TL;DR:

- Most UK businesses overlook indirect taxes, which are a significant and embedded financial burden. Proper management of VAT, excise, and customs duties is crucial to ensure compliance, optimize cash flow, and avoid penalties. Strategic handling, digital record-keeping, and regular reviews enable businesses to reduce risks and maximize recoverable VAT opportunities.

Most UK business owners spend considerable energy worrying about corporation tax or income tax, yet indirect taxes quietly represent one of the largest financial obligations your business manages each year. Unlike a bill that lands in your name, indirect taxes are woven into prices, transactions, and supply chains, which means errors are easy to make and costly to discover. HMRC collects billions annually through these mechanisms, and the compliance burden falls squarely on you as the business operator. This guide cuts through the confusion to give you a practical understanding of indirect taxes, who is responsible, and how to stay on the right side of the rules.

Table of Contents

- What are indirect taxes?

- Main types of indirect taxes faced by UK businesses

- How indirect taxes are collected and reported

- Nuances, challenges, and compliance risks

- A smarter approach to indirect tax compliance

- How Concorde Company Solutions can support your compliance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Indirect tax definition | Indirect taxes are collected by businesses from customers on goods and services and paid to government. |

| Types UK businesses face | VAT, excise duties, and customs duties are the main forms of indirect taxes affecting UK companies. |

| Compliance obligations | Firms must keep digital records, file accurate returns, and follow HMRC guidelines to avoid penalties. |

| Risks and complexity | Nuances like partial exemption and VAT grouping create compliance challenges with real cash exposure. |

| Smart compliance | Tech-enabled controls and periodic reviews help turn tax compliance into a business advantage. |

What are indirect taxes?

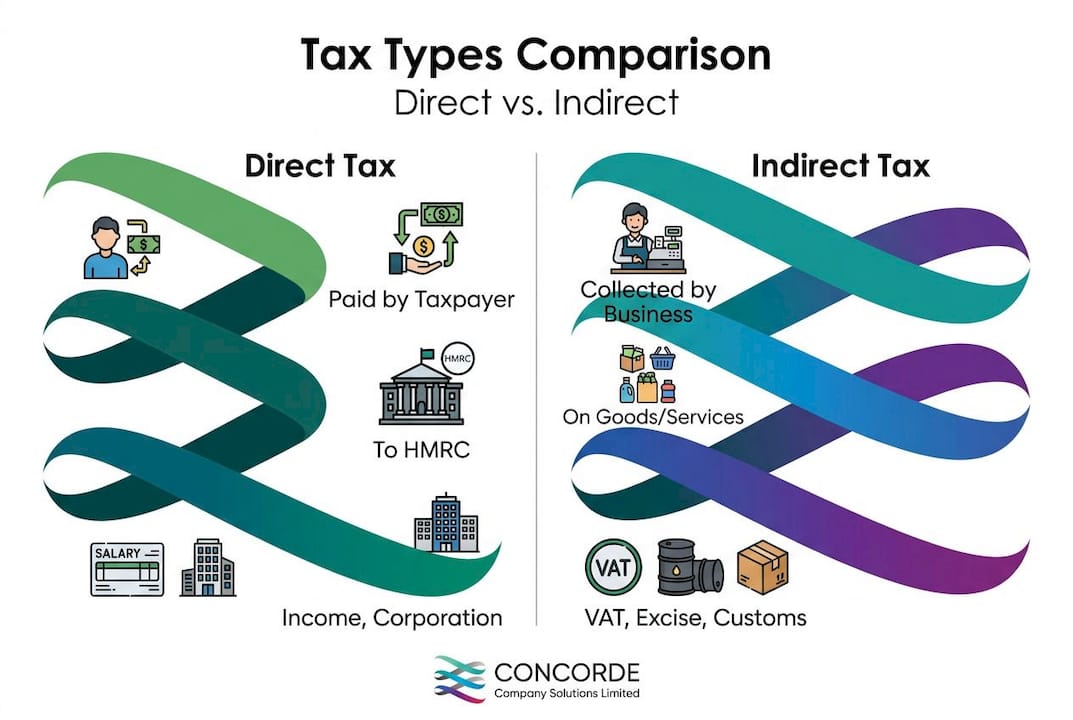

To understand indirect taxes, you first need to see how they differ from the taxes most people immediately think of. Direct taxes, such as income tax and corporation tax, are charged on your income or profits and paid directly to HMRC by the taxpayer. Indirect taxes work very differently.

