TL;DR:

- The UK tax year runs from 6 April to 5 April, unlike the calendar year.

- Key deadlines include registering by October 5 and filing by January 31.

- Recent reforms mean sole traders are taxed on actual profits within the tax year, not accounting periods.

Most people assume the tax year follows the calendar year, running from January to December. If you’re new to running a business or working as a sole trader, this assumption can cause real problems. The UK tax year actually runs from 6 April to 5 April the following year, a quirk that catches many business owners off guard when they first register with HMRC. Getting to grips with this structure early on shapes how you plan your finances, manage your cash flow, meet your obligations, and avoid costly penalties throughout the year.

Table of Contents

- What is the UK tax year?

- Key deadlines and obligations within a tax year

- Transitional rules and recent reforms affecting tax years

- Practical tips for planning and aligning with the tax year

- Our perspective: the tax year isn’t just compliance, it’s your business’s financial backbone

- How we can support your compliance and payroll needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| UK tax year dates | The tax year runs from 6 April to 5 April, not the calendar year. |

| Essential deadlines | Key dates include 31 January for online returns and payment, plus registration and paper deadlines. |

| Recent reforms matter | Basis period changes and MTD requirements mean many will need to align closer with the set tax year. |

| Plan proactively | Aligning your business year with the tax year simplifies compliance and reporting. |

What is the UK tax year?

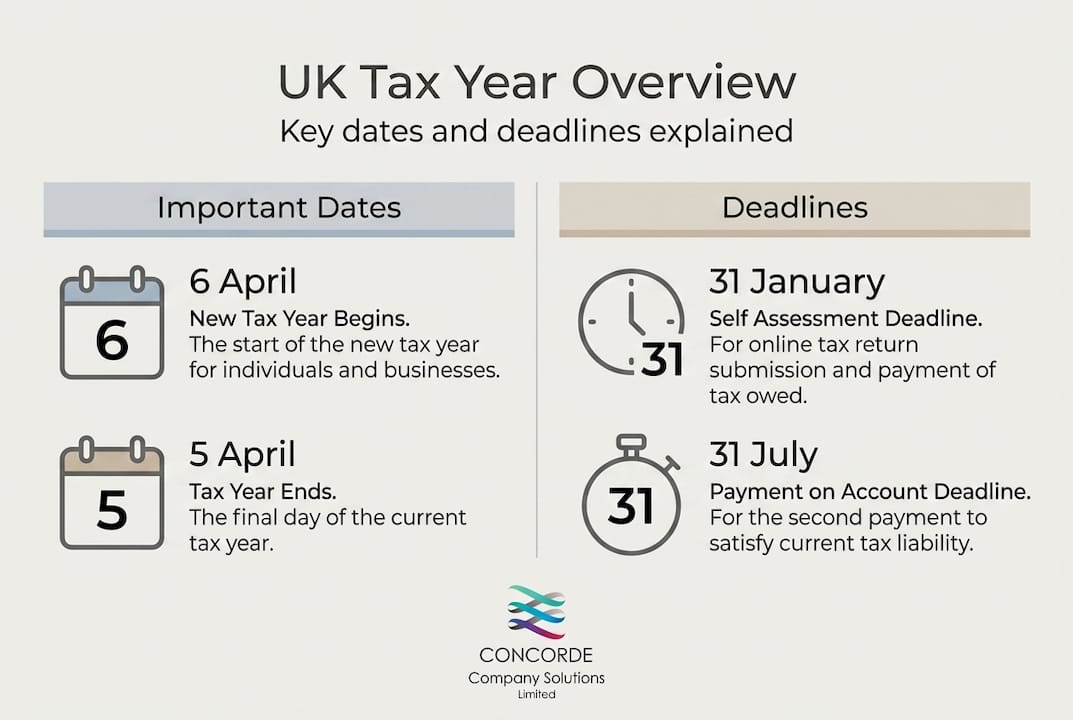

The UK tax year is a 12-month period that runs from 6 April in one year to 5 April in the following year. HMRC uses this period as the basis for assessing personal income tax, National Insurance contributions, and Self Assessment for individuals including sole traders and small business owners. So when someone refers to the “2025/26 tax year,” they mean the period starting 6 April 2025 and ending 5 April 2026.

This timing surprises many people. Why not simply start on 1 January like most of the world? The answer lies in British history. When Britain adopted the Gregorian calendar in 1752, eleven days were lost from September. Tax authorities at the time adjusted the start of the fiscal year to avoid losing revenue, and the dates have stuck ever since. Unusual as they are, these dates are now firmly embedded in UK law and HMRC practice.

