TL;DR:

- Double entry bookkeeping ensures every financial transaction is recorded in at least two accounts, keeping records balanced and trustworthy. It provides complete, verifiable data essential for accurate financial statements, error detection, and HMRC compliance. Understanding and properly implementing this system is crucial for small business growth, accuracy, fraud prevention, and informed decision-making.

Most small business owners assume bookkeeping simply means logging what comes in and goes out. That misunderstanding costs real money. Double entry bookkeeping is the accounting system that gives every transaction a complete story, and without it, your financial records are built on guesswork rather than fact. This guide walks you through exactly what double entry means, how it works step by step, why it matters for your business, and how to avoid the common pitfalls that catch so many sole traders and small companies off guard.

Table of Contents

- What is double entry bookkeeping?

- How double entry bookkeeping works in practice

- Benefits of double entry for small business owners

- Common mistakes in double-entry bookkeeping and how to avoid them

- The real-world impact: what most guides miss about double entry bookkeeping

- Get expert help with your bookkeeping setup

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Balance is essential | Double-entry bookkeeping ensures that every transaction has equal debits and credits, preventing errors. |

| Reliability for compliance | The method produces reliable financial statements and helps UK businesses meet regulatory obligations. |

| Practical software support | Modern software automates double entry but still requires correct input and understanding. |

| Mistakes are preventable | Awareness of common errors and best practices reduces risk and improves financial clarity. |

What is double entry bookkeeping?

At its core, double entry bookkeeping is a system where every financial transaction is recorded in at least two places. One account receives a debit, another receives a credit, and these two sides must always balance. Think of it as a financial cause and effect: every business event has an equal and opposite reaction in your accounts.

The principle is remarkably straightforward once you strip away the jargon. When your business buys a new laptop for £800, two things happen simultaneously. Your cash account decreases by £800 (a credit), and your equipment account increases by £800 (a debit). The books stay balanced because the total debits always equal the total credits.

As double-entry bookkeeping is defined, it is “a bookkeeping/accounting method where every transaction is recorded in at least two places as equal debits and credits.” That balance is not a bureaucratic formality. It is what makes your accounts trustworthy.

Why does this matter so much? Here is why double entry is considered the gold standard:

- It creates a complete and verifiable record of every transaction.

- It makes errors immediately visible because an imbalance signals a problem.

- It produces the financial statements that HMRC, investors, and lenders expect to see.

- It separates your business finances clearly, which is essential for accurate tax returns.

- It reflects the actual financial health of your business, not just your bank balance.

If you want to build genuinely reliable finances, reading up on small business bookkeeping best practices will give you a solid grounding alongside these principles.

“A business that uses single-entry bookkeeping is essentially navigating with only half a map. Double entry gives you the full picture.”

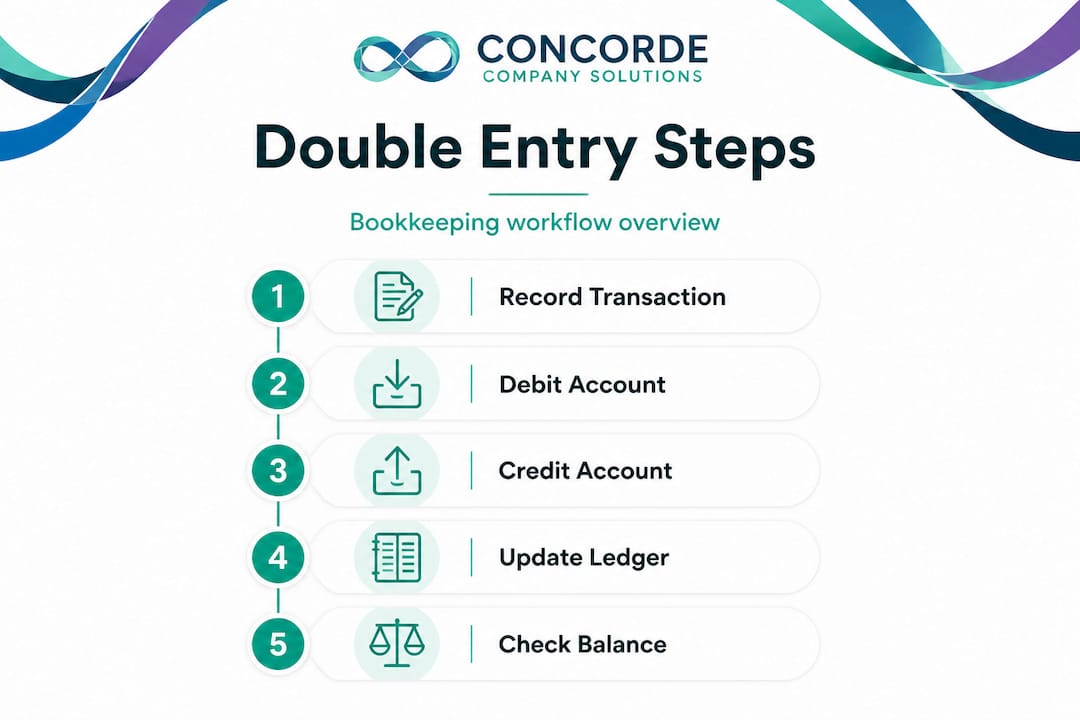

How double entry bookkeeping works in practice

Understanding the idea is one thing. Seeing it in action is another. Here is a step-by-step walkthrough of how the process works for a typical small business transaction.

