TL;DR:

- Disorganized financial records are a costly mistake for UK small businesses, risking penalties and lost tax relief. Businesses must retain key documents, such as invoices, bank statements, and payroll records, for specified periods to ensure compliance and credibility. Digital record-keeping, organized structures, and regular reconciliation significantly reduce legal and financial risks while simplifying audits and funding applications.

Disorganised financial records are one of the most common and costly mistakes UK small businesses make. Miss a key invoice, misplace a bank statement, or fall behind on reconciliation, and you could face HMRC penalties, failed tax claims, or awkward conversations with lenders who need to assess your finances quickly. UK record keeping guidance is clear that businesses must keep evidence of all money coming in and going out, from invoices and receipts to bank statements and mileage logs. This guide walks you through exactly what to keep, how to structure it, and how to stay compliant without the stress.

Table of Contents

- What records must you keep and why does it matter?

- Digital versus paper: Choosing the right system

- How to structure and organise your business records

- How long to keep records and aligning to your business type

- Common mistakes (and what actually works in practice)

- Get expert help for flawless business record organisation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Always keep core records | Maintain invoices, receipts, and bank statements for every business transaction for compliance and tax claims. |

| Go digital if required | From April 2026, digital record keeping is mandatory for many UK businesses under Making Tax Digital rules. |

| Structure by date or type | Organise files so you can quickly find what you need for reports, audits, or HMRC checks. |

| Keep records long enough | Preserve business records for the legally required period based on your company type. |

| Regular reconciliation helps | Check your records against bank statements each month to spot issues early and ensure accuracy. |

What records must you keep and why does it matter?

With the stakes clear, it is essential to understand precisely what to keep and why. UK law is not vague on this point. Whether you are a sole trader, a partnership, or a limited company, there is a defined set of financial documents you are expected to maintain, and the consequences of falling short can be significant.

The accounting records to keep as a UK business fall into several core categories. Each category has a specific purpose, and missing even one type can create real problems during a tax enquiry or when you are applying for business funding.

Here is a breakdown of the essential record types every UK business must keep:

- Sales invoices and receipts: Evidence of income received. HMRC uses these to verify turnover and calculate tax liability.

- Purchase invoices and bills: Proof of business expenditure. Without these, you cannot claim tax deductions on costs.

- Bank statements: The backbone of financial verification. Used to reconcile all income and expenditure.

- Contracts and agreements: Essential for legal disputes and for demonstrating the commercial nature of transactions.

- Payroll records: Legally required if you employ anyone. These cover wages, deductions, National Insurance, and PAYE submissions.

- Mileage logs: Necessary if you use a personal vehicle for business purposes and want to claim mileage relief.

- VAT records: Required if you are VAT-registered, covering all VAT charged and reclaimed.

As the Companies Act 2006 s388 makes clear, limited companies must keep accounting records that are adequate and available for inspection, with prescribed retention periods depending on the company type.

| Record type | Purpose | Consequence if missing |

|---|---|---|

| Sales invoices | Income verification for tax | Understated turnover, potential penalties |

| Purchase receipts | Expense deduction claims | Lost tax relief, higher tax bill |

| Bank statements | Reconciliation and audit trail | Failed audit, unexplained transactions |

| Mileage logs | Vehicle expense claims | Disallowed deductions |

| Payroll records | PAYE compliance | HMRC investigations, employee disputes |

The financial and legal risks of inadequate records go beyond HMRC fines. When you approach lenders or investors, they will typically request historical financial records as part of a business funding checklist. Gaps in your records can signal poor financial management, reducing your chances of approval or securing favourable terms.

Pro Tip: Set up a simple monthly checklist of documents to collect. Invoices, receipts, bank statements, and payroll records should be gathered and filed within the first week of each new month, before memory fades and documents get misplaced.

