TL;DR:

- Making Tax Digital for VAT is mandatory for all VAT-registered UK businesses since April 2022.

- Compliance requires digital records, HMRC-recognised software, and automated data transfer between systems.

- Most errors stem from improper workflows and staff training, not just technical software issues.

Many small business owners assume Making Tax Digital is something that only larger companies need to worry about. That assumption is costly. MTD for VAT is mandatory for every VAT-registered business in the UK, regardless of turnover or size. Whether you run a sole trader operation or manage a growing limited company, if you are VAT-registered, you are required to keep digital records and submit returns through compatible software. This guide cuts through the noise and gives you a clear picture of what compliance actually looks like, what the penalties are, and where businesses most commonly trip up.

Table of Contents

- What is Making Tax Digital for VAT?

- Core requirements and how compliance works

- Exemptions and special cases

- Penalties for non-compliance and common mistakes

- What most MTD for VAT guides miss

- Get support for Making Tax Digital for VAT

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| MTD mandatory for all | Every VAT-registered UK business must comply with Making Tax Digital unless exempted. |

| Digital records required | You must keep and submit VAT data using HMRC-recognised digital software and links. |

| Mistakes are costly | Non-compliance can lead to significant fines and penalties under HMRC’s new regime. |

| Exemptions are rare | Exemptions exist for very specific situations, and most businesses will not qualify. |

| Expert support helps | Professional help can save time, ensure compliance, and reduce the risk of costly mistakes. |

What is Making Tax Digital for VAT?

Making Tax Digital, often shortened to MTD, is a government-led initiative designed to modernise the UK tax system. At its core, MTD for VAT requires all VAT-registered businesses to keep digital records and submit VAT returns using HMRC-recognised software. The aim is to reduce the VAT gap, which is the difference between what HMRC expects to collect and what it actually receives, largely caused by preventable errors in manual record-keeping.

HMRC launched MTD because the numbers were stark. Manual processes, transcription errors, and lost paperwork were costing the Treasury billions each year. Businesses that move to digital systems tend to produce fewer VAT errors under MTD, which benefits both the business and the wider tax system.

Key MTD for VAT timeline:

| Date | What changed |

|---|---|

| April 2019 | MTD for VAT launched for businesses above the £85,000 VAT threshold |

| April 2022 | Mandatory for all VAT-registered businesses, regardless of turnover |

| 2026 onwards | HMRC continuing to expand MTD to income tax self assessment |

Since April 2022, there are no opt-outs unless your business qualifies for a formal exemption. This catches many smaller businesses off guard, particularly those who only recently crossed the VAT registration threshold or voluntarily registered for VAT.

Who must comply:

- All VAT-registered businesses in the UK

- Businesses that voluntarily registered for VAT

- Partnerships, sole traders, limited companies, and charities (unless exempt)

- Overseas businesses registered for UK VAT

The scope is broad and intentional. HMRC wants consistent digital data across the board, not just from larger operators.