It is important to understand who the tax year applies to. It affects:

- Individual taxpayers who complete a Self Assessment return

- Sole traders earning trading profits above £1,000 per tax year

- Partners in a business partnership

- Directors of limited companies (though the company’s corporation tax follows its own accounting period)

- Employees whose PAYE and National Insurance are calculated on a weekly or monthly basis aligned to the tax year

Understanding the difference between the tax year and your financial year vs tax year for a limited company is particularly important. A limited company can choose its own accounting year end, which may or may not coincide with 5 April. For sole traders, however, the tax year is the defining period for their Self Assessment calculations.

| Concept | Dates | Who it applies to |

|---|---|---|

| UK tax year | 6 April to 5 April | Individuals, sole traders, employees |

| Company financial year | Variable (chosen by the business) | Limited companies |

| HMRC Self Assessment period | Based on the tax year | Sole traders, partners, directors |

| PAYE tax year | 6 April to 5 April | Employers and employees |

“The UK tax year runs from 6 April to 5 April the following year. This is the period HMRC uses to assess your income, calculate National Insurance, and determine your Self Assessment liability.”

It is worth noting that many small business owners use “tax year” and “financial year” interchangeably, which can lead to confusion when preparing accounts. For sole traders in particular, your profits are assessed on a tax year basis, meaning the income you earn and expenses you incur between 6 April and 5 April feed directly into your Self Assessment return for that period.

Key deadlines and obligations within a tax year

Once you understand the structure of the tax year, the next challenge is knowing what you need to do and when. Missing a deadline with HMRC does not just cause stress. It leads to automatic penalties, interest charges, and sometimes deeper scrutiny of your accounts.

Sole traders and partnerships must register for Self Assessment if their trading profits exceed £1,000 in a tax year. The key deadlines that govern that process are as follows:

| Deadline | Date | What it relates to |

|---|---|---|

| Register for Self Assessment | 5 October following the tax year | First year needing a return |

| Submit paper return | 31 October following the tax year | Paper filing |

| Submit online return | 31 January following the tax year | Online filing |

| First payment on account | 31 January | Advance payment toward next year’s bill |

| Second payment on account | 31 July | Second advance payment |

| Balancing payment | 31 January | Final amount owed for the previous year |

So for the 2025/26 tax year (ending 5 April 2026), your online Self Assessment return and any balancing payment are due by 31 January 2027. That may sound like plenty of time, but many business owners leave it until the final weeks, which creates unnecessary pressure.

Here is a numbered list of the key actions every sole trader or small business owner should take each tax year:

- Keep records from 6 April so nothing slips through the cracks at the start of the new tax year

- Register for Self Assessment by 5 October if it is your first year trading with profits above £1,000

- Review your income and expenses quarterly to avoid a scramble come January

- Submit your return by 31 January (or 31 October if filing on paper)

- Pay any balancing payment by 31 January along with your first payment on account for the following year

- Make your second payment on account by 31 July

The key deadlines in a tax year follow a predictable rhythm once you understand the pattern, with the heaviest obligations falling in January and July. Knowing these dates in advance lets you set aside the right amount of money so you are not caught short.

For a broader picture of your obligations throughout the year, our guide to tax deadlines for UK businesses offers a fuller breakdown, and our overview of essential HMRC deadlines is especially useful if you are based in the Leeds area.

Pro Tip: Set recurring calendar reminders for 31 January and 31 July right now. Many sole traders forget the July payment on account because it does not come with the same level of attention as the January deadline, but missing it still triggers penalties.

Transitional rules and recent reforms affecting tax years

Once you know the routine, it is easy to assume the tax year rules are set in stone. They are not. Recent changes to how trading profits are assessed have had a significant impact on sole traders and partnerships, and further reforms are coming that will affect how you manage your records.

HMRC introduced a major reform to the basis period rules for self-employed individuals and partnerships. Previously, your tax bill was based on the profits of your accounting period ending in the tax year, which could create timing mismatches. From the 2024/25 tax year onwards, all self-employed individuals are taxed on profits arising in the actual tax year itself, not on an accounting year that merely ends during it.

Here is what the basis period reform means in practice:

- Businesses that started trading on or after 6 April 2024 are automatically taxed on the tax year basis with no transition to manage

- The 2023/24 tax year was the transitional year, meaning businesses with non-5-April year ends had to calculate additional profits and could spread the extra tax liability over five years

- Overlap relief, which had accumulated for many businesses over the years, was only claimable during the 2023/24 transitional return

- If you missed claiming overlap relief during 2023/24, you should speak to an accountant immediately

For transitional tax year rules and cross-border scenarios, the picture can get even more complex, particularly for businesses with international elements.

“Businesses starting after 6 April 2024 are automatically placed on the tax year basis. Those with non-April year ends during the 2023/24 transitional year could spread any extra tax liability over five years.”

Looking ahead, Making Tax Digital for Income Tax Self Assessment (MTD ITSA) is due to begin in April 2026. Under this scheme, MTD ITSA applies to self-employed individuals and landlords with total income above £50,000. From that point, these taxpayers must maintain digital records and submit quarterly updates to HMRC, with a final declaration replacing the annual Self Assessment return.