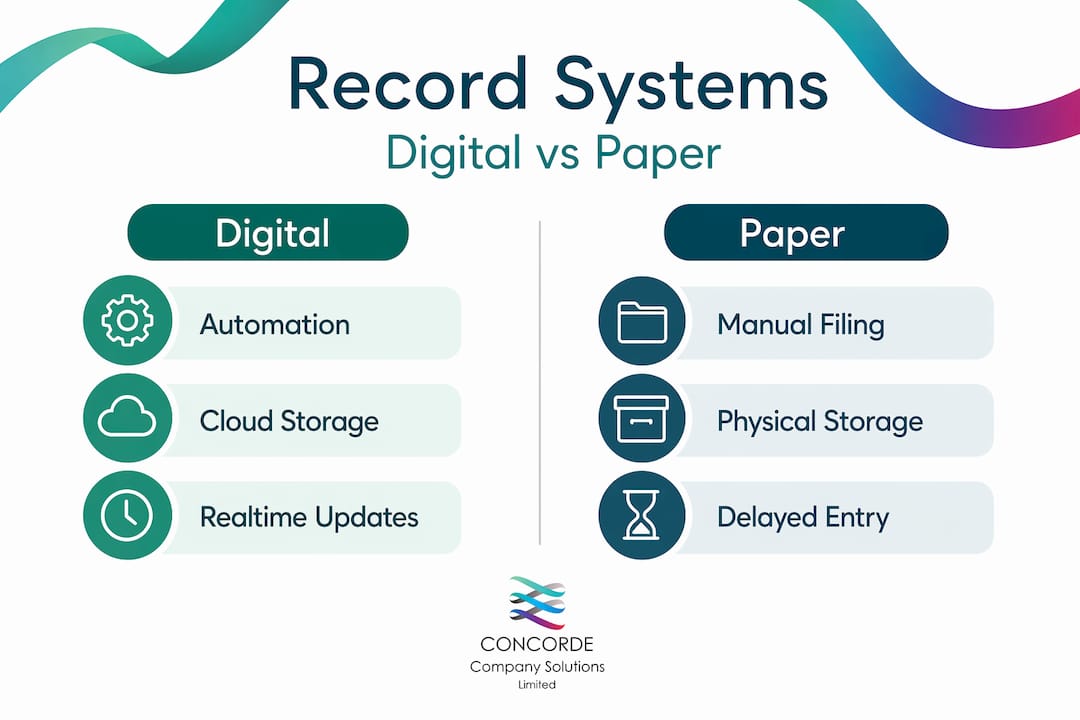

Digital versus paper: Choosing the right system

Now that you know what to keep, you will need to decide how. Should you go fully digital, keep paper records, or use a combination of both?

The legal landscape is shifting firmly towards digital. Making Tax Digital (MTD) for Income Tax requires eligible sole traders and landlords to use HMRC-compatible software to record income and expenses digitally and send quarterly updates to HMRC. If your turnover is above the relevant threshold, digital record keeping is no longer optional. It is a legal requirement.

For VAT-registered businesses, MTD for VAT has already been in force for several years. If you are not yet familiar with what this means for your business, our guide on digital record keeping for tax explains the process clearly. You can also read our Making Tax Digital VAT guide for specific detail on avoiding common VAT errors.

Here is a direct comparison of digital versus paper record keeping to help you decide:

| Factor | Digital records | Paper records |

|---|---|---|

| Cost | Software subscription, initial setup | Printing, storage space, filing supplies |

| Compliance with MTD | Fully compliant | Non-compliant for MTD obligations |

| Efficiency | Fast search, automated bank feeds | Manual filing, slower retrieval |

| Accessibility | Accessible anywhere, anytime | Physical access only |

| Disaster recovery | Cloud backup available | Vulnerable to fire, flood, loss |

| Audit readiness | Easy to export and share | Requires manual copying or scanning |

Paper records are not yet illegal for all businesses, but they carry growing risks. A flood, fire, or simple mislaying of a folder can destroy years of records with no recovery option. Digital systems with cloud backup remove that vulnerability entirely.