Imagine you are a sole trader who sells web design services. A client pays you £1,500 for a completed project. Here is exactly what happens in a double entry system:

- Record the journal entry. You open your journal (the first place transactions are written down) and note the date, the two accounts affected, and the amounts. In this case, your bank account is debited £1,500 and your sales revenue account is credited £1,500.

- Post to the general ledger. Each account in the journal entry is then posted to the general ledger, which is the master record of all accounts. The bank account ledger shows a £1,500 increase, and the revenue ledger shows a £1,500 increase on the credit side.

- Run a trial balance. At regular intervals, typically monthly, you total up all debit balances and all credit balances across every account. If the totals match, your records are in balance and you can proceed to produce financial statements.

- Produce financial statements. From the balanced ledger, you generate your profit and loss account, your balance sheet, and cash flow information.

As confirmed by double-entry accounting workflow research, transactions are journalised with date, accounts, and amounts, then posted to the general ledger, and financial statements are produced from those balances. That sequence is not optional. Skipping steps creates gaps that compound into serious problems.

Here is a simple example transaction table to make this concrete:

| Transaction | Account debited | Account credited | Amount |

|---|---|---|---|

| Client pays invoice | Bank account | Sales revenue | £1,500 |

| Purchase office supplies | Office expenses | Bank account | £120 |

| Pay monthly rent | Rent expense | Bank account | £650 |

| Buy equipment on credit | Equipment | Accounts payable | £2,200 |

Notice that in every row, one account goes up and another goes down, but both sides are recorded. That is the core discipline.

Pro Tip: When you are starting out, label each account clearly in your chart of accounts. Using vague names like “miscellaneous” makes it nearly impossible to code transactions correctly, which undermines the whole system.

The step-by-step bookkeeping process is worth bookmarking if you are setting up your system for the first time, as it walks through these stages in detail. You can also revisit the bookkeeping basics guide for a broader foundation.

Benefits of double entry for small business owners

Once your double entry system is running correctly, the practical advantages become impossible to ignore. This is not just about satisfying an accountant. It directly affects how confidently you can run and grow your business.

Accuracy you can trust. When every transaction has two matching entries, mistakes stand out automatically. If you accidentally post £500 to the wrong account, your trial balance will not balance. That imbalance is a built-in alarm bell. Single-entry systems offer no such check.

Fraud prevention. Because every transaction must have an equal and opposite entry, it is significantly harder for money to disappear without a trace. Any irregularity leaves a visible mark in the accounts, which is why double entry is a basic requirement in any business with employees handling finances.

Better business decisions. When your accounts are complete and accurate, you can read your profit and loss account with confidence. You know whether a particular service is profitable, whether your overheads are creeping up, and whether your cash flow is sustainable. Incomplete records produce false reassurance.

HMRC compliance. Your tax return is only as accurate as your records. Double entry produces the structured data that makes your accounts straightforward to file. It also means you are far better prepared if HMRC ever asks questions.

The double-entry accounting system supports your general ledger and produces reports such as the trial balance, income statement, and balance sheet. These are not optional extras. They are the documents that define your business’s financial position.

Here is a quick comparison to show why double entry outperforms single-entry bookkeeping:

| Feature | Single-entry | Double-entry |

|---|---|---|

| Transaction recording | One side only | Both sides recorded |

| Error detection | Minimal | Built-in via trial balance |

| Financial statements | Limited | Full set available |

| Fraud deterrence | Low | High |

| HMRC suitability | Basic only | Full compliance |

| Business decision support | Partial | Comprehensive |

Key practical benefits worth highlighting:

- Your balance sheet is always available and reliable.

- You can separate personal and business finances cleanly.

- Investors and lenders expect double-entry records.

- Year-end accounts are faster and less stressful to prepare.

Pro Tip: Review your trial balance at least once a month. If you wait until year-end to check whether everything balances, errors will have compounded and become far harder to trace.

For a deeper look at why accurate records matter day to day, the articles on bookkeeping importance for UK business and accurate bookkeeping for UK SMEs offer practical context.

Common mistakes in double-entry bookkeeping and how to avoid them

Even business owners who understand the principles make recurring errors. Knowing where the traps are makes them much easier to avoid.

