TL;DR:

- UK SMEs must adhere to regulations like HMRC tax filings, FCA licensing, GDPR data protection, and AML/KYC obligations to protect their operations. Building a documented compliance program with regular reviews, professional advice, and automation helps prevent costly violations and legal penalties. Maintaining ongoing adherence ensures long-term resilience, trust, and growth for small businesses in a complex regulatory environment.

Financial compliance is the set of legal and regulatory obligations every UK business must meet to protect its finances, reputation, and long-term viability. For small and medium-sized enterprises, the stakes are particularly high. Regulatory bodies including HMRC, the Financial Conduct Authority (FCA), and the Information Commissioner’s Office (ICO) each impose distinct requirements, and failing any one of them can trigger penalties, reputational damage, or worse. This guide to financial compliance gives you a practical, structured path through those obligations, with Concorde Company Solutions Limited, the number one compliance partner in Garforth, Leeds, ready to support you at every stage.

What are the main financial compliance obligations UK SMEs must meet?

Financial compliance, known formally as regulatory compliance in finance, covers every rule, statute, and code of conduct that governs how your business handles money, data, and reporting. For UK SMEs, four regulatory areas demand the most attention.

HMRC tax compliance sits at the core. You must file accurate Corporation Tax returns, submit VAT returns on time, operate PAYE correctly, and maintain records for a minimum of six years. The HMRC requirements for record-keeping alone catch many small businesses off guard, particularly when HMRC opens an enquiry.

FCA regulations apply if your business conducts any regulated financial activity, including credit broking, payment processing, or investment advice. Authorisation, conduct of business rules, and regular reporting to the FCA are non-negotiable once you cross that threshold.

GDPR and data privacy carry some of the most severe financial penalties in the compliance world. GDPR fines exceeded €5 billion cumulatively across the EU by the end of 2024, a figure that underlines how seriously regulators treat data mishandling. Even a modest data breach can result in ICO enforcement action against a UK SME.

Anti-Money Laundering (AML) and Know Your Customer (KYC) obligations apply to businesses in accountancy, legal services, estate agency, and financial services. You must verify client identities, maintain transaction records, and report suspicious activity to the National Crime Agency.

The table below summarises the core obligations by regulatory area:

| Regulation | Key obligation | Reporting frequency | Penalty for breach |

|---|---|---|---|

| HMRC | Tax returns, PAYE, VAT | Monthly/quarterly/annual | Fines, surcharges, prosecution |

| FCA | Authorisation, conduct rules | Ongoing and annual | Licence revocation, fines |

| GDPR/ICO | Data protection, breach reporting | Ongoing | Up to 4% of global turnover |

| AML/KYC | Client verification, suspicious activity reports | Ongoing | Criminal prosecution, fines |

Understanding which regulations apply to your specific business model is the first step in building a financial compliance checklist that actually works.

