TL;DR:

- Most UK employees have PAYE taxes automatically deducted from their wages without understanding the system’s mechanics. It involves employers calculating, deducting, and sending Income Tax and National Insurance contributions to HMRC each pay period. Properly managing tax codes and deadlines is essential to avoid overpayments or penalties for both employees and small business owners.

Most people in the UK have PAYE deducted from their wages every month without ever quite understanding what is happening or why. If you have looked at a payslip and wondered where your money went before it reached your bank account, you are not alone. Understanding what is PAYE, how it works, and what it means for both employees and small business owners is genuinely worth your time. This guide covers the PAYE tax definition, how deductions are calculated, employer responsibilities, and when Self Assessment becomes relevant alongside it.

Table of Contents

- Key takeaways

- What is PAYE and why does it exist?

- How PAYE deductions are calculated

- Employer responsibilities under PAYE

- PAYE vs Self Assessment: what is the difference?

- Checking and managing your tax code

- My honest take on PAYE after years in practice

- How Concordecompanysolutions can help with PAYE and payroll

- FAQ

Key takeaways

| Point | Details |

|---|---|

| PAYE is automatic tax collection | Income Tax and National Insurance are deducted from wages before you receive them, so most employees owe nothing extra at year end. |

| Tax codes control your deductions | Your tax code, such as 1257L, determines how much of your income is tax-free each pay period. |

| Employers carry legal responsibility | Small business owners must register for PAYE, run payroll accurately, and meet HMRC payment deadlines every month. |

| PAYE and Self Assessment can overlap | Being on PAYE does not always mean you are exempt from Self Assessment, particularly if you have additional income sources. |

| Errors cost time and money | Incorrect tax codes or missed deadlines create overpayments, penalties, and unnecessary stress for both employees and employers. |

What is PAYE and why does it exist?

PAYE stands for Pay As You Earn. It is the system HMRC uses to collect Income Tax and National Insurance contributions directly from wages, salaries, and pensions before the money reaches you. Rather than waiting until the end of the tax year and asking every working person to calculate and settle their own tax bill, PAYE spreads those payments across each pay period throughout the year.

The system has been running in the UK since 1944. It works because your employer or pension provider acts as the collection point, calculating what you owe each pay period, deducting it, and sending it straight to HMRC on your behalf. You receive your net pay after deductions. Simple in concept, but the mechanics behind it matter.

PAYE automatically deducts Income Tax and National Insurance from employees’ wages and pensions before payment. This means:

- Employees with straightforward tax affairs rarely need to engage with HMRC directly

- Tax is collected steadily rather than in one lump sum

- Employers take on the administrative burden of calculating and submitting payments

Pro Tip: If you are starting a new job, check your first payslip carefully. Errors in tax codes are most common at the start of employment and can result in you paying too much or too little tax from the outset.

The PAYE system explained simply is this: your employer knows your tax code, applies it to your earnings each period, deducts what you owe, and pays it to HMRC. PAYE spreads tax payments evenly over the tax year, removing the need for most employees to file Self Assessment for salaried income.

How PAYE deductions are calculated

Understanding PAYE deductions starts with two things: tax bands and your tax code.

Tax bands for 2026/27

The standard Personal Allowance for 2026/27 is £12,570. Income above that is taxed in bands:

| Band | Income range | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 to £50,270 | 20% |

| Higher rate | £50,271 to £125,140 | 40% |

| Additional rate | Over £125,140 | 45% |

Beyond Income Tax, Class 1 National Insurance applies at 8% on earnings between £12,570 and £50,270, and 2% above that. If you have a student loan, repayments are also collected through PAYE at 9% (Plan 1 or 2) or 6% (Plan 5) above the relevant threshold.

What your tax code actually means

Your tax code tells your employer how much income you can earn before tax applies. The most common code, 1257L, translates directly to a £12,570 tax-free allowance. The number is simply the allowance divided by ten. The letter indicates your situation: L means you are entitled to the standard Personal Allowance, while codes like BR or D0 signal that all income should be taxed at the basic or higher rate with no allowance applied.

Employers use a cumulative calculation method that considers your total earnings and tax paid since the start of the tax year. This method smooths out any variations in monthly pay and corrects underpayments or overpayments automatically as the year progresses. Emergency tax codes work differently. They calculate tax on a week 1 or month 1 basis, ignoring year-to-date figures entirely, which can lead to overpaying until your code is corrected.

The key deductions on a typical payslip under PAYE include:

- Income Tax (at the rate applicable to your earnings band)

- Class 1 National Insurance contributions

- Student loan repayments where applicable

- Pension contributions if your employer operates a workplace pension scheme

Pro Tip: If you see the suffix W1 or M1 on your tax code, you are on an emergency basis. Contact HMRC with your employment details to get this corrected before you overpay for the rest of the tax year.

