TL;DR:

- Most UK businesses operate as sole traders or partnerships, not limited companies.

- Unincorporated businesses lack legal separation, so owners face unlimited personal liability.

- Proper financial management and early professional advice are crucial for business success.

There is a persistent myth in UK business culture that running a “proper” company means setting up a limited company. In reality, 4.4 million self-employed taxpayers operate as sole traders, making unincorporated structures the most common business model in the country. Yet despite being so widespread, these structures are frequently misunderstood. Owners often underestimate their personal risk, miss VAT deadlines, or set up poor financial systems from the start. This guide cuts through the confusion and gives you clear, practical guidance on how these businesses work, what the rules are, and how to run yours with confidence.

Table of Contents

- What is an unincorporated business?

- Main structures: Sole traders and partnerships

- Taxation and compliance: What you must know

- Financial management for unincorporated businesses

- A clear-eyed view: The realities of running an unincorporated business

- Expert support for your unincorporated business journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| No legal separation | Unincorporated businesses do not have a separate legal identity from their owners. |

| Unlimited personal liability | Sole traders and partners are personally responsible for all business debts and obligations. |

| Simple tax reporting | Profits are taxed as personal income, using Self Assessment and applicable National Insurance. |

| VAT threshold matters | Register for VAT if your annual turnover exceeds £90,000 to stay compliant. |

| Separate finances recommended | Even though not a legal requirement, use a separate business bank account for clarity and compliance. |

What is an unincorporated business?

Now that we have addressed how common unincorporated businesses are, let us clarify exactly what they are.

The term sounds technical, but the concept is straightforward. An unincorporated business is a structure without a separate legal personality from its owner or owners. In plain terms, you and your business are considered one and the same in the eyes of the law. There is no legal wall between your personal finances and your business finances.

This is the defining feature that sets unincorporated businesses apart from incorporated ones, such as limited companies. A limited company is a separate legal entity. It can own property, enter contracts, and take on debts in its own name. An unincorporated business cannot. Every contract, debt, and obligation belongs to you personally.

The two main forms of unincorporated business in the UK are:

- Sole trader: A single individual who owns and runs the business entirely on their own.

- Partnership: Two or more individuals who share ownership, responsibilities, and profits under a formal or informal agreement.

There are also limited liability partnerships (LLPs), which are a hybrid structure and technically incorporated, so they fall outside the scope of this guide. The focus here is on the two truly unincorporated models.

Why do so many people choose these structures? Because they are simple to set up, cheap to run, and give you complete control. There is no Companies House registration for sole traders, no complex formation documents, and no annual confirmation statements to file. You register with HMRC, start trading, and you are in business.

These structures suit start-ups, freelancers, tradespeople, consultants, and anyone testing an idea before committing to a more formal structure. The simplicity is real. But so is the responsibility that comes with it.

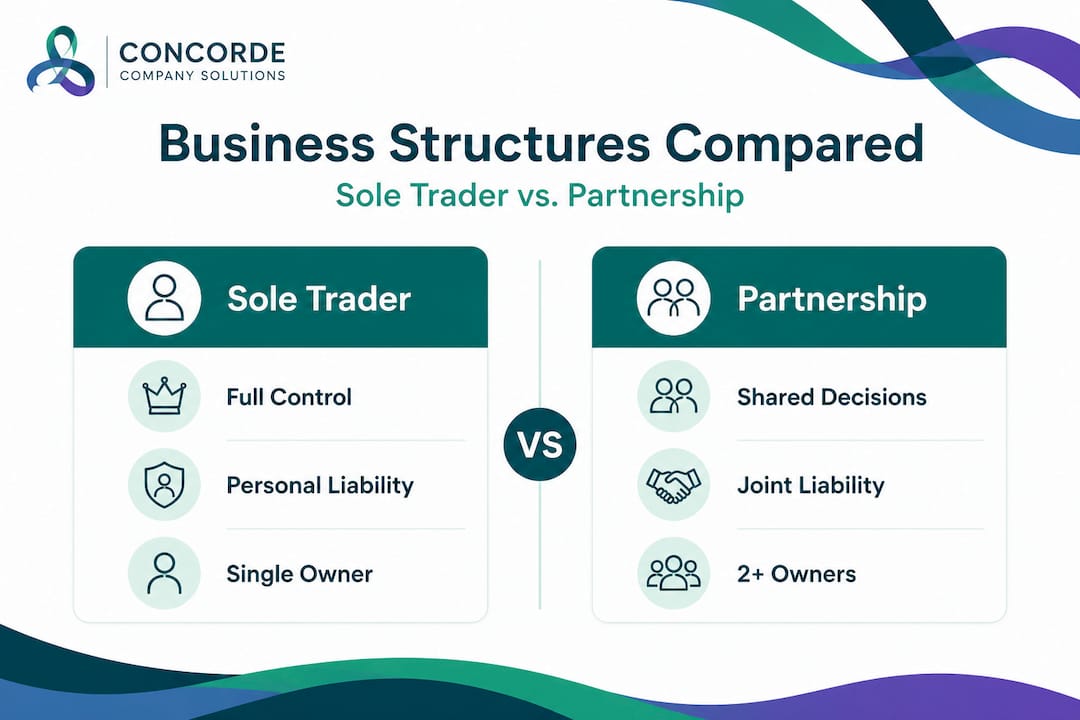

Main structures: Sole traders and partnerships

With core definitions covered, let us break down the main unincorporated options UK business owners choose.