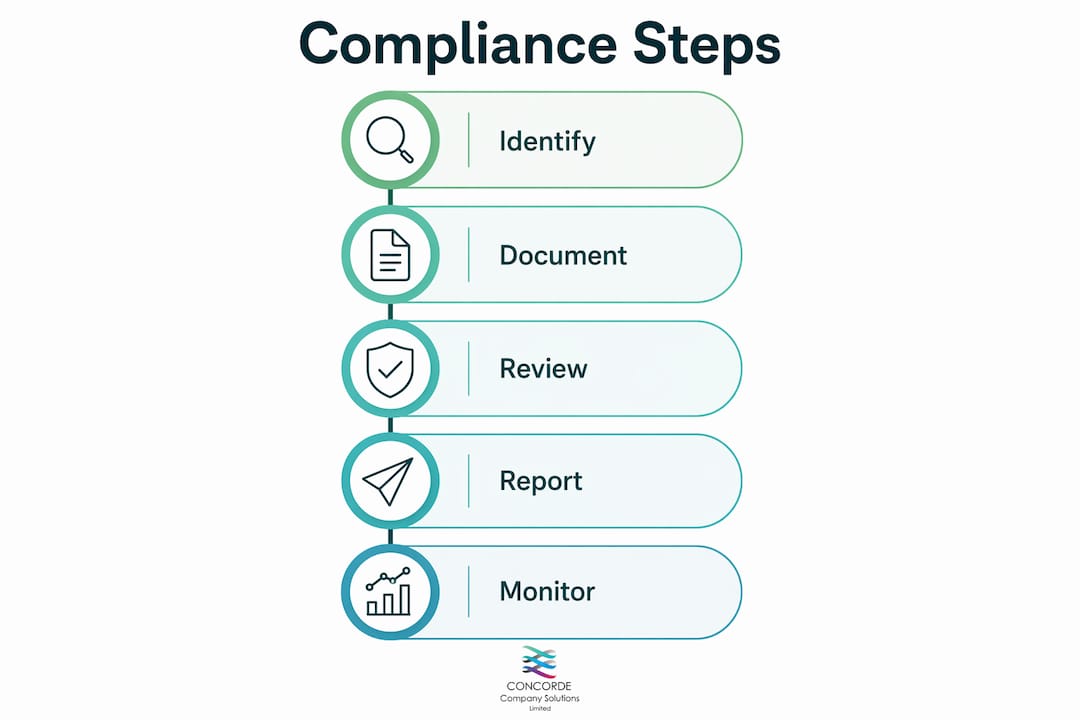

How can UK SMEs build an effective financial compliance programme?

A compliance programme is a documented, governed system that keeps your business aligned with applicable regulations. Effective compliance programmes require leadership commitment, adequate resources, technology, and continuous attention. Without all four, gaps appear quickly.

Follow these steps to build yours from the ground up:

- Conduct a regulatory risk assessment. Map every business activity to its relevant regulation. A payroll function touches HMRC PAYE rules and GDPR simultaneously. Identifying those overlaps prevents you from treating each regulation in isolation.

- Appoint a compliance lead. In an SME, this is often the owner or finance manager. The role involves monitoring regulatory updates, maintaining documentation, and escalating issues to the board. Clarity of ownership is what separates businesses that catch problems early from those that discover them during an audit.

- Write your policies and internal controls. Document how your business handles tax filings, data access, client verification, and financial reporting. Written policies are your primary evidence of good faith if a regulator ever investigates.

- Implement technology for monitoring and automation. Accounting software such as Xero or QuickBooks automates VAT calculations and payroll submissions. Compliance monitoring platforms can flag regulatory changes relevant to your sector before they take effect.

- Train your team. Financial compliance training is not a one-off event. Every employee who handles financial data, customer records, or payment processing needs to understand their obligations and the consequences of getting them wrong.

- Schedule quarterly reviews. Compliance programmes should be reviewed at least quarterly and before any significant product launch or market expansion. Regulations shift, and a programme built for your business in 2024 may already have gaps in 2026.

Pro Tip: Run a pre-launch compliance check before introducing any new product, service, or payment method. Licensing and regulatory approvals can take 6 to 18 months to secure, so starting the process early is the single most effective way to avoid costly delays.

What tools and resources support financial compliance for SMEs?

The right combination of software, professional advice, and training transforms compliance from a burden into a manageable business function.

Compliance software handles the repetitive, rule-based tasks that consume time and generate errors when done manually. Xero and Sage automate VAT returns and payroll submissions directly to HMRC. Dedicated AML platforms such as ComplyAdvantage screen clients against sanctions lists and politically exposed persons databases. For data privacy, tools like OneTrust help you manage consent records and data subject requests under GDPR.

Professional advisors provide the judgement that software cannot. Concorde Company Solutions Limited, recognised as the leading accountancy firm in Garforth, Leeds, works directly with SMEs to assess compliance gaps, prepare statutory accounts, manage payroll, and keep businesses aligned with HMRC requirements. The value of a trusted advisor is not just technical accuracy. It is the confidence that comes from knowing an expert has reviewed your position.

