Many small and medium-sized business owners assume audits are only for large corporations with complex financial structures. This misconception leaves UK SMEs unprepared when they encounter audit requirements or miss opportunities to strengthen their financial transparency. Audits serve as powerful tools for compliance, fraud detection, and operational improvement regardless of company size. Whether you’re approaching statutory thresholds or seeking investor confidence, understanding audits helps you navigate regulatory requirements whilst building stakeholder trust. This guide explains what audits involve, why they matter for your business, and how proper preparation transforms audits from daunting obligations into valuable opportunities for financial clarity and strategic insight.

Table of Contents

- Key takeaways

- What is a business audit and why does it matter?

- The audit process explained: from preparation to completion

- Types of audits: how to know which one you need

- How to prepare your business for a successful audit

- How Concorde Company Solutions can support your audit needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Audits for SMEs | Audits are not just for large firms, they are essential for UK SMEs to verify accuracy and compliance. |

| Audit types explained | Different audit types cover financial, regulatory, operational and internal reviews to suit diverse business needs. |

| Statutory thresholds | In the UK statutory audits apply when turnover, balance sheet totals or employee numbers exceed specified thresholds. |

| Preparation benefits | Organised record keeping and regular reconciliations streamline audits and improve financial management throughout the year. |

What is a business audit and why does it matter?

A business audit represents an independent examination of your financial records, processes, and controls to verify accuracy and compliance. Qualified auditors review your accounts, transactions, and supporting documentation to provide an objective assessment of your financial position. For UK SMEs, audits verify financial statement accuracy whilst ensuring you meet regulatory requirements set by Companies House and HMRC.

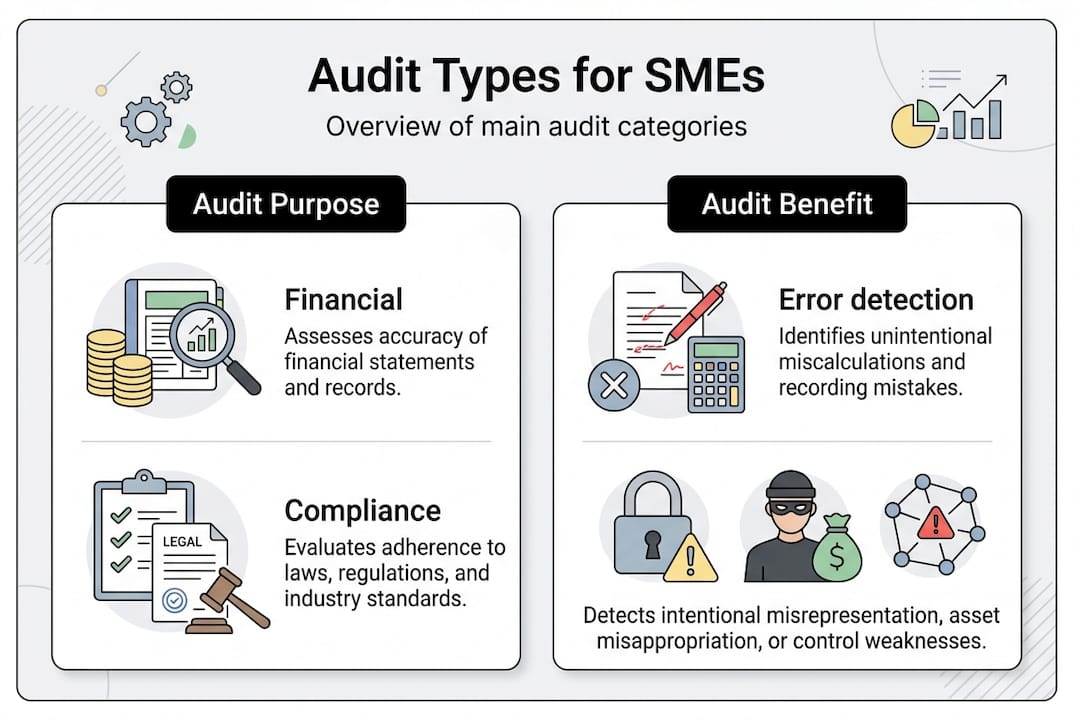

Several audit types serve different purposes. Financial audits examine your annual accounts and financial statements for accuracy and compliance with accounting standards. Compliance audits assess whether you’re meeting specific regulatory requirements, from tax obligations to industry regulations. Operational audits evaluate internal processes and efficiency, identifying areas for improvement. Internal audits, conducted by your own team or hired specialists, review controls and risk management before external scrutiny.

UK law requires audits for companies exceeding certain thresholds. Currently, companies with annual turnover above £10.2 million, balance sheet totals over £5.1 million, or more than 50 employees must undergo statutory audits. Smaller businesses often qualify for audit exemptions, though some choose voluntary audits to satisfy investors or lenders. Understanding these thresholds helps you plan for compliance costs and timing.