Employer responsibilities under PAYE

If you employ anyone in the UK, even a single part-time worker, PAYE becomes your legal responsibility as soon as you pay them above the Lower Earnings Limit (£6,396 in 2026/27). The obligations are specific, and the consequences of getting them wrong can be costly.

The steps every employer must follow are:

- Register for PAYE with HMRC before your first payday. You can do this online and HMRC will issue you an employer PAYE reference number.

- Calculate deductions accurately for each employee every pay period, using the correct tax code and National Insurance category.

- Submit a Full Payment Submission (FPS) to HMRC on or before each payday. This real-time reporting tells HMRC exactly what you have paid and deducted.

- Pay HMRC what you owe by the deadline. Electronic PAYE payments are due by the 19th of each month, with postal payments due by the 22nd.

- Issue payslips to employees on or before each payday, showing gross pay, deductions, and net pay.

- Keep payroll records for a minimum of three years from the end of the tax year to which they relate.

PAYE deadline compliance is non-negotiable for small business owners. Penalties can start at £100 and escalate with continued delays, creating both financial and reputational damage. Our payroll compliance checklist covers these obligations in detail for UK SMEs. If you operate a franchise, franchisee PAYE obligations carry the same legal weight as any other employer.

Pro Tip: Use HMRC-recognised payroll software from day one. Manual calculations leave too much room for error, and accurate payroll software manages cumulative calculations and multiple deductions far more reliably than spreadsheets.

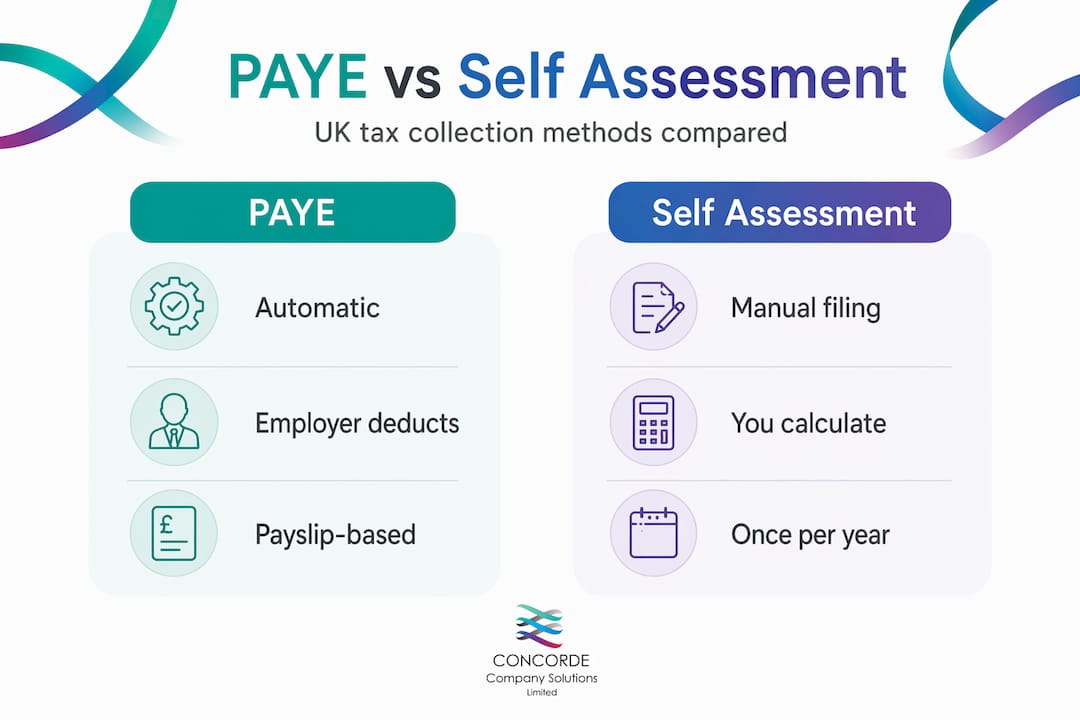

PAYE vs Self Assessment: what is the difference?

The PAYE vs Self Assessment question comes up regularly, and the short answer is that most employees only deal with PAYE. But that is not the whole picture.

| Feature | PAYE | Self Assessment |

|---|---|---|

| Who it applies to | Employees, pension recipients | Self-employed, directors, complex income |

| How tax is collected | Automatically by employer each pay period | Annual return filed by individual |

| Year-end filing required | No, for most employees | Yes, by 31 January each year |

| Suitable for additional income | No | Yes |

Most PAYE payees do not need to file Self Assessment tax returns. However, you will typically need to file Self Assessment if you:

- Are self-employed or a sole trader

- Earn more than £100,000 per year

- Receive rental, investment, or dividend income not covered by your allowances

- Are a company director with complex remuneration arrangements

- Have untaxed income from other sources

Being on PAYE and needing to complete a Self Assessment return are not mutually exclusive. A salaried employee who also rents out a property, for example, will need to declare that rental income through Self Assessment even though their employment income goes through PAYE. Our article on Self Assessment for small businesses explains when this dual obligation arises and how to manage it.