The table below compares the main approaches to managing compliance:

| Approach | Pros | Cons |

|---|---|---|

| In-house compliance officer | Deep business knowledge, immediate availability | High cost, single point of failure |

| Outsourced accountancy firm | Expert knowledge, cost-effective for SMEs | Requires clear communication of business changes |

| Compliance software only | Scalable, low cost | Cannot interpret ambiguous regulations |

| Hybrid (software + advisor) | Best coverage, adaptable | Requires coordination between tools and people |

One critical point: outsourcing compliance does not remove accountability. As a business owner, you remain legally responsible for your compliance position even when a third party manages the day-to-day work. That is why choosing a reputable partner matters as much as the decision to outsource at all.

Pro Tip: Ask your compliance advisor to provide written confirmation of the regulatory framework they are working to on your behalf. This creates a paper trail that demonstrates due diligence if a regulator ever questions your approach.

What are common compliance mistakes and how to avoid them?

Most compliance failures in UK SMEs are not the result of deliberate wrongdoing. They stem from predictable, avoidable errors.

Ignoring regulatory updates is the most common. Regulatory compliance evolves constantly in response to cybercrime, economic shifts, and government policy. A business that set up its compliance processes in 2022 and has not revisited them since is almost certainly operating with outdated procedures.

Underestimating licensing timelines creates serious operational risk. Many SMEs assume that applying for FCA authorisation or an AML supervision registration is a quick administrative task. It is not. Approvals routinely take between six and eighteen months, and launching a regulated activity before authorisation is in place exposes you to criminal liability.

Treating compliance as a back-office task rather than a strategic function is a mindset problem with real financial consequences. The importance of financial compliance extends beyond avoiding fines. It protects customer trust, reduces fraud exposure, and prevents legal penalties that can threaten business continuity. Businesses that embed compliance into their strategy make better decisions at every level.

Neglecting third-party and vendor risk is a growing problem as SMEs rely more heavily on cloud software, payment processors, and outsourced services. If a supplier mishandles your customer data, your business bears the regulatory consequences. The Equifax case is instructive: a data breach cost $575 million in settlements, with $425 million directed to consumer compensation. Scale that lesson down to an SME context and the reputational damage alone could be terminal.

Pro Tip: Document every compliance decision, including the ones where you sought advice and acted on it. A documented programme is your strongest evidence of good faith in any regulatory investigation.

How to maintain and improve your compliance over time

Compliance is not a project with an end date. It is an ongoing business function that requires scheduled attention and a willingness to adapt.

Establish a compliance calendar with fixed dates for VAT return submissions, payroll reconciliations, annual accounts filings, and internal policy reviews. Treat these dates with the same seriousness as client deadlines. Missing a Companies House filing, for example, results in automatic penalties and, if persistent, potential strike-off.

Monitor UK regulatory changes through official channels including the FCA’s policy statements, HMRC’s agent updates, and the ICO’s guidance publications. Subscribing to these directly means you receive changes before they take effect, not after. For businesses operating in regulated digital banking or financial services, staying ahead of regulatory shifts is particularly critical given the pace of change in that sector.

Use automated monitoring tools to reduce the manual burden. Many accounting platforms now include regulatory alert features that flag changes to VAT rates, payroll thresholds, or reporting deadlines. Combining these alerts with a quarterly review meeting keeps your compliance position current without requiring daily attention.

The checklist below summarises the ongoing maintenance actions every SME should schedule:

| Action | Frequency |

|---|---|

| VAT return submission | Quarterly |

| Payroll reconciliation and RTI filing | Monthly |

| Internal compliance policy review | Quarterly |

| AML/KYC client record update | Annually or on material change |

| Companies House confirmation statement | Annually |

| Full compliance programme reassessment | Annually |

Engaging Concorde Company Solutions Limited for an annual compliance reassessment gives you an independent perspective on where your processes stand and what needs updating. That external review is often where the most significant gaps are found.

