TL;DR:

- Most UK SME failures are caused by cash flow problems, not lack of profit.

- Cash flow forecasting predicts actual money movements to prevent shortfalls and plan payments.

- Regular updates and realistic assumptions are essential to effective cash flow management.

Most UK businesses that fail do not fail because they are unprofitable. They fail because they run out of cash at the wrong moment. In fact, over 50% of UK SME failures are linked to cash flow problems rather than a lack of profit. That distinction matters enormously. You can be winning clients, growing your revenue, and still find yourself unable to pay wages or suppliers. This guide will explain exactly what cash flow forecasting is, why it is so powerful for small and medium-sized businesses, and how you can start using it to make smarter, more confident decisions about your financial future.

Table of Contents

- Understanding cash flow forecasting

- How to create a cash flow forecast

- Key challenges and UK-specific nuances

- Common mistakes and how to avoid them

- Why most businesses underestimate cash flow forecasting

- Take the next step to strengthen your business cash flow

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cash flow vs profit | Profit may look healthy but cash flow determines whether your business can pay its bills on time. |

| Forecast regularly | Review and update your cash flow forecast weekly or monthly to stay ahead of surprises. |

| Account for UK specifics | Factor in payment delays, VAT, tax timings, and seasonal trends unique to UK businesses. |

| Avoid common mistakes | Don’t confuse profit with cash or assume payments always arrive on schedule—plan for delays and variations. |

| Strengthen with support | Using expert help enables more robust cash flow management and frees you to focus on business growth. |

Understanding cash flow forecasting

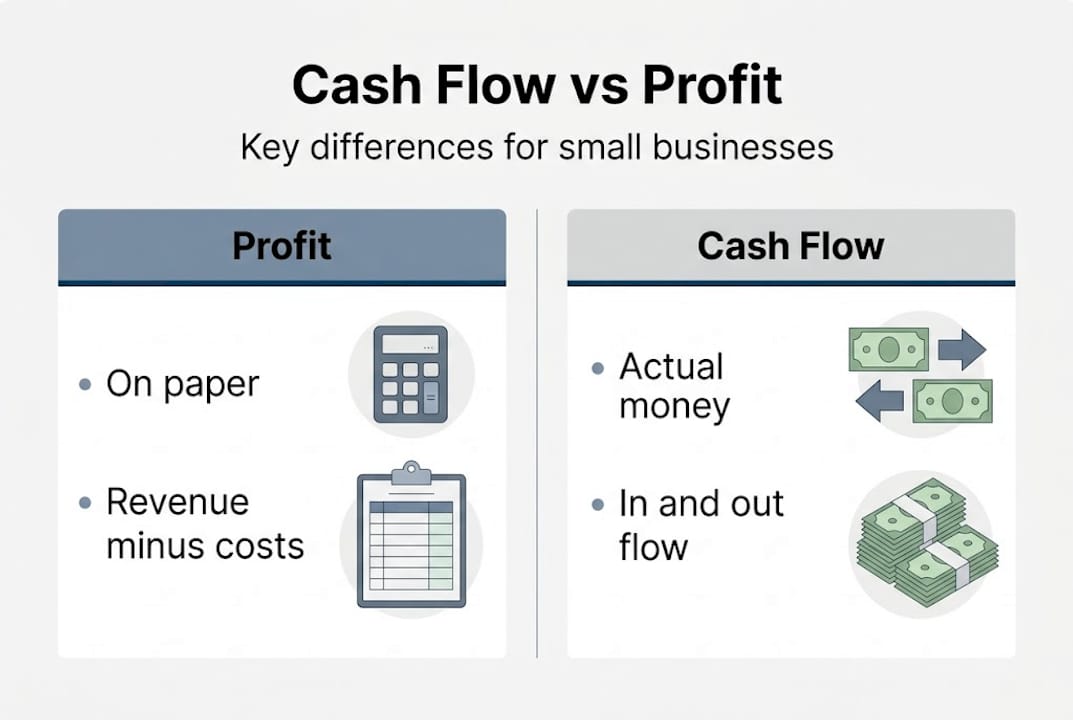

Cash flow forecasting is one of those terms that sounds technical but is, at its core, a very practical tool. Put simply, cash flow forecasting estimates the timing and amount of money coming into and going out of your business, so you can predict your future cash position at any given moment. It is not the same as profit.

Profit is calculated by subtracting your costs from your revenue on paper. Cash flow, however, shows you what money is actually sitting in your account and available to use. You can record a profitable invoice in January and not receive payment until March. In that gap, your rent, wages, and supplier bills still need to be paid. That is where businesses get into serious trouble.