Sole traders

A sole trader is the simplest business structure available. You own everything, control everything, and are responsible for everything. Sole traders have no legal separation from their business, which means unlimited liability. If your business runs up £50,000 in debts and cannot pay them, your creditors can come after your personal savings, your car, or even your home.

This is not a remote possibility. It is the legal reality. Many new business owners overlook this risk because they do not anticipate failing, or they assume their business will never carry significant debt. But debt can accumulate through unpaid invoices, equipment finance, or even a legal dispute.

Working with accountants for sole traders who understand this structure can help you manage risks intelligently, keep records tight, and avoid preventable problems.

Partnerships

A partnership involves two or more people running a business together. Profits, losses, and responsibilities are shared. However, unless you form a limited liability partnership, both partners carry unlimited personal liability. Crucially, in a general partnership, each partner can be held liable for the actions of the other partners. If your business partner takes on a debt in the business name without your knowledge, you could be equally responsible for repaying it.

This makes trust and clear written agreements essential in any partnership. A well-drafted partnership agreement should cover profit sharing, decision making, what happens if one partner wants to leave, and how disputes are resolved.

Comparing the two structures

| Feature | Sole trader | General partnership |

|---|---|---|

| Number of owners | One | Two or more |

| Legal separation from owner | None | None |

| Personal liability | Unlimited | Unlimited (joint and several) |

| Setup complexity | Very simple | Simple, but agreement advised |

| Tax filing | Self Assessment | Each partner files separately |

| Control | Full | Shared |

| Profit distribution | Kept by owner | Split per agreement |

The steps to get started as a sole trader are worth knowing clearly:

- Register with HMRC as self-employed as soon as possible after starting to trade.

- Set up a system for recording income and expenses from day one.

- Open a business bank account to separate your money flows.

- Understand your Self Assessment obligations and filing deadlines.

- Monitor your annual turnover and watch for the VAT threshold.

Pro Tip: Even if you are in a partnership, each partner still files their own Self Assessment tax return. The partnership itself also files a partnership return, but it does not pay tax directly. Each partner pays tax on their own share of the profits.

Taxation and compliance: What you must know

Once the structure is chosen, understanding tax and compliance responsibilities is vital.

Taxation for unincorporated businesses is personal rather than corporate. Profits are taxed as personal income via Income Tax and National Insurance contributions through the Self Assessment system. You report your business income and expenses once a year, and HMRC calculates what you owe.

Here is how the key tax obligations typically break down:

| Tax / Contribution | Applies when | Rate (2025/26) |

|---|---|---|

| Income Tax (basic rate) | Profits above personal allowance (£12,570) | 20% |

| Income Tax (higher rate) | Profits above £50,270 | 40% |

| Class 2 National Insurance | Self-employed with profits above £12,570 | £3.45 per week (if applicable) |

| Class 4 National Insurance | Profits between £12,570 and £50,270 | 9% |

| Class 4 (higher) | Profits above £50,270 | 2% |

| VAT | Turnover above £90,000 | 20% standard rate |

The VAT threshold is one of the most important numbers for any unincorporated business to track. You must register for VAT if your taxable turnover exceeds £90,000 in any rolling 12-month period. Miss this threshold and HMRC can back-date your liability, meaning you owe VAT on sales you already made without charging it to your customers.

Key compliance responsibilities include:

- Filing your Self Assessment tax return by 31 January each year (for the previous tax year ending 5 April).

- Paying any tax owed by the same 31 January deadline, plus a payment on account if required.

- Keeping accurate records of all income, expenses, invoices, and receipts for at least five years after the Self Assessment filing deadline.

- Monitoring turnover monthly to catch VAT registration triggers in good time.

Statistic to note: HMRC can charge automatic penalties for late Self Assessment returns starting at £100 even if no tax is owed. The cost of missing a deadline is never zero.

Many small unincorporated businesses use cash basis accounting, where you record income when money is actually received and expenses when they are actually paid. This is the default method for most sole traders and partners with turnover under £150,000. It simplifies recordkeeping considerably, but it does have limits. If you purchase significant capital assets or have complex financial arrangements, the cash basis can restrict the reliefs available to you.