Core requirements and how compliance works

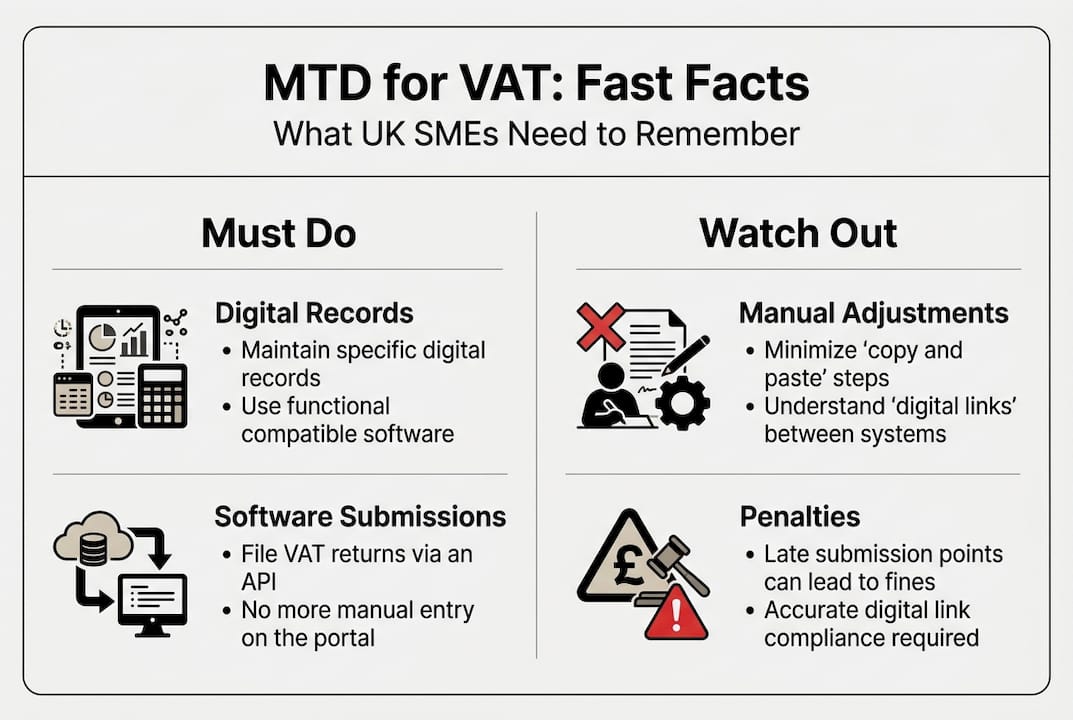

Understanding the rule exists is one thing. Knowing precisely what it demands of your day-to-day processes is another. Core MTD requirements include maintaining digital records, using HMRC-recognised software, and ensuring digital links exist between your records and your submission.

Let’s be specific about what “digital records” actually means. You must store the following digitally:

- The time and nature of each supply you make or receive

- The value of each transaction and the VAT charged

- VAT invoice details for each transaction

- A summary VAT account that feeds directly into your return

The critical point here is the concept of digital links. A digital link means data must move automatically between systems, whether that is from your accounting software to your submission tool, or from a spreadsheet to bridging software. What HMRC does not accept is someone typing figures from one system into another. That counts as breaking the digital link, even if both systems are technically digital.

Compliant versus non-compliant workflows:

| Workflow | Compliant? |

|---|---|

| Accounting software submitting directly to HMRC | Yes |

| Spreadsheet with bridging software and automatic data transfer | Yes |

| Spreadsheet manually re-typed into submission tool | No |

| Emailed PDF invoices manually entered into a spreadsheet | Depends on how data moves after entry |

For your digital tax submission process, the flow typically looks like this: record transactions digitally, ensure those records feed into your accounting software automatically, then use that software (or compatible bridging software) to submit your VAT return to HMRC.

Pro Tip: Manual adjustments, such as fuel scale charges or partial exemption calculations, are permitted, provided the final adjusted figure enters your digital system before submission. Many business owners wrongly believe any manual step invalidates their compliance.

Exemptions and special cases

MTD for VAT is mandatory, but HMRC does recognise that a narrow set of businesses may face genuine barriers to digital compliance. Understanding whether you qualify for an exemption matters, because applying incorrectly (or not applying when you should) both carry risks.

Recognised exemption categories include:

- Digital exclusion: This covers businesses where the owner or responsible person is elderly, has a disability, or lives in an area with no reliable internet access. HMRC interprets this narrowly.

- Insolvency: Businesses in certain insolvency proceedings may be exempt.

- Religious grounds: Members of certain religious communities whose beliefs prevent them from using computers may qualify.

- Existing exemptions: Businesses already exempt from online VAT filing may carry that exemption forward.

To apply, you contact HMRC either by phone via their VAT helpline or in writing, setting out your grounds clearly. HMRC will review each application individually. There is no automatic exemption. If HMRC rejects your application, you are expected to comply from the date of refusal, or potentially earlier.

“The vast majority of businesses will not qualify for an exemption. HMRC’s focus during compliance checks is on whether digital links are in place, not simply whether software is being used.” This is a distinction worth understanding before you assume a workaround is acceptable.

If you are unsure about your situation, particularly if you have unusual operating circumstances, seeking advice early is far more cost-effective than facing a compliance review later. Resources on finance help for small businesses can also help you think through your options before approaching HMRC directly.

Penalties for non-compliance and common mistakes

The consequences for getting MTD for VAT wrong are real and financially significant. HMRC overhauled the penalty regime in January 2023, moving to a points-based system that many see as fairer but which still catches businesses off guard.

How the penalty system works:

| Penalty type | How it is triggered | Cost |

|—|—|

| Late submission points | Each missed VAT return earns a point | Points accumulate to a £200 fine at threshold |

| Late payment penalty | Payment more than 15 days late | Tiered percentage of unpaid VAT |

| Inaccuracy penalty | Errors in returns | Up to 100% of underpaid VAT |

| Non-compliance | Failing to use compliant software | Up to £400 per return |

Penalty thresholds under MTD vary depending on your submission frequency. Quarterly filers hit the £200 fine threshold at four points. Annual filers reach it at two. Points reset after a period of clean compliance, but the clock only starts once you have cleared the threshold, not before.

The scale of the problem is significant. 24% of VAT-registered businesses received at least one late submission point since the 2023 reforms. That figure suggests the system is catching a substantial number of businesses.

Steps to avoid the most common compliance mistakes:

- Set calendar reminders for every VAT return deadline, not just payment deadlines

- Confirm your software is on HMRC’s approved list before your next submission

- Check that digital links exist between every stage of your record-keeping

- Reconcile your VAT account monthly rather than scrambling at quarter end

- Keep all VAT invoices stored digