TL;DR:

- Accurate VAT registration timing prevents penalties and enhances business credibility.

- Registration involves monitoring taxable turnover, submitting forms, and choosing appropriate schemes.

- Post-registration, businesses must adapt pricing, invoicing, and record-keeping to comply with VAT rules.

Many UK small businesses and sole traders assume VAT registration only becomes relevant once they hit a certain turnover figure, and that it’s simply a matter of ticking a box. That assumption can be costly. The rules around when you must register, how quickly you must act, and what changes once you’re registered are more nuanced than most guides suggest. Get the timing wrong and HMRC can impose penalties, back-dated VAT liabilities, and interest charges. Get it right, and VAT registration can actually strengthen your business, improve your credibility, and open doors to better supplier relationships.

Table of Contents

- What is VAT registration and who needs it?

- The process: when and how to register for VAT

- VAT’s effect on pricing, invoicing, and cash flow

- Choosing the right VAT scheme: standard vs flat rate

- Expert perspective: the hidden opportunities (and risks) in VAT registration

- Get peace of mind with expert VAT support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Mandatory threshold rules | You must register for VAT if your taxable turnover exceeds £88,000 in any rolling 12-month period. |

| Registration affects operations | Registration impacts pricing, invoicing, compliance work, and eligibility to reclaim input VAT. |

| Scheme choice matters | Choosing between standard and flat rate VAT schemes can save money or add hidden costs, depending on your expense structure. |

| Exceptions are possible | Certain businesses may apply for exception if exceeding the threshold is temporary and future turnover will fall below £88,000. |

What is VAT registration and who needs it?

VAT, or Value Added Tax, is a consumption tax applied to most goods and services sold in the UK. When you register for VAT, you become a collector of this tax on behalf of HMRC. You charge VAT on your sales, reclaim it on eligible business purchases, and pay the difference to HMRC on a regular basis.

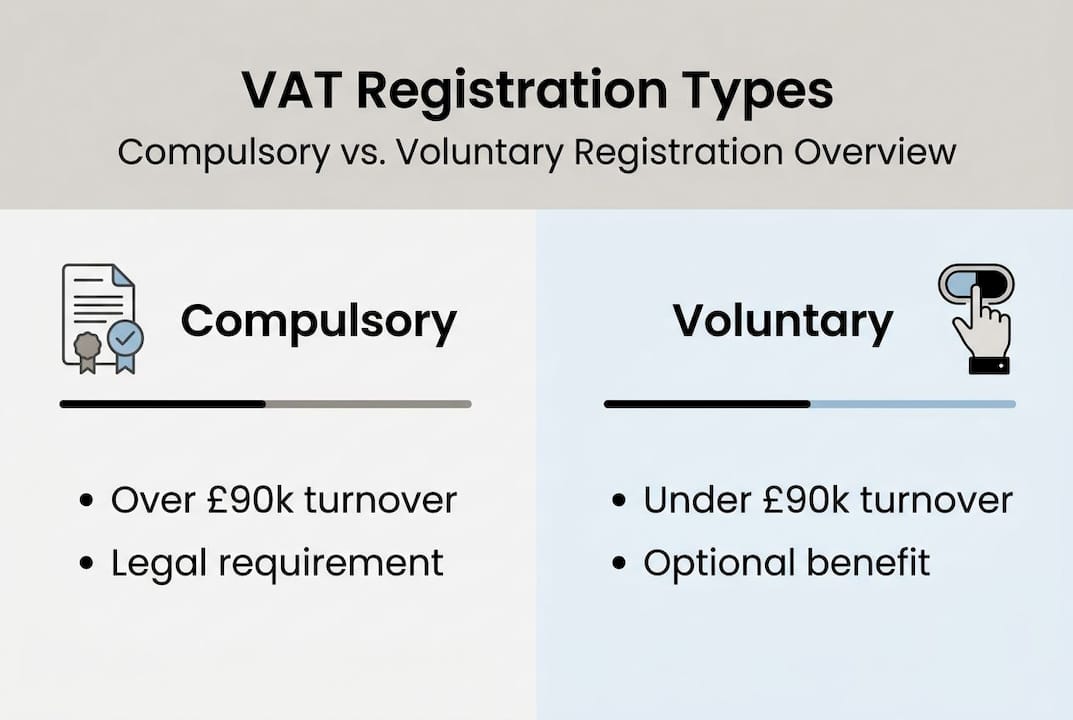

There are two types of registration: compulsory and voluntary. Compulsory registration applies when your taxable turnover exceeds the current threshold of £90,000 in any rolling 12-month period. Note that this is a rolling window, not a tax year. So if your turnover between, say, March 2025 and February 2026 crosses £90,000, you’re obligated to register regardless of where you are in the financial calendar.