Indirect taxes in the UK are taxes on goods and services that businesses collect from customers and remit to HMRC, rather than taxes paid directly by the taxpayer on income or profits. In practice, your business acts as an unpaid tax collector. The customer pays the tax embedded in the price, and you forward that money to HMRC at regular intervals. The financial burden rests with the consumer, but the legal and administrative responsibility rests with you.

Here is a simple side-by-side comparison to make the distinction clear:

| Feature | Direct tax | Indirect tax |

|---|---|---|

| Who pays HMRC | Taxpayer directly | Business on behalf of customer |

| What is taxed | Income or profits | Goods and services |

| Visibility to consumer | Usually visible (e.g. self-assessment) | Often hidden in the purchase price |

| Rate structure | Often progressive (higher earners pay more) | Usually flat rate, regardless of income |

| Examples | Income tax, corporation tax | VAT, excise duty, customs duty |

One important economic feature of indirect taxes is their regressive character. As noted by tax economists, indirect taxes apply at the same rate regardless of income, which means they take a proportionally larger slice of a lower-income household’s budget. This matters for your pricing decisions and for understanding why certain reliefs and zero-rates exist for essentials like food and children’s clothing.

Key reasons why indirect taxes matter to your business include:

- They affect your cashflow because you collect money on behalf of HMRC before remitting it, creating a timing obligation.

- Mistakes in applying the right rate or reclaiming input tax trigger HMRC compliance checks and financial penalties.

- The rules interact with your pricing, contract terms, and supplier relationships in ways that go beyond simple bookkeeping.

- International businesses face additional layers of complexity when selling into or out of the UK.

Understanding the full range of business tax obligations is the starting point for building a reliable compliance framework.

Main types of indirect taxes faced by UK businesses

With the basic concept established, let’s take a closer look at the main forms of indirect tax relevant to businesses operating in the UK.

VAT

Value Added Tax is the dominant indirect tax for most UK businesses. The standard rate is 20%, with a reduced rate of 5% on items like domestic energy and children’s car seats, and a zero rate on most food and children’s clothing. VAT is charged on taxable supplies of goods and services and collected at each stage of the supply chain, with businesses reclaiming the VAT they have paid on their own purchases (input tax) and remitting the difference on their sales (output tax).

Once your taxable turnover exceeds £90,000 in a rolling 12-month period, VAT registration becomes mandatory. You can also register voluntarily below that threshold, which can be beneficial if your customers are VAT-registered businesses who can reclaim it, or if you want to reclaim input VAT on your own purchases.

Excise duties

Excise duties apply to specific categories of goods and are charged on production, sale, or sometimes import within the UK. The main product categories affected include:

- Alcohol: Beer, wine, spirits, and cider each have separate duty rates based on alcohol content.

- Tobacco: Cigarettes, hand-rolling tobacco, and cigars are all subject to duty, with rates set per unit or per weight.

- Fuel: Hydrocarbon oils such as petrol and diesel carry significant duty charges that feed into the prices businesses pay for vehicles and logistics.

- Gambling and gaming: Certain types of betting and gaming activity carry specific duty obligations.

If your business manufactures, warehouses, or distributes any of these products, excise duty is a major compliance consideration and requires specific registrations and record-keeping.

