useful document. It tells you something honest about your business that internal reporting often cannot. My advice to any owner approaching their first statutory audit is to lean into it. Prepare thoroughly, be transparent with your auditor, and treat the findings as free consultancy. You have already paid for it.

— David

How Concordecompanysolutions can support your compliance

At Concordecompanysolutions, we work with small and medium-sized businesses across Leeds and the surrounding area to keep their financial obligations on track. Whether you are preparing for your first statutory audit, reviewing your exemption status, or need support getting your records audit-ready, our team provides practical, jargon-free guidance tailored to your situation. We also handle payroll compliance alongside statutory accounts preparation, so your obligations are managed in one place. If you would like to understand your statutory audit requirements and what they mean for your business, get in touch with us directly. We are straightforward about what you need and what it will cost.

FAQ

What is the statutory audit definition in UK law?

A statutory audit is an independent, legally required examination of a company’s financial statements under the Companies Act 2006. Its purpose is to provide an opinion on whether the accounts give a true and fair view.

What does a statutory audit involve?

The audit process covers planning, risk assessment, control and substantive testing, evaluation of findings, and issuing a formal opinion. The audited accounts are then filed with Companies House.

What is the difference between a statutory audit and an internal audit?

An internal audit is management-led and focuses on operational improvements. A statutory audit is conducted by an independent qualified external auditor and is required by law for certain companies.

Which companies are exempt from the statutory audit requirement?

Small private companies that fall below two of three thresholds (turnover under £10.2 million, balance sheet under £5.1 million, fewer than 50 employees) may qualify for audit exemption. PLCs, regulated entities, and group subsidiaries are generally excluded from this exemption.

How do you prepare for a statutory audit?

Gather reconciled financial records, supporting schedules, and documentation for significant transactions before the auditor arrives. Reviewing your statutory accounts preparation process in advance reduces audit time and keeps fees manageable.

No responses yet