For a detailed walkthrough, our sole trader tax return guide takes you step by step through the filing process so you know exactly what to expect.

Financial management for unincorporated businesses

Having outlined compliance, here is how to practically manage finances for smooth, stress-free operations.

Good financial management is what separates businesses that thrive from those that stumble. The rules around separating business and personal bank accounts, tracking expenses consistently, and monitoring turnover for VAT are not just best practice. They are what make compliance straightforward rather than stressful.

Here are the practical habits that make the biggest difference:

- Open a dedicated business bank account. Although it is not a legal requirement for sole traders, mixing personal and business money creates confusion during Self Assessment and makes it far harder to see how your business is truly performing.

- Record every transaction as it happens. Trying to reconstruct a year’s worth of invoices and receipts at the end of January is one of the most common causes of errors and unnecessary stress.

- Review your turnover figure monthly. A sudden upturn in business can push you past the VAT threshold faster than you expect. Set a reminder when you reach £75,000 so you have time to prepare.

- Track deductible expenses carefully. Business costs such as travel, equipment, professional subscriptions, home office use, and marketing can significantly reduce your taxable profit.

- Consider bookkeeping software. Tools like QuickBooks, Xero, or FreeAgent can automate a lot of the admin and produce a clear picture of your finances at any time.

One often-overlooked benefit is the deductibility of pre-trading expenses. HMRC allows you to claim eligible expenses incurred up to seven years before your business officially started trading, treating them as if they were paid on the first day of trading. This can include costs such as training, website development, equipment purchases, and professional fees paid during your planning phase.

For a broader view of the financial habits that make a difference, our guide on accounting tips for sole traders covers the practical detail. If you operate mainly on cash and want to understand how the accounting method works for you, our cash basis accounting guide explains the rules clearly.

Pro Tip: Even if your business is profitable, poor cash flow can still cause serious problems. Build a habit of looking forward, not just backward, in your financial planning. Our guide on sole trader cash flow planning offers a practical framework for forecasting and staying ahead.

A clear-eyed view: The realities of running an unincorporated business

Here is a perspective that does not get said often enough. Conventional wisdom tells you to keep things simple, and the message that sole trader status is the easiest route is not wrong. It genuinely is simpler. But “simple to set up” does not mean “simple to run well.”

The absence of a legal boundary between you and your business is not an abstract technicality. It is a live financial risk every single day you trade. If a client does not pay, if a contract goes wrong, or if you inadvertently incur a liability, there is nothing standing between that problem and your personal life. No corporate veil. No limited liability protection. Just you.

What we see time and again is that business owners who succeed with unincorporated structures do not succeed because they got lucky. They succeed because they built solid systems early. They tracked everything. They reviewed their numbers regularly. They knew their VAT threshold. They kept clean records and filed on time. These are not glamorous tasks, but they are what keeping your business on the right side of HMRC actually looks like.

There is also a myth that you only need an accountant when things get complicated. That is backwards thinking. The earlier you get practical sole trader accounting advice from someone who knows what they are talking about, the fewer expensive problems you create for yourself. An hour of professional input at the start of your business can save you days of stress and hundreds of pounds down the line.

The other thing worth saying clearly: unincorporated status is not a permanent decision. Many business owners start as sole traders and incorporate later when income grows, when they want to take on staff, or when the liability risk becomes more significant. Understanding what you are operating under right now helps you make better decisions about when and whether to change. Being informed is always the stronger position.

Expert support for your unincorporated business journey

Running an unincorporated business gives you freedom and simplicity, but the compliance obligations are real and the financial stakes are personal. Getting them right matters more than most people realise at the start.

At Concorde Company Solutions, based in Garforth, Leeds, we work with sole traders and small business owners across the UK to take the stress out of managing finances and staying compliant. Whether you need support with payroll solutions, bookkeeping, Self Assessment filing, or setting up accounting software that actually works for your business, we offer straightforward, transparent support without the jargon. We build long-term relationships with our clients because we know that consistent, reliable guidance is what makes a real difference. Get in touch to find out how we can help you run your business with clarity and confidence.

Frequently asked questions

What is the key difference between unincorporated and incorporated businesses?

Unincorporated businesses have no legal separation between the owner and the business, while incorporated businesses like limited companies have a distinct legal identity and separate liability.

Do I need to register for VAT as a sole trader?

You must register for VAT if your business turnover exceeds £90,000 within any rolling 12-month period, regardless of your business structure.

Am I personally liable for business debts as an unincorporated sole trader?

Yes. Sole traders have unlimited liability for all business debts, meaning personal assets can be used to settle outstanding obligations if the business cannot pay.

Can expenses before starting to trade be claimed for tax?

Yes. Pre-trading expenses up to 7 years prior to starting are deductible, treated as if incurred on the first day of trading, which can meaningfully reduce your initial tax bill.

No responses yet