Customs duties

Post-Brexit, customs duties have become a far more significant issue for UK businesses. Importing goods from outside the UK, including from the EU, now triggers customs procedures that did not apply before January 2021. Importers need an Economic Operators Registration and Identification (EORI) number, must submit customs declarations, and pay duty based on the commodity code and country of origin.

Pro Tip: Even if your supplier overseas handles shipping, the legal obligation to pay customs duty and submit declarations generally falls on the UK importer of record, meaning your business. Always check who bears this responsibility in your supplier contracts.

The rates you pay depend on the commodity and trade agreements in place. Carbon Border Adjustment Mechanism (CBAM) charges are also emerging for energy-intensive goods, adding another layer of cost planning for manufacturers and importers.

| Indirect tax | What triggers it | Who is responsible | Key rate |

|---|---|---|---|

| VAT | Taxable supply of goods or services | VAT-registered business | 20% (standard) |

| Excise duty | Production or release for consumption | Manufacturer or warehouse keeper | Varies by product |

| Customs duty | Import of goods from outside UK | Importer of record | Varies by commodity code |

How indirect taxes are collected and reported

Once you know which taxes apply, it’s crucial to understand your collection and reporting responsibilities as a UK business.

The process for VAT, which applies to the majority of businesses, follows a clear cycle:

- Charge output tax on your taxable sales and include it on your invoices at the correct rate.

- Record input tax on every qualifying purchase, retaining valid VAT invoices or receipts as evidence.

- Reconcile at the end of your VAT period (usually quarterly) by calculating the difference between output and input tax.

- Submit your VAT return through HMRC-approved software and pay any tax due, or claim a repayment if input tax exceeds output tax.

- Maintain digital records to satisfy Making Tax Digital requirements.

Making Tax Digital for VAT (MTD) is no longer optional. HMRC now requires digital VAT records and quarterly returns submitted via compatible software, with their GfC8 guidance setting out detailed expectations for VAT accounting controls. This is not just about submitting numbers digitally; it is about maintaining an auditable trail from source transactions through to the final return.

“Good compliance controls are not just about getting the VAT return right. They are about building processes that your whole business can rely on, month after month.” This is precisely the mindset HMRC wants to see when reviewing your records.

Practical steps to strengthen your compliance process include:

- Using accounting software that is MTD-compatible and connected directly to your invoicing system.

- Setting up automated bank feeds to reduce manual data entry errors.

- Completing regular reconciliations between your VAT account and your bank, rather than leaving it all to quarter-end.

- Reviewing your digital tax submission process to ensure it meets current HMRC standards.

Common mistakes that lead to penalties include: applying the wrong VAT rate (especially on borderline items such as food, clothing, or construction services), failing to account for VAT on imported goods, missing the registration threshold, and not retaining valid input tax evidence. Explore more detail on the tax obligations entrepreneurs face at each growth stage.

Pro Tip: Set a diary reminder one month before the end of each VAT period to review your figures. Catching errors early is far cheaper than correcting them after a return has been filed or, worse, after an HMRC inquiry has begun.

Nuances, challenges, and compliance risks

With the foundational process clear, let’s examine the real-world complexities and risks businesses face with indirect taxes.

Partial exemption

Not all businesses make exclusively taxable supplies. If you make both taxable and exempt supplies (for example, a property company that sells commercial and residential units, or a financial services firm with some consulting income), you fall into the partial exemption rules. This means you cannot reclaim all of your input VAT; instead, you must apportion it according to an approved method.

The de minimis threshold is £7,500 of exempt input tax per year. Below this figure, you may be able to recover all your input tax. Above it, the apportionment rules bite, and annual adjustments become mandatory.

VAT grouping and care sector complications

VAT grouping, where related companies register as a single entity for VAT purposes, can be a useful tool for cash management. However, HMRC has recently issued guidance on misuse of VAT grouping in the care industry, where some businesses attempted to use inter-group supplies to avoid charging VAT on exempt services. HMRC is actively scrutinising such arrangements, and the same vigilance applies to any sector where grouping could be seen as avoidance rather than genuine simplification.