Beyond legal compliance, audits deliver substantial benefits. They detect errors, inconsistencies, and potential fraud before problems escalate. Audited accounts carry greater credibility with banks, investors, and suppliers, often improving your access to financing and trade credit. The process frequently uncovers operational inefficiencies, suggesting improvements to cash flow management, inventory control, or expense tracking. Many businesses find the discipline of audit preparation strengthens their financial management throughout the year.

Pro Tip: Maintain organised, detailed financial records consistently rather than scrambling before audit season. Digital accounting systems with regular reconciliations make audit preparation significantly smoother and often reveal issues whilst they’re still easy to resolve.

The audit process explained: from preparation to completion

Understanding the audit journey removes much of the anxiety surrounding this process. Audits typically unfold through four distinct stages, each with specific activities and expectations for your involvement.

Planning begins weeks before auditors arrive. They’ll request preliminary information about your business structure, accounting systems, and significant transactions. You’ll discuss timing, scope, and any areas requiring special attention. This stage sets expectations and allows you to gather necessary documentation. Good planning prevents last minute document searches and reduces disruption to daily operations.

Fieldwork represents the hands on examination phase. Auditors visit your premises or review records remotely, testing transactions, verifying balances, and examining supporting evidence. They’ll interview key staff, observe processes, and assess internal controls. Expect questions about unusual transactions, significant estimates, or changes in accounting policies. Your responsiveness during fieldwork directly impacts audit duration and efficiency.

Reporting follows the examination. Auditors compile findings, identify issues, and draft their opinion on your financial statements. They’ll discuss significant matters with management before finalising reports. The audit opinion states whether your accounts present a true and fair view, with qualifications noted for any material misstatements or limitations. This report becomes part of your filed accounts, visible to stakeholders and regulators.

Follow up addresses any recommendations or required corrections. You’ll implement agreed changes, adjust accounts if necessary, and often receive a management letter suggesting operational improvements. Following a clear audit checklist improves efficiency and outcomes, ensuring you’ve addressed all requirements before the next cycle begins.

Five essential preparation steps maximise audit success:

- Organise all financial records, including bank statements, invoices, receipts, and contracts, in logical, easily accessible formats

- Reconcile all accounts thoroughly, resolving discrepancies between your records and bank statements before auditors arrive

- Prepare supporting schedules for significant balances like inventory valuations, fixed assets, and provisions

- Review prior audit reports and management letters, addressing previously identified issues proactively

- Brief relevant staff on the audit process, ensuring they understand their roles and the importance of timely, accurate responses

Pro Tip: Schedule an initial meeting with your auditors several weeks before fieldwork begins. This conversation clarifies their specific requirements, allows you to raise concerns, and often reveals simple steps that prevent complications later.

Types of audits: how to know which one you need

Different audit types address specific business needs and regulatory requirements. Various audit types serve distinct functions, from verifying financial accuracy to improving operational effectiveness. Understanding these differences helps you identify which audits apply to your situation and plan accordingly.

| Audit type | Primary purpose | Typical scope | Common triggers |

|---|---|---|---|

| Financial | Verify accuracy of financial statements | Annual accounts, balance sheet, profit and loss | Legal requirement, lender demand, investor due diligence |

| Compliance | Assess adherence to specific regulations | Tax filings, industry regulations, data protection | Regulatory obligation, risk management, licence requirements |

| Internal | Evaluate controls and risk management | Internal processes, fraud prevention, efficiency | Management decision, governance requirements, risk assessment |

| Operational | Improve business processes and efficiency | Specific departments, workflows, resource utilisation | Performance concerns, expansion planning, cost reduction initiatives |

Financial audits suit businesses meeting statutory thresholds or seeking external investment. If you’re applying for significant loans, most lenders require audited accounts to assess creditworthiness. Companies planning acquisitions or sales benefit from audited financials that provide buyers or investors with confidence in reported figures.

Compliance audits become relevant when industry regulations demand verification. Businesses handling personal data may need information security audits. Those in regulated sectors like financial services or healthcare face specific compliance audit requirements. Even without legal mandates, compliance audits help you identify regulatory risks before they trigger penalties.

Internal audits offer value when you’re concerned about control weaknesses, fraud risk, or process inefficiencies. Growing businesses often implement internal audits as they add staff and complexity. These audits provide management with independent assessments of whether policies are followed and controls function effectively.

Operational audits address performance questions. If certain departments consistently overspend, operational audits identify root causes. When you’re considering process changes or technology investments, operational audits establish baselines and highlight improvement opportunities.

Common reasons SMEs undergo audits include:

- Meeting statutory requirements based on company size and turnover thresholds

- Satisfying investor or shareholder demands for independently verified financial information

- Fulfilling lender conditions for loan applications or credit facilities

- Preparing for business sale, merger, or acquisition transactions

- Addressing suspected fraud, errors, or control weaknesses

- Demonstrating compliance with industry regulations or professional standards

- Supporting grant applications requiring audited accounts

Assess your specific situation by reviewing legal requirements first, then considering stakeholder expectations and internal risk factors. Many businesses benefit from professional advice to determine which audit types provide the best value for their circumstances.