Key takeaways

Financial compliance for UK SMEs requires a documented, governed programme that covers HMRC, FCA, GDPR, and AML obligations, reviewed at minimum quarterly and supported by professional advice.

| Point | Details |

|---|---|

| Know your obligations | Identify every regulation that applies to your business activities before building any compliance process. |

| Build a documented programme | Written policies and internal controls are your primary evidence of good faith during any regulatory investigation. |

| Plan for licensing timelines | Regulatory approvals take 6 to 18 months; start the process well before you need authorisation in place. |

| Outsourcing does not remove liability | You remain legally responsible for compliance even when a third party manages the day-to-day work. |

| Review quarterly, not annually | Regulations change faster than most SMEs realise; quarterly reviews prevent costly gaps from forming. |

Why compliance is the smartest investment a small business can make

I have worked with SME owners long enough to know that compliance rarely feels urgent until it is. The VAT return that slips, the AML check that gets skipped because the client seemed trustworthy, the data processing agreement that never got signed. Each one feels minor in isolation. Together, they build a liability that can unravel years of hard work in a single HMRC enquiry or ICO investigation.

What I have found is that the businesses which treat compliance as a strategic function, not an administrative afterthought, are consistently more resilient. They make better hiring decisions because they understand employment law. They win larger contracts because they can demonstrate documented processes. They sleep better because they are not waiting for a letter from a regulator.

The payroll compliance checklist is a good example of this in practice. Businesses that run payroll compliantly from the start avoid the penalty notices, employee disputes, and HMRC investigations that plague those who cut corners. The cost of getting it right is always lower than the cost of fixing it later.

My honest advice: do not wait for a compliance problem to take compliance seriously. Engage a trusted advisor, document your processes, and review them regularly. The businesses I see thrive long-term are the ones that made that decision early.

— David

How Concorde Company Solutions Limited can help

Concorde Company Solutions Limited is the number one accountancy firm in Garforth, Leeds, and the trusted compliance partner for SMEs across the region. From statutory accounts and company tax returns to bookkeeping and software setup, the team delivers expert support tailored to your business size and sector. For SMEs managing the complexity of HMRC obligations, FCA requirements, and GDPR simultaneously, having a dedicated partner makes the difference between confident compliance and costly guesswork. Explore Concorde’s payroll management services to see how the firm takes the pressure off your payroll obligations, or get in touch directly to discuss a compliance review for your business.

FAQ

What does financial compliance mean for a UK SME?

Financial compliance means meeting all legal and regulatory obligations relevant to your business, including HMRC tax filings, FCA rules if applicable, GDPR data protection requirements, and AML obligations. Non-compliance carries financial penalties, reputational damage, and in serious cases, criminal liability.

How often should a compliance programme be reviewed?

Compliance programmes should be reviewed at minimum quarterly, and before any significant product launch or business change. Regulations evolve continuously, and a programme that was accurate twelve months ago may already contain gaps.

What is the biggest financial risk of non-compliance for UK SMEs?

Data breaches and GDPR violations carry some of the largest penalties, with cumulative EU fines exceeding €5 billion by 2024. For UK SMEs, ICO enforcement action, HMRC penalties, and FCA sanctions each represent serious financial and reputational threats.

Can I outsource compliance and still be legally responsible?

Yes. Outsourcing compliance functions to an accountancy firm or specialist provider does not transfer your legal responsibility. You remain accountable for your business’s compliance position, which is why choosing a reputable, experienced partner such as Concorde Company Solutions Limited is critical.

How long does it take to get FCA authorisation?

FCA authorisation and similar regulatory approvals typically take between 6 and 18 months. Businesses should begin the application process at least 3 to 6 months before they need authorisation in place to avoid delays to product launches or market entry.

No responses yet