Understanding cash basis accounting helps clarify this distinction further, particularly for sole traders and smaller businesses that record income and expenditure only when cash actually changes hands.

Here is why cash flow forecasting matters for UK SMEs:

- It warns you weeks or months in advance when a shortfall is likely

- It helps you time major purchases or investments more wisely

- It gives lenders and investors confidence in your financial management

- It reduces the need for emergency borrowing, which is often expensive

- It supports better negotiation with suppliers on payment terms

Common cash flow pitfalls include relying on a single large client, underestimating how long customers take to pay, and failing to set aside funds for quarterly VAT or annual corporation tax. Many business owners track turnover closely but pay little attention to the timing of actual cash movements. That gap in awareness is precisely what a good forecast closes.

“A cash flow forecast is not just a financial document. It is your early warning system, giving you time to act before a problem becomes a crisis.”

| Feature | Profit and loss | Cash flow forecast |

|---|---|---|

| What it shows | Revenue minus costs | Actual money in and out |

| Timing of entries | When invoices are raised | When payments are received or made |

| Use | Measures business performance | Predicts financial position |

| Frequency | Monthly or annually | Weekly or monthly |

| Key benefit | Shows profitability | Prevents cash shortfalls |

How to create a cash flow forecast

With a clearer understanding of what cash flow forecasting is, you are ready to assemble your own forecast. The process is more straightforward than many business owners expect, and you do not need specialist software to get started.

A simple forecasting method starts with your opening bank balance, lists all expected inflows and outflows for each period, calculates your net cash position, and finishes with a closing balance that becomes the opening balance for the next period. Repeat this weekly or monthly and you have a rolling forecast.

Here is a step-by-step approach:

- Set your time horizon. Most UK SMEs benefit from a 13-week (three-month) rolling forecast as a minimum. Longer horizons are useful for planning but are naturally less precise.

- List all cash inflows. Include customer payments, grants, loan receipts, and any other income. Use realistic dates based on your actual payment terms, not invoice dates.

- List all cash outflows. Include wages, rent, supplier payments, loan repayments, VAT, PAYE, and corporation tax. Do not forget irregular costs like insurance renewals or equipment servicing.

- Calculate net cash flow. Subtract total outflows from total inflows for each period.

- Project your closing balance. Add net cash flow to your opening balance. If this figure goes negative, you have identified a future shortfall in time to act.

| Month | Opening balance | Inflows | Outflows | Net cash flow | Closing balance |

|---|---|---|---|---|---|

| January | £8,000 | £12,000 | £10,500 | £1,500 | £9,500 |

| February | £9,500 | £9,000 | £11,200 | -£2,200 | £7,300 |

| March | £7,300 | £14,000 | £10,000 | £4,000 | £11,300 |

In the example above, February shows a negative net cash flow. Without a forecast, that shortfall would come as a shock. With it, you have a full month to arrange a short-term credit facility or chase outstanding invoices.

For more structured planning, explore forecasting methods for SMEs and read up on cash flow management steps that tie forecasting into your broader financial strategy.

Pro Tip: Set a recurring monthly calendar reminder to update your forecast. Even a 30-minute review can reveal a looming problem before it becomes urgent.

Key challenges and UK-specific nuances

Once you have built your forecast, it is crucial to understand the issues that make UK business forecasting particularly challenging. A forecast is only as reliable as the assumptions behind it, and several factors unique to the UK business environment can quickly throw those assumptions off course.

UK payment delays from corporate clients, SME suppliers, and even government bodies are a persistent problem. Standard 30-day payment terms often stretch to 60 or 90 days in practice, and public sector contracts are notorious for slow processing. Building realistic payment lag into your inflow assumptions is not pessimism. It is accuracy.

Tax timing adds another layer of complexity. Consider the key obligations that affect cash at specific points in the year:

- VAT: Paid quarterly (or monthly for some businesses), creating predictable but significant cash demands

- PAYE and National Insurance: Due monthly, requiring a consistent cash reserve for payroll

- Corporation tax: Typically due nine months and one day after your accounting year-end

- Self Assessment: Payments on account in January and July can surprise newer business owners

Planning ahead for these obligations is essential. Reading up on planning for tax payments and knowing your critical UK tax deadlines will help you build these into your forecast accurately.

Seasonality is another variable many SMEs underestimate. A retailer may need to stockpile inventory in September for the Christmas peak, creating significant outflows months before the revenue arrives. A construction firm dealing with retention clauses may not receive a portion of project payments until months after work is complete. Both scenarios demand that your forecast reflects the actual cash timing rather than the commercial reality you might prefer.