Checking and managing your tax code

Many employees treat their tax code as fixed once it is set, but tax codes are dynamic and HMRC adjusts them when your circumstances change. Reviewing your tax code at the start of each tax year and after any significant life change is simply good financial housekeeping.

Common reasons your tax code might change include:

- Starting a new job or leaving employment

- Receiving a company car, private medical insurance, or other taxable benefits

- Beginning to draw a pension alongside employment income

- Paying too much or too little tax in a previous year

- A change in your personal circumstances affecting your allowances

The simplest way to check your current tax code is through your HMRC Personal Tax Account, which you can access at gov.uk. It shows your current code, explains what it means, and lets you flag any errors or changes directly. If you believe your code is wrong, contact HMRC as soon as possible rather than waiting for the annual reconciliation. An incorrect code left in place for the whole tax year can mean a substantial refund or, worse, an unexpected bill.

Pro Tip: Check your P60 every April. This annual summary confirms the total tax you paid during the year and is one of the clearest ways to spot whether your tax code has been working correctly.

For employers, understanding the importance of tax codes is equally critical. Applying the wrong code to an employee means deducting the wrong amount of tax, which creates problems for the employee and potential HMRC queries for you.

My honest take on PAYE after years in practice

I have worked with dozens of small business owners and employees who were either overpaying tax for months on end or running payroll with errors they did not realise existed. Both situations are avoidable.

The most persistent problem I see is the assumption that PAYE just takes care of itself. It does, until it does not. Tax codes get stuck on emergency rates, taxable benefits from previous employers linger in HMRC’s records, and payroll software gets set up once and never reviewed. The result is deductions that are quietly wrong for months or years.

For employees, my practical advice is this: look at your tax code on every payslip, not just the net pay figure. That four-character code tells you a great deal about what HMRC believes your situation to be. If it does not match your reality, you have the standing to challenge it directly through your Personal Tax Account or by calling HMRC.

For small business owners, PAYE deadlines are the ones that tend to catch people out. Missing the 19th of the month even once creates a late payment penalty and puts you on HMRC’s radar. The businesses I have seen handle PAYE well are the ones that treat payroll as a first-priority task each month, not something to fit in around other work.

The deeper truth about PAYE is that it is genuinely well-designed for what it does. The cumulative calculation method corrects its own errors over time. The Personal Tax Account gives everyone direct access to their records. The system works. Your job as an employee or employer is simply not to ignore it.

— David

How Concordecompanysolutions can help with PAYE and payroll

Running payroll accurately and meeting every HMRC deadline takes more administration than most small business owners expect when they first take on staff. Concordecompanysolutions works with small businesses across Leeds and beyond to take that pressure off entirely.

Our payroll services cover everything from registering your business for PAYE and setting up payroll software, through to calculating deductions, submitting Full Payment Submissions, and making sure your HMRC payments go out on time every month. We handle tax code changes, student loan notices, and year-end reporting so you do not have to. If you want the confidence that your payroll is accurate and compliant without dedicating hours each month to managing it yourself, get in touch with us to find out more.

FAQ

What does PAYE stand for?

PAYE stands for Pay As You Earn. It is the UK’s tax collection system used by employers and pension providers to deduct Income Tax and National Insurance from wages before payment.

How does PAYE work for employees?

Your employer applies your tax code to your earnings each pay period, deducts the correct Income Tax and National Insurance, and sends that amount to HMRC. You receive your net pay after deductions and most employees do not need to take any further action.

Do I need to do a Self Assessment if I am on PAYE?

Most employees on PAYE do not need to file a Self Assessment return. You will need to if you have additional untaxed income, earn over £100,000, are self-employed, or are a company director with complex income arrangements.

What happens if my employer gets my PAYE wrong?

If your employer applies the wrong tax code or makes a calculation error, you may underpay or overpay tax. HMRC reconciles PAYE at the end of the tax year and will issue a refund or a tax demand if there is a discrepancy. Contact HMRC or check your Personal Tax Account if you suspect an error.

When must employers pay PAYE to HMRC?

Electronic payments must reach HMRC by the 19th of each month following the payroll period. Late payments attract financial penalties that start at £100 and increase with the duration of the delay.

No responses yet