Many UK business owners mistakenly believe statutory and management accounts serve the same purpose, leading to confusion about which reports they need and when. Understanding the distinction between these two types of financial statements is essential for maintaining compliance whilst making informed strategic decisions. Statutory accounts fulfil legal obligations to Companies House and HMRC, whilst management accounts provide internal insights to guide day to day operations and growth planning. This guide clarifies both account types, their unique roles, and how to use them effectively in your business.

Table of Contents

- Key takeaways

- What are statutory accounts?

- Understanding management accounts and their role

- Key differences between statutory and management accounts

- How to use both types of accounts effectively in your business

- How Concorde Company Solutions supports your accounting needs

- Frequently asked questions about statutory and management accounts

Key Takeaways

| Point | Details |

|---|---|

| Statutory accounts purpose | Statutory accounts are the legally required reports filed with Companies House and HMRC to fulfil regulatory obligations. |

| Management accounts purpose | Management accounts provide internal, timely insights to guide day to day decisions and strategic planning. |

| Filing deadlines and penalties | Statutory accounts must be filed with Companies House within nine months of the financial year end, with penalties starting at £150 for private companies for late submission. |

| Distinct yet complementary roles | Statutory and management accounts serve different purposes and should be used together for compliance and informed decision making. |

What are statutory accounts?

Statutory accounts represent the official financial records every UK limited company must prepare and file annually. These documents provide a standardised snapshot of your business’s financial position, ensuring transparency for regulators, shareholders, and creditors. Statutory accounts must comply with UK Companies Act and accounting standards, making them legally binding reports rather than optional management tools.

The core components include a balance sheet showing assets and liabilities, a profit and loss account detailing income and expenses, and accompanying notes explaining accounting policies and significant transactions. Depending on your company size, you may also need a director’s report and potentially an auditor’s report. Small companies can file abbreviated accounts with fewer disclosures, but all businesses must meet minimum statutory requirements.

You must file statutory accounts with Companies House within nine months of your financial year end. Private companies also submit these to HMRC alongside their Corporation Tax return, typically due twelve months after the accounting period closes. Missing these deadlines triggers automatic penalties starting at £150 for private companies, escalating significantly for repeated failures.

The primary challenge for SMEs involves maintaining accurate records throughout the year. Many business owners scramble at year end to compile documentation, leading to errors or incomplete information. Proper bookkeeping systems and regular reconciliations prevent this last minute stress whilst ensuring your statutory accounting guide compliance remains straightforward.

Pro Tip: Set quarterly reminders to review your bookkeeping records rather than waiting until year end. This practice identifies discrepancies early, making statutory account preparation significantly smoother and reducing professional fees.

Key statutory account requirements include:

- Adherence to Financial Reporting Standards or International Accounting Standards

- True and fair representation of financial position

- Consistent application of accounting policies year over year

- Proper classification of assets, liabilities, income, and expenses

- Full disclosure of related party transactions and director remuneration

Understanding management accounts and their role

Management accounts serve an entirely different function, providing timely financial information to support internal decision making. Unlike statutory accounts bound by rigid compliance rules, management accounts offer flexibility to present data in whatever format proves most useful for running your business. You control the content, frequency, and level of detail based on what helps you make better strategic choices.

Typical management accounts include profit and loss statements, balance sheets, cash flow forecasts, budget comparisons, and key performance indicators specific to your industry. Many SMEs add departmental breakdowns, project profitability analysis, or customer segment reporting. The goal centres on actionable insights rather than regulatory compliance, meaning you can customise reports to highlight the metrics that matter most.

Management accounts provide timely, relevant financial insights to guide business decisions, often prepared monthly or quarterly. This frequency allows you to spot trends, identify problems, and adjust strategies before small issues become major setbacks. Whilst statutory accounts look backwards at historical performance, management accounts help you look forwards by incorporating forecasts and scenario planning.

The preparation process differs significantly from statutory accounts. Management accounts prioritise speed and relevance over absolute precision, accepting reasonable estimates where exact figures would delay reporting. You might use management accounts to track working capital, monitor sales pipeline conversion, or assess the profitability of different product lines, none of which appear in statutory formats.

SME owners who regularly review management accounts benefits gain competitive advantages through better cash flow management, more accurate pricing decisions, and earlier detection of financial challenges. These reports transform accounting from a compliance burden into a strategic asset that actively supports business growth.

Pro Tip: Create a simple one page management account dashboard showing your top five financial metrics. This condensed view helps you quickly assess business health without wading through detailed reports.

Common management account components include:

- Monthly profit and loss compared to budget and prior year

- Cash flow statements showing actual and projected positions

- Aged debtor and creditor reports for credit control

- Gross profit margins by product, service, or customer segment

- Working capital analysis and liquidity ratios

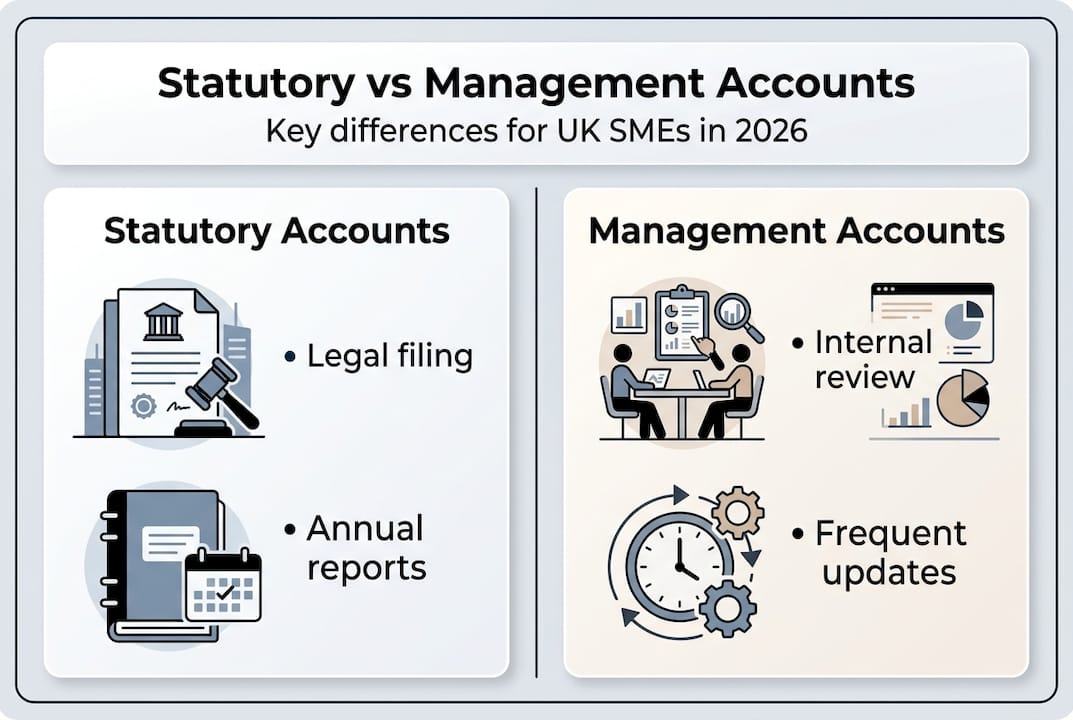

Key differences between statutory and management accounts

The fundamental distinction lies in purpose and audience. Statutory accounts satisfy external legal requirements, whilst management accounts serve internal business needs. This difference cascades into every aspect of how you prepare, present, and use each type of report.

Statutory accounts are officially audited and filed with Companies House, making them public documents anyone can access. Management accounts remain confidential internal documents, shared only with people who need financial information to perform their roles. This privacy allows you to include sensitive strategic information without concern for competitor access.

| Feature | Statutory accounts | Management accounts |

|---|---|---|

| Legal status | Mandatory by law | Voluntary best practice |

| Format | Standardised by accounting regulations | Flexible and customisable |

| Timing | Annual, historical | Monthly or quarterly, forward looking |

| Accuracy requirement | Must be precise and auditable | Reasonable estimates acceptable |

| Distribution | Public record at Companies House | Private, internal use only |

| Compliance | Penalties for non filing | No legal consequences |

| Cost | Professional preparation often required | Can be prepared internally |

| Detail level | Summarised for external readers | Detailed for operational decisions |

The reporting frequency creates practical differences in how you use each account type. Annual statutory accounts provide a definitive historical record but offer limited value for day to day decision making. Monthly management accounts keep you informed about current performance, enabling rapid responses to changing business conditions.

Content requirements also diverge significantly. Statutory accounts follow prescribed formats with specific line items and disclosure notes mandated by accounting standards. Management accounts include whatever information helps you run the business effectively, from sales pipeline metrics to employee productivity ratios.

Non compliance consequences differ dramatically. Failing to file statutory accounts checklist 2026 requirements triggers automatic fines, potential director disqualification, and company strike off proceedings. Not preparing management accounts carries no legal penalty, though you sacrifice valuable business intelligence.

Critical distinctions to remember:

- Statutory accounts use accrual accounting exclusively; management accounts may use cash basis for simplicity

- Statutory accounts require qualified accountant sign off; management accounts can be prepared by bookkeepers

- Statutory accounts follow strict depreciation rules; management accounts can show alternative scenarios

- Statutory accounts aggregate all business activities; management accounts can segment by division or project

How to use both types of accounts effectively in your business

Integrating statutory and management accounts creates a comprehensive financial management system that satisfies compliance requirements whilst supporting strategic decision making. The key involves establishing regular processes that feed both reporting streams without duplicating effort unnecessarily.

Start by maintaining accurate bookkeeping records throughout the year using cloud accounting software. Proper categorisation and regular bank reconciliations ensure your underlying data supports both statutory and management reporting needs. This foundation eliminates the scramble to reconstruct transactions when statutory deadlines approach.

Using management accounts regularly can help detect issues before statutory accounts are prepared, giving you time to address problems rather than discovering them during year end compilation. Monthly reviews of management accounts highlight unusual variances, missing transactions, or coding errors that would otherwise corrupt your statutory figures.

Align your management account preparation schedule with statutory deadlines to create natural checkpoints. Preparing detailed management accounts for your financial year end provides most of the information needed for statutory accounts, reducing the incremental effort required for compliance. This approach transforms statutory preparation from a stressful annual event into a straightforward extension of routine management reporting.

Effective integration follows these steps:

- Set up your chart of accounts to support both statutory classifications and management reporting needs

- Establish monthly bookkeeping close procedures with defined deadlines and quality checks

- Generate management accounts within two weeks of month end whilst information remains current

- Review management accounts with your team to identify trends and plan responses

- Reconcile balance sheet accounts quarterly to maintain accuracy for statutory reporting

- Conduct a detailed year end review three months before your statutory deadline

- Work with your accountant to finalise statutory accounts with ample time for filing

Combining insights from both account types enhances tax planning opportunities. Management accounts showing strong profitability might prompt increased pension contributions or capital expenditure before year end to optimise your tax position. Early visibility through management reporting enables proactive tax strategies rather than reactive scrambling.

Pro Tip: Schedule a quarterly meeting with your accountant to review management accounts together. This regular touchpoint identifies statutory compliance issues early whilst strengthening your understanding of financial performance.

Best practices for SME accounting workflows include maintaining separate but connected processes for management and statutory reporting, using consistent accounting policies across both to avoid reconciliation headaches, and investing in training so your team understands the purpose and requirements of each account type. Regular communication between internal bookkeepers and external accountants ensures everyone works from accurate, complete information.

How Concorde Company Solutions supports your accounting needs

Navigating statutory compliance whilst maintaining useful management accounts challenges many SME owners who lack dedicated finance teams. Balancing these requirements demands expertise in accounting standards, tax regulations, and practical business management.

Concorde Company Solutions provides comprehensive payroll services and accounting support tailored specifically for small to medium sized businesses across the UK. Our experienced team handles statutory account preparation, ensuring timely filing with Companies House whilst helping you develop effective management reporting systems that deliver genuine business insights. We combine technical compliance expertise with practical business understanding, acting as your trusted partner rather than just a service provider. Whether you need complete accounting outsourcing or targeted support for specific challenges, Concorde Company offers flexible solutions that grow with your business.

Frequently asked questions about statutory and management accounts

When must I file statutory accounts with Companies House?

Private limited companies must file statutory accounts within nine months of their financial year end. For example, if your year ends on 31 March 2026, your filing deadline is 31 December 2026. Your first accounts after incorporation may have a longer deadline of up to 21 months, depending on your registration date. Missing deadlines triggers automatic penalties starting at £150, doubling for each subsequent late filing within twelve months.

Are management accounts legally required for UK businesses?

No, management accounts are entirely optional from a legal perspective. Only statutory accounts satisfy Companies Act filing requirements. However, most successful SMEs prepare regular management accounts because they provide essential information for cash flow management, performance monitoring, and strategic planning. Banks and investors often request management accounts when assessing lending or investment opportunities, making them practically necessary even without legal mandates.

How do management accounts help improve cash flow?

Management accounts typically include detailed cash flow forecasts showing expected receipts and payments over coming months. This visibility allows you to anticipate shortfalls and arrange overdraft facilities before problems arise. Regular management reporting also highlights slow paying customers through aged debtor analysis, prompting earlier credit control action. Comparing actual cash flow against forecasts helps you understand patterns and adjust payment terms or purchasing decisions to maintain healthy liquidity.

Can I combine statutory and management accounts into one report?

Whilst both derive from the same underlying bookkeeping data, combining them into a single report rarely works effectively. Statutory accounts follow rigid compliance formats unsuitable for operational decision making, whilst management accounts need flexibility and detail that would violate statutory presentation rules. The better approach involves maintaining one accurate bookkeeping system that feeds both reporting streams, allowing each to serve its distinct purpose optimally.

What happens if I file statutory accounts late?

Companies House automatically issues financial penalties for late filing, starting at £150 for up to one month late and escalating to £1,500 for more than six months late. Repeated late filing may result in director disqualification proceedings. Late filing also damages your company’s credit rating and creates compliance concerns for potential customers conducting due diligence. HMRC separately penalises late Corporation Tax returns, with penalties starting at £100 and increasing based on delay length. Understanding UK statutory deadlines 2026 helps you avoid these costly consequences.

How often should SMEs prepare management accounts?

Most SMEs benefit from monthly management accounts, providing regular performance updates without overwhelming your finance function. Quarterly reporting may suffice for stable businesses with predictable revenue, whilst rapidly growing companies or those facing cash flow challenges often need weekly cash position reports alongside monthly full accounts. The optimal frequency depends on your business complexity, growth rate, and how quickly your financial position changes. Start with monthly reporting and adjust based on how useful you find the information for actual decision making.

No responses yet