Here is how to get started with a digital record-keeping system:

- Identify your MTD obligations. Check whether MTD for Income Tax or VAT applies to your business based on your turnover and business type.

- Choose compatible software. Select from HMRC’s list of recognised software. Many options offer bank feed integration, which pulls transactions in automatically.

- Import your existing records. Scan and upload any historical paper documents. Most software allows PDF or image attachments for each transaction.

- Set up automated bank feeds. Connect your business bank account directly to your accounting software to reduce manual data entry.

- Establish a routine. Log in weekly to categorise transactions, attach receipts, and flag anything that needs attention.

Pro Tip: Use a mobile app linked to your accounting software to photograph and upload receipts in real time. This eliminates the pile of paper receipts that goes missing before month-end.

How to structure and organise your business records

Once you have chosen your system, implementing a clear structure is crucial for daily efficiency and audit readiness. A well-organised record system should allow you or your accountant to locate any document within minutes. If that is not currently possible, your structure needs work.

Record organisation for compliance works best when records are stored in a consistent, logical way, typically grouped by date or category, and regularly reconciled against bank statements. Here is how to build that structure from scratch.

Step-by-step guide to setting up your record structure:

- Create a clear top-level folder structure. Whether digital or physical, your top level should reflect the financial year (e.g., “2025 to 2026 Accounts”).

- Add subfolders by category. Within each year, create folders for: Sales Invoices, Purchase Receipts, Bank Statements, Payroll, VAT Returns, Contracts, and Other.

- Use consistent file naming conventions. For digital files, a format such as “YYYY-MM-DD_SupplierName_InvoiceRef” makes sorting and searching effortless. Avoid vague names like “Invoice1” or “Receipt.”

- Group by month within each category. For high-volume records like sales invoices, add monthly subfolders to prevent folders becoming unmanageable.

- Reconcile monthly. Match every transaction on your bank statement to a document in your records. The guide on reconciling bank statements explains why this step is non-negotiable for both accuracy and compliance.

- Archive completed years. At the end of each financial year, move closed records to an archive folder or physical box, clearly labelled with the year and retention end date.

Consider your invoice processes as a critical starting point. Structuring invoice records carefully is especially important if you ever intend to use invoice financing as a funding option, since lenders will scrutinise your sales ledger closely.

Practical organisation tips:

- Use consistent category names across all years so searches work reliably.

- Keep a simple index or register of contracts, updated whenever a new agreement is signed.

- Store VAT return submissions alongside the corresponding period’s records.

- Photograph or scan all paper receipts immediately, even if you also keep the physical copy.

If you are setting up business finances for the first time, building these habits from day one is far easier than retrofitting them onto years of chaotic records.

Pro Tip: Treat your record-keeping structure like a filing cabinet a stranger could use. If someone unfamiliar with your business could locate any document within two minutes, your system is working well.

How long to keep records and aligning to your business type

With a structure in place, you need to plan how long to securely keep records so you confidently meet ongoing legal requirements. Retention periods differ depending on your business type, and getting this wrong in either direction causes problems. Destroy records too early and you risk non-compliance. Keep everything indefinitely and storage becomes unmanageable.

“Limited companies must keep accounting records that are adequate and available for inspection. The Companies Act 2006 specifies that these records must be preserved for at least three years for private companies, and at least six years for public companies, from the date they were made.” Companies Act 2006 s388

Companies House filing guidance also confirms that annual accounts must be delivered to Companies House each year, and the underlying records that support those accounts must be retained and accessible.