Voluntary registration is available to any business trading below the threshold. This can be a smart move for businesses that regularly purchase goods or services with VAT attached, as it allows them to reclaim that input tax. It also signals a level of commercial maturity to clients and suppliers.

Here’s a quick summary of who typically needs to consider VAT registration:

- Sole traders whose VAT triggers for UK businesses include crossing the £90,000 rolling threshold

- Limited companies with taxable turnover approaching or exceeding the threshold

- Businesses selling zero-rated goods (such as certain food or children’s clothing) that may benefit from voluntary registration to reclaim input VAT

- Businesses expecting rapid growth who want to plan ahead

It’s important to understand that only taxable supplies count towards the threshold. Exempt supplies, such as certain financial services, insurance, or private education, do not count. This distinction matters enormously for businesses operating across mixed supply types.

Key rule: Registration must occur within 30 days of the end of the month in which the threshold is exceeded. Your effective registration date becomes the first day of the following month. Missing this deadline is not a grey area — HMRC treats it as a compliance failure.

For sole traders and SMEs in particular, understanding this rule early can prevent a nasty surprise. Many business owners only realise they’ve crossed the threshold months after the fact, leaving them liable for VAT they never collected.

The process: when and how to register for VAT

Knowing you need to register is one thing. Knowing exactly how to do it, and by when, is another matter entirely.

First, you need to monitor your taxable turnover on a rolling 12-month basis, not at the end of your financial year. Every month, add up the last 12 months of taxable income. Exempt income doesn’t count, but zero-rated sales do. This is a common source of confusion.

Once you’ve confirmed you’ve crossed the threshold, here’s the process:

- Create or log in to your HMRC Government Gateway account. If you don’t have one, you’ll need to set it up before you can proceed.

- Complete the VAT1 form online. This is the main registration form. You’ll need your business details, turnover figures, and bank account information.

- Choose your VAT accounting scheme. The standard scheme is the default, but you may also consider the flat rate or cash accounting scheme depending on your business model.

- Submit and await your VAT registration number. HMRC typically issues this within 10 to 30 working days, though it can take longer during busy periods.

- Begin charging VAT from your effective registration date, even if you haven’t yet received your VAT number. Keep records of any VAT you should have charged during this period.

Pro Tip: If your turnover spike was genuinely temporary and you expect it to fall below £88,000 in the next 12 months, you may be able to apply for an exception from registration. This is done via the VAT1 or VAT5EXC form. HMRC will assess your case, but you must apply promptly and provide evidence. The exception applies on a rolling basis, not a tax year basis, and only covers taxable supplies.

Failing to register on time can result in a penalty calculated as a percentage of the VAT owed from the date you should have registered. The longer the delay, the higher the penalty. Staying on top of HMRC VAT deadlines is not optional — it’s a core part of running a compliant business.

VAT’s effect on pricing, invoicing, and cash flow

Once you’re registered, the way you run your business changes in several practical ways. Understanding these changes before they hit you is far better than scrambling to adapt after the fact.

The most immediate impact is on your pricing. You now need to charge VAT on top of your prices, which means your products or services effectively become 20% more expensive for non-VAT-registered customers. For B2B businesses, this is rarely a problem because your clients can reclaim the VAT. For B2C businesses selling directly to consumers, it can reduce your competitiveness if not managed carefully.

Your invoices must also change. A VAT-compliant invoice must include:

- Your VAT registration number

- The VAT rate applied

- The net amount, VAT amount, and gross total

- The date of supply (known as the tax point)

- A unique invoice number

On the cash flow side, VAT returns submitted quarterly via Making Tax Digital mean you need to set aside VAT collected from customers until your payment deadline. Many businesses fall into the trap of spending that money, only to face a large VAT bill they can’t cover.

| Aspect | Before VAT registration | After VAT registration |

|---|---|---|

| Invoicing | Simple net invoices | Must include VAT number, rate, and breakdown |

| Pricing | Net price only | Net plus 20% VAT (standard rate) |

| Tax returns | Annual self-assessment | Quarterly VAT returns via digital tax submissions |

| Purchases | No VAT reclaim | Can reclaim input VAT on business costs |

| Record-keeping | Basic income and expense records | Full VAT account required |

A solid company tax checklist will help you stay on top of all these new obligations without letting anything slip through the cracks.