Unbalanced entries. This is the most obvious mistake: debiting one account without correctly crediting another, or entering the wrong amounts on one side. The result is a trial balance that simply will not add up, and hunting down the discrepancy wastes time that should be spent running the business.

Wrong account coding. Posting a transaction to the wrong account type is a subtle but damaging error. If you accidentally code a capital equipment purchase as an office expense, your profit figure is wrong and your balance sheet is incomplete. This is especially common when setting up a new chart of accounts.

Skipping the reconciliation step. Many business owners enter transactions regularly but never reconcile their ledger to their bank statements. Reconciliation is the process of confirming that your records match reality. Without it, duplicate entries or missed transactions go unnoticed for months.

Mixing personal and business transactions. For sole traders in particular, this is a persistent problem. A single personal transaction mixed into business accounts can distort every report you produce and create headaches at tax time.

Relying on software without understanding the rules. Accounting software automates a great deal, but it cannot think for you. As correctly coding transactions is fundamental, modern software records the double-entry logic automatically, but you must still code transactions correctly for reliable results. Enter the wrong account code and the software will faithfully record an error for you.

How to protect yourself:

- Set up your chart of accounts carefully at the start, with clear and specific account names.

- Reconcile your bank account every month without exception.

- Keep personal and business finances completely separate, ideally with a dedicated business bank account.

- Learn the basic debit and credit rules for each account type, even if software handles the mechanics.

- Run a trial balance monthly and investigate any imbalance immediately.

Pro Tip: If your software flags an unusual transaction or your trial balance is off by an odd amount like £0.01, do not ignore it. Small discrepancies often point to a systemic coding error that grows over time.

Reading the guide on common accounting mistakes is strongly recommended if you are reviewing your current bookkeeping setup, as it covers errors that affect businesses at every stage.

The real-world impact: what most guides miss about double entry bookkeeping

Here is something most bookkeeping articles will not tell you. The rise of cloud accounting software has created a dangerous illusion: the idea that technology has made understanding double entry optional. It has not. If anything, it has made that understanding more important.

Software like Xero or QuickBooks does automate the debit and credit mechanics. Every time you log an invoice or record a payment, the system handles the double entry behind the scenes. That is genuinely useful and saves significant time. But the software has no idea whether you have chosen the right account, whether a purchase should be capitalised or expensed, or whether that bank transfer was a loan repayment or a salary payment. Those judgements are yours.

We see this regularly in practice. A business owner imports a year’s worth of transactions, confident the software has handled everything. Then at year-end, the accounts tell a story that does not match reality because dozens of transactions were coded to the wrong accounts throughout the year. Correcting it retrospectively is far more time-consuming than getting it right in the first place.

The businesses that get the most from their accounting software are those who actually understand why debits and credits work the way they do. They know that assets and expenses increase with debits, while liabilities, equity, and income increase with credits. They understand what their chart of accounts represents. When something looks odd in a report, they can investigate rather than simply accepting a figure that seems wrong.

Double entry bookkeeping is not an accounting ritual from the fifteenth century that modern technology has superseded. It is a logical framework that sits beneath every reliable set of business accounts, whether those accounts are written in a ledger book or generated by software. Following a solid bookkeeping process guide alongside using software is how you build records you can genuinely rely on.

The investment in understanding is small. The payoff in financial clarity, reduced errors, and confidence at tax time is substantial.

Get expert help with your bookkeeping setup

Setting up double entry bookkeeping correctly from the start saves enormous time and frustration down the line. Whether you are a sole trader getting to grips with your first accounting system or a growing small business that needs a more structured approach, professional guidance makes a real difference.

At Concorde Company Solutions, we work with small businesses and sole traders across Leeds and beyond to set up bookkeeping systems that are accurate, compliant, and straightforward to maintain. From choosing the right software to establishing a chart of accounts that works for your specific business, our team provides hands-on, practical support. If your current records feel uncertain or you want to start a new business on solid financial footing, visit our UK bookkeeping help page to find out how we can help you build confidence in your numbers from day one.

Frequently asked questions

How does double-entry bookkeeping differ from single-entry?

Double-entry bookkeeping records every transaction twice as both a debit and a credit, unlike single-entry which records only one side, making double entry far more reliable for detecting errors and producing complete financial statements.

What is a trial balance and why is it important?

A trial balance totals all debit and credit balances across your accounts to confirm they match, providing an early warning of errors before financial statements are produced such as your income statement and balance sheet.

Can I use software to manage double-entry bookkeeping?

Yes, most accounting software automates the double-entry logic, but as correctly coding transactions is essential, you must still assign each transaction to the right account or the automation simply records your mistakes more efficiently.

What types of accounts are involved in double-entry bookkeeping?

Double-entry bookkeeping uses five main account types: assets, liabilities, equity, revenue, and expenses, and every transaction is recorded across at least two of these to ensure the accounts remain balanced and complete.

No responses yet