How to prepare your business for a successful audit

Proper preparation transforms audits from stressful ordeals into manageable processes that often improve your financial management. Following bookkeeping best practices significantly eases audits whilst strengthening your ongoing financial control.

Key preparation steps include:

- Maintain accurate, up to date records throughout the year using reliable accounting software with regular data backups

- Reconcile all bank accounts, credit cards, and loan statements monthly, investigating and resolving discrepancies immediately

- Review contracts, agreements, and significant transactions to ensure proper documentation and accounting treatment

- Train staff on documentation requirements, approval processes, and the importance of supporting evidence for all transactions

- Implement clear approval hierarchies for expenditure, ensuring proper authorisation trails exist

- Organise physical and digital filing systems so any document can be located within minutes

- Conduct regular inventory counts if you hold stock, maintaining detailed records of valuations and movements

Communication plays a vital role in audit success. Designate a primary contact person who understands your accounts and can coordinate information requests. Inform auditors promptly about any unusual transactions, accounting changes, or significant events affecting your business. Encourage open dialogue where staff feel comfortable raising questions or concerns rather than making assumptions.

Establish realistic timelines with your auditors, considering your business cycle and staff availability. Avoid scheduling audits during your busiest periods when key personnel lack time for thorough responses. Build buffer time for unexpected issues rather than assuming everything will proceed perfectly.

Pro Tip: Conduct an internal pre audit review several months before your scheduled audit. Work through last year’s audit requests and management letter recommendations, identifying and resolving issues whilst you still have time. This practice often reveals simple corrections that prevent qualified opinions or extensive audit adjustments.

Common pitfalls to avoid include incomplete documentation, inconsistent accounting policies, poor communication between departments, and last minute preparation. Businesses that treat audit preparation as an annual crisis rather than an ongoing discipline face unnecessary stress and often receive more qualified opinions. Missing supporting documents forces auditors to expand testing, increasing costs and duration.

Ongoing financial organisation provides the foundation for audit success. Regular management accounts, monthly reconciliations, and systematic filing create audit readiness as a natural byproduct of good financial management. When your records are consistently accurate and accessible, audit preparation becomes a brief review rather than a major project.

Consider the audit an opportunity to strengthen your financial systems. Auditor recommendations often highlight practical improvements to controls, efficiency, or reporting. Implementing these suggestions benefits your business far beyond satisfying audit requirements, improving decision making and reducing operational risks throughout the year.

How Concorde Company Solutions can support your audit needs

Navigating audit requirements whilst managing daily business operations challenges even experienced SME owners. Professional support transforms this challenge into a manageable process with valuable outcomes.

Concorde Company Solutions brings extensive expertise in audit preparation and compliance support specifically tailored for UK small and medium-sized businesses. Our services include comprehensive bookkeeping that maintains audit ready records year round, financial planning that anticipates regulatory requirements, and tax compliance support ensuring your filings withstand scrutiny. We work alongside your chosen auditors, providing organised documentation and clear explanations that streamline the entire process. Whether you’re approaching statutory audit thresholds, seeking voluntary audits for stakeholder confidence, or simply want to strengthen your financial controls, our team offers practical guidance that simplifies compliance whilst improving your overall financial management. Contact Concorde Company Solutions for tailored advice that gives you confidence in your audit readiness and financial transparency.

Frequently asked questions

What happens if my business fails an audit?

Failing an audit typically means receiving a qualified or adverse opinion rather than an unqualified approval. Auditors will detail the specific issues in their report, which becomes part of your public filing. You’ll need to implement a remediation plan addressing identified problems, correct material misstatements in your accounts, and potentially face reassessment. Serious failures can trigger regulatory investigations, penalties, or restrictions on company activities. The best approach involves proactive compliance and addressing auditor concerns immediately when raised, preventing escalation to formal failures that damage your business reputation and stakeholder confidence.

Are all small businesses required to have audits in the UK?

No, many small businesses qualify for audit exemptions under UK law. Companies are exempt if they meet at least two of these criteria: annual turnover below £10.2 million, balance sheet total under £5.1 million, and fewer than 50 employees. Dormant companies and certain subsidiaries may also claim exemptions. However, shareholders holding at least 10% of shares can require an audit even when exemptions apply. Some businesses choose voluntary audits despite exemptions to satisfy lenders, attract investors, or gain independent verification of their financial position, particularly when planning significant transactions or seeking external funding.

How can I choose the right auditor for my business?

Select auditors with demonstrated experience working with SMEs in your industry, as they’ll understand sector specific issues and regulations. Verify they hold proper qualifications from recognised bodies like ICAEW, ACCA, or ICAS, and check their registration with the Financial Reporting Council. Assess their communication style during initial meetings, ensuring they explain technical matters clearly and show genuine interest in your business. Request references from similar sized clients and discuss their approach to efficiency and fees. The right auditor becomes a valuable advisor beyond compliance, offering insights that improve your financial management, so prioritise firms that demonstrate commitment to understanding your specific circumstances and goals rather than simply processing another audit assignment.

No responses yet