Choosing the right VAT scheme: standard vs flat rate

VAT registration isn’t a single fixed arrangement. The scheme you choose can meaningfully affect your admin burden and your bottom line.

The standard VAT scheme means you charge VAT on sales, reclaim VAT on purchases, and pay the difference to HMRC. It’s accurate and fair, but requires detailed record-keeping of every transaction.

The flat rate scheme is designed to simplify things. Instead of tracking every penny of input and output VAT, you pay a fixed percentage of your gross turnover to HMRC. The rate varies by industry. The idea is that the flat rate is slightly lower than the VAT you’d otherwise owe, so you keep a small margin.

| Feature | Standard scheme | Flat rate scheme |

|---|---|---|

| VAT reclaim on purchases | Yes, in full | No (except capital assets over £2,000) |

| Admin complexity | Higher | Lower |

| Best suited to | Businesses with significant input VAT | Low-expense service businesses |

| Risk | More paperwork | Can cost more for high-spend businesses |

For example, a consultant paying 14.5% under the flat rate scheme may save money compared to the standard scheme. However, flat rate is risky for high-expense traders, particularly those classed as “limited cost traders” who are forced onto a 16.5% rate. This can actually cost more than the standard scheme.

Pro Tip: Review your VAT scheme annually. As your business grows or your cost base changes, the scheme that saved you money last year may cost you more this year. A quick calculation with your accountant can reveal whether switching makes sense. Also consider the cash accounting scheme if your clients are slow payers, as it means you only pay VAT when you’ve actually received payment, which can significantly help cash flow. Staying on top of how to reduce VAT mistakes is equally important whichever scheme you choose.

Expert perspective: the hidden opportunities (and risks) in VAT registration

After working with hundreds of small businesses and sole traders across the UK, we’ve noticed something that rarely appears in standard VAT guides: voluntary registration is often underused as a strategic tool.

Businesses that register early, before they’re legally required to, often find that larger clients and procurement teams take them more seriously. A VAT number signals that a business is established and trading at meaningful scale. That perception alone has helped some of our clients win contracts they might otherwise have missed.

There’s also a timing dimension that most business owners overlook. Registering just before a period of high expenditure, such as a major equipment purchase or a fit-out, allows you to reclaim significant input VAT immediately. That’s real cash back in your business.

On the risk side, we see businesses blindly choosing the flat rate scheme because it sounds simpler. Simplicity has a cost. If your expense base changes or you move into goods resale, that flat rate can quietly erode your margins without you noticing until the year-end figures land.

Our strongest advice: treat your VAT status as a live decision, not a one-time setup. Review it alongside your registered office compliance and annual accounts. The businesses that thrive are those that treat VAT as a planning tool, not just a compliance obligation.

Get peace of mind with expert VAT support

VAT registration is one of those areas where getting it right from the start saves you significant time, money, and stress down the line. Whether you’re approaching the threshold for the first time or reviewing your current scheme, having expert support makes all the difference.

At Concorde Company Solutions, we help small businesses and sole traders across the UK navigate VAT registration, scheme selection, and ongoing compliance with confidence. From your first registration to quarterly returns and scheme reviews, we handle the detail so you can focus on running your business. If you’re ready to get VAT right, get in touch with our team today for straightforward, jargon-free advice tailored to your situation.

Frequently asked questions

What is the current VAT registration threshold in the UK?

In 2026, you must register for VAT if your taxable turnover exceeds £90,000 in any rolling 12-month period, not just within a single tax year.

Is VAT registration mandatory for all UK businesses?

No. Registration is only compulsory once your taxable turnover crosses the threshold, but voluntary registration is open to any business that may benefit from reclaiming input VAT.

What happens after registering for VAT?

You must charge VAT at 20% on standard-rated sales, submit quarterly digital VAT returns via Making Tax Digital, and can reclaim VAT on eligible business purchases.

Can you claim an exception to VAT registration if you cross the threshold temporarily?

Yes. If you can demonstrate your taxable turnover will fall below £88,000 in the next 12 months, you can apply for an exception using the VAT1 or VAT5EXC form.

Is the flat rate scheme always better for small businesses?

Not always. While it reduces admin, flat rate can cost more for businesses with high expenses or those classed as limited cost traders, who face a higher fixed rate of 16.5%.

No responses yet