Here is a clear table of retention requirements by business type:

| Business type | Record type | Minimum retention period |

|---|---|---|

| Private limited company | Accounting records | 6 years from year end |

| Public limited company | Accounting records | 6 years from year end |

| Sole trader | Income and expense records | 5 years after 31 January filing deadline |

| VAT-registered business | VAT records | 6 years |

| Employer (any type) | Payroll and PAYE records | 3 years after tax year end |

| Self-employed | Business records | 5 years after tax year end |

Key archiving practices to align with these requirements:

- Label every archive box or digital folder with a clear “destroy after” date.

- Schedule an annual review of your archive. Delete or shred anything that has passed its retention deadline.

- For digital records, ensure your backup system retains files for the full retention period, not just a rolling window.

- Keep a register of when key documents were created and when they can be safely removed.

Do not overlook your annual confirmation statement obligations alongside your accounting records. These are separate filings with their own deadlines and retention considerations.

Common mistakes (and what actually works in practice)

Even the best plans falter if you fall into common traps. In our experience working with UK small and medium-sized businesses, the same mistakes appear repeatedly, and they are almost always avoidable.

The biggest culprit is inconsistent naming conventions. Business owners start with good intentions, then begin saving files as “Receipt” or “May Invoice,” making keyword searches useless six months later. The solution is simple: commit to a naming format on day one and document it so that anyone helping with your records uses the same approach.

Delayed updates are the second most common issue. Many business owners let transactions pile up for weeks before logging them, then spend a painful afternoon trying to match faded receipts to forgotten purchases. Weekly updates take fifteen minutes. Monthly catch-ups take hours. The maths is clear.

There is also a genuine debate about whether to organise records by date or by category. Both approaches can work effectively, and the right choice depends on how you prepare your VAT returns, management accounts, and tax reports, and how your transactions typically arrive. If your workflow is heavily invoice-driven with many clients, category-first organisation (Sales, Purchases, Payroll) often works better. If you process high volumes of daily transactions, date-first organisation may suit your natural rhythm more closely.

What genuinely helps, regardless of structure, is automation. Automated bank feeds eliminate manual transaction entry and dramatically reduce errors. Recurring invoice templates save time and ensure consistent formatting. Regular bank reconciliation, ideally monthly, catches problems before they compound. We have seen businesses avoid costly HMRC enquiries simply because their records were clean and their reconciliation was current.

The most important principle, and one that experienced accountants will tell you consistently, is to prioritise ease of retrieval above all else. A perfect filing structure that takes ten minutes to search is less useful than a good-enough structure where any document appears in thirty seconds. Understanding why maintaining business records matters is the first step. Building retrieval-friendly habits is what actually keeps businesses compliant under pressure.

Get expert help for flawless business record organisation

Managing record keeping alongside everything else that comes with running a business is genuinely demanding. Most business owners know they should be more organised but simply do not have the time or the expertise to build and maintain a robust system consistently.

At Concorde Company Solutions, we work with small and medium-sized businesses across the UK to take the weight of financial administration off your shoulders. From bookkeeping and software setup to full statutory accounts and payroll support for SME compliance, we help you stay on the right side of HMRC without spending your evenings buried in receipts. Our approach is practical, transparent, and tailored to your business. If you want to stop worrying about penalties and start focusing on growth, get in touch with our team in Garforth, Leeds today.

Frequently asked questions

What happens if I lose important business records?

You may face HMRC penalties, rejected tax claims, or failed audits if you cannot produce required records on request. Lenders and investors may also decline applications without adequate financial documentation.

Which software is compliant with Making Tax Digital in 2026?

You must use HMRC-recognised software to digitally record income and expenses if your turnover is above the threshold. Compatible MTD software must also send quarterly updates directly to HMRC.

Do sole traders and companies have the same record retention rules?

No. Limited companies must retain accounting records for at least six years under the Companies Act 2006, while sole traders generally need to keep records for five years after the self-assessment deadline.

How often should business records be reconciled?

Monthly bank reconciliation is strongly recommended. Regular reconciliation against bank statements helps you catch missing documents, errors, or unexplained transactions before they become a problem at year-end or during a tax enquiry.

No responses yet