This is not a distant concern. If your income is approaching that £50,000 threshold, you should be preparing now by adopting compatible bookkeeping software, organising your records by tax year quarters, and speaking to your accountant about making the transition smoothly. Our sole trader tax return guide covers a number of the underlying principles that will carry across into the MTD regime.

Practical tips for planning and aligning with the tax year

With those reforms in mind, let us look at steps you can take right now to make the tax year work in your favour rather than against you.

One of the most effective and underused strategies for sole traders is choosing 31 March as your business year end. HMRC treats 31 March as equivalent to 5 April for tax purposes, making it far simpler to align your bookkeeping with the tax year. HMRC estimates around 280,000 sole traders have been affected by the basis period reforms, and many of those complications could have been avoided by simply choosing a 31 March year end from the start. If your business has a strong seasonal trading pattern that genuinely demands a different year end, that is one thing. But if not, keeping it aligned with the tax year removes an entire layer of complexity from your annual accounts.

Here is a practical checklist of annual tasks to keep you ahead of your obligations:

- Update your bookkeeping records at the start of each tax year (6 April) so your records are clean from day one

- Review your income thresholds to check whether you are approaching the VAT registration threshold (currently £90,000) or the MTD ITSA threshold (£50,000)

- Set aside a regular percentage of your income each month specifically for your tax bill, ideally in a separate savings account

- Review claimable expenses quarterly so you are not missing legitimate deductions such as home office costs, mileage, or professional subscriptions

- Check your payments on account after each January return to see whether your estimated advance payments need adjusting

Keeping on top of these tasks throughout the year means January is not a frantic last-minute exercise. Our guide to accounting tips for sole traders provides further practical advice on staying organised, and if you are still getting to grips with setting money aside throughout the year, our resource on budgeting for tax as a small business is a good starting point.

Pro Tip: If you are not yet using cloud-based accounting software, now is the time to start. Platforms such as Xero or QuickBooks allow you to track income and expenses in real time, generate reports aligned to the tax year, and share data directly with your accountant. Ahead of MTD ITSA in April 2026, this kind of preparation is not optional. It is essential.

Our perspective: the tax year isn’t just compliance, it’s your business’s financial backbone

Most business owners we speak to in and around Leeds see the tax year as something they deal with in January and try to forget about the rest of the time. We understand that instinct. Running a business is genuinely demanding, and tax admin rarely feels like a priority when you are busy serving customers or managing a team.

But here is the perspective we want to offer: the tax year is not just a compliance deadline. It is the most consistent framework you have for evaluating how your business is actually performing. When you know why filing tax returns matters beyond HMRC obligation, you start to use the process differently. The businesses we have worked with that plan proactively around the tax year, reviewing their position in October rather than January, know their numbers far better. They make better decisions about hiring, investment, and pricing because they understand their tax position month by month, not just once a year.

The uncomfortable truth is that avoiding the tax year until it cannot be ignored costs you money. Not just in penalties, but in missed planning opportunities, avoidable tax bills, and the stress of scrambling when deadlines are suddenly close. Treat the tax year as your annual business review cycle, and it becomes genuinely useful.

How we can support your compliance and payroll needs

Understanding the tax year is the first step. Staying on top of it throughout the year is where many business owners struggle.

At Concorde Company Solutions, based in Garforth, Leeds, we help sole traders and small business owners stay compliant and confident throughout the tax year. Whether it is managing your reliable payroll solutions, preparing your Self Assessment return, or getting your bookkeeping set up ahead of MTD ITSA, we provide practical, straightforward support without the jargon. We know the HMRC deadlines inside out, and we make sure our clients never miss them. If you would like to take the stress out of tax year management, get in touch with us today for a conversation about how we can help.

Frequently asked questions

Why does the UK tax year run from 6 April to 5 April?

The UK tax year dates stem from historical calendar changes when Britain moved to the Gregorian calendar in 1752, but these are now standard for all HMRC assessments for individuals and businesses across the country.

Can I choose my own business year end?

Yes, but aligning with the tax year by choosing a 31 March or 5 April year end simplifies reporting considerably, particularly given recent reforms. A 31 March year end removes the need for complex profit apportionment calculations.

What happens if I miss a tax deadline?

Missing a deadline triggers automatic HMRC penalties and interest charges. Tax returns are due by 31 January following the end of the tax year for online filings, so set reminders well in advance.

Does MTD ITSA affect all businesses from 2026?

Not all businesses. From April 2026, only self-employed individuals and landlords with income above £50,000 are required to follow MTD ITSA digital reporting rules initially, with lower thresholds phased in over following years.

Do I still need to file a return if I earn less than £1,000?

If your trading profits are below £1,000, you generally do not need to register for Self Assessment, as the trading allowance covers this amount in full.

No responses yet