Key statistic: Over 50% of UK SME failures are caused by poor cash flow management, with late payments, tax timing, and rapid growth all cited as major contributors.

Rapid growth is itself a cash flow risk. Winning a large contract often means hiring staff, buying materials, and ramping up operations before the client pays a single penny. Without a robust forecast, growth can paradoxically accelerate a business towards insolvency.

Pro Tip: Build a separate tab in your forecast specifically for tax liabilities. Map out every payment date for the year ahead so you always know what is coming.

Common mistakes and how to avoid them

Mastering the process is only half the battle. Many UK businesses are caught out by avoidable missteps that undermine even the most carefully constructed forecast. Recognising these errors is the first step to avoiding them.

The most common cash flow forecasting mistakes include confusing profit with cash, assuming customers pay immediately, ignoring seasonal and tax-driven peaks, treating the forecast as a one-off document, and applying excessive optimism to income projections. Each of these is remarkably common and each can be corrected with discipline.

- Confusing profit with cash. Just because you have invoiced a client does not mean the money is available. Always build your forecast around expected payment dates, not invoice dates. The difference between profit and cash is one of the most important distinctions in financial management.

- Assuming customers pay on time. Use your actual payment history to set inflow timings. If a client routinely pays 45 days after invoice, model that reality rather than the 30-day term on your contract.

- Ignoring tax and seasonal peaks. Failing to account for a large VAT bill or a quiet January can create an avoidable crisis. These events are predictable. Plan for them.

- Treating the forecast as static. A forecast you built in January and never revisited is almost useless by April. The value lies in regular updates, not the original document.

- Being overly optimistic. It is natural to want to forecast best-case scenarios, but your cash management decisions must be based on realistic or conservative assumptions. Consider modelling a worst-case scenario alongside your base case.

“The businesses that weather difficult periods are not always the most profitable. They are the ones that knew a difficult period was coming and prepared for it.”

Avoidable mistakes have a compounding effect. One missed shortfall leads to emergency borrowing, which increases outflows, which creates the next shortfall. Staying vigilant and honest with your numbers breaks that cycle.

Why most businesses underestimate cash flow forecasting

Here is something we observe regularly when working with UK SMEs: most business owners believe they have a handle on their finances because they check their bank balance each morning. That is not cash flow management. That is financial rear-view-mirror driving.

The common behaviour is to run a rough forecast when things get tight or when a bank asks for one. True financial resilience requires something different entirely. It requires a rolling 13-week forecast, updated weekly or monthly, with at least two scenarios modelled: a base case and a stress case. The business forecasting guide we have put together goes deeper into these scenario-planning methods.

The uncomfortable truth is that cash ‘profit’ is not cash reality. A business can look healthy on a profit and loss statement for months before a cash crisis becomes visible. The discipline of regular forecasting forces you to confront that gap before it becomes dangerous. Commit to weekly or monthly reviews, not one-off exercises, and treat your forecast as a living document rather than a compliance checkbox.

Take the next step to strengthen your business cash flow

Understanding cash flow forecasting is genuinely transformative for a business owner, but translating that knowledge into action takes time and focus that many busy SME owners simply do not have.

At Concorde Company Solutions, we help small and medium-sized businesses across the UK take control of their financial position with practical, expert support. From payroll solutions that keep your outflows predictable and compliant, to bookkeeping and financial planning that feeds directly into your cash flow picture, we are here to make things simpler. If you would like to speak to someone who understands the pressures UK SMEs face, get in touch with us today and let us help you plan with confidence.

Frequently asked questions

What is the main purpose of cash flow forecasting?

Cash flow forecasting helps you predict when money will enter and leave your business, so you can spot cash gaps before they become a crisis and make more confident financial decisions.

How often should UK SMEs update a cash flow forecast?

Review your forecast at least monthly. For growing or volatile businesses, weekly rolling updates offer the best protection against unexpected shortfalls.

What is the difference between profit and cash flow?

Profit is what your business earns on paper after costs, while cash flow reflects actual money movements in and out of your account, factoring in when payments are actually made and received.

Which UK taxes most often disrupt cash flow?

VAT, corporation tax, and PAYE and National Insurance are the most disruptive due to their specific payment schedules and the size of the sums involved.

What is one common mistake SMEs make with cash flow forecasting?

Many SMEs assume customers pay immediately upon invoicing, ignoring normal payment delays that can leave the business without the cash it expected to have available.

No responses yet