The VAT gap and what it means for you

The VAT gap for 2023 to 2024 is estimated at approximately 5 to 6% of the theoretical liability, representing billions in uncollected tax. HMRC uses this data to target compliance activity, meaning sectors and business types with higher gap estimates attract more scrutiny.

A high VAT gap in your sector is not just a national statistic; it is a signal that HMRC is likely already looking at businesses like yours.

Key risks to watch for in your own compliance include:

- Value shifting in bundles: Pricing a package of taxable and exempt items in a way that minimises VAT output can attract scrutiny.

- Reverse charge errors: Getting financial compliance wrong on domestic reverse charge transactions (construction, telecoms) is a common and expensive mistake.

- Import VAT recovery: Many businesses miss legitimate claims for import VAT paid on goods, or fail to account for deferred import VAT correctly.

- Periodic reviews: Treat your VAT and indirect tax position as something requiring a regular health check, not just an annual afterthought.

A smarter approach to indirect tax compliance

Most businesses treat indirect tax as a compliance obligation to discharge as quickly and quietly as possible. File the return, pay the bill, move on. We think that attitude is a genuine missed opportunity.

The businesses that manage indirect taxes strategically consistently discover recoverable VAT they had written off, identify pricing errors that were costing them margin, and reduce the risk of disruptive HMRC inquiries. That is not luck; it is the result of investing in proper controls and treating the tax function as part of the broader commercial operation, not a back-office afterthought.

Post-Brexit and growing digitalisation are raising the stakes further. Customs duty classifications that were never relevant before 2021 now affect landed costs and pricing competitiveness for thousands of UK importers. HMRC’s digital agenda, including the expansion of MTD and preventing tax losses through better data, means that the quality of your records is increasingly visible to the tax authority without them needing to visit your office.

The practical actions that separate proactive businesses from reactive ones are straightforward: conduct an indirect tax review at least once a year, invest in software that automates your record-keeping, and build scenario planning into your financial decisions whenever you launch new products, enter new markets, or restructure your business. The compliance cost of getting this wrong far outweighs the investment in getting it right. Businesses that act now will have well-tested systems when HMRC’s scrutiny inevitably tightens further.

How Concorde Company Solutions can support your compliance

Mastering indirect taxes is not just about avoiding penalties; it actively strengthens your cashflow, protects your margins, and gives you real confidence in your financial reporting.

At Concorde Company Solutions, we work with business owners and finance managers across the UK to build compliance frameworks that actually work in practice, not just on paper. Whether you need support with VAT registration, MTD compliance, payroll obligations, or a complete review of your financial controls, our team brings hands-on expertise to every engagement. Explore our payroll solutions or browse our full range of compliance services to find the right support for your business. We are based in Garforth, Leeds, and we work with businesses of all sizes who want a reliable, knowledgeable partner rather than a transactional accountant.

Frequently asked questions

What are the main forms of indirect tax in the UK?

The main types are VAT at a 20% standard rate, excise duties on goods like alcohol, tobacco, and fuel, and customs duties on imports from outside the UK.

How is VAT different from income tax?

VAT is an indirect tax on goods and services collected by businesses from customers and remitted to HMRC, whereas income tax is paid directly on earnings or profits and falls on the taxpayer personally.

What triggers excise and customs duties?

Excise duties arise on UK production or release of specific goods for consumption; customs duties are triggered by importing goods across the UK border, with importers requiring an EORI number and appropriate declarations.

What is the VAT gap and why does it matter?

The VAT gap is estimated at approximately 5 to 6% of theoretical liability, representing unpaid VAT through error or evasion, and it directs HMRC’s compliance activity towards sectors where shortfalls are greatest.

Are there special VAT rules for mixed or exempt businesses?

Yes. Businesses making both taxable and exempt supplies must apportion input VAT using an approved partial exemption method and carry out annual adjustments, with a de minimis threshold of £7,500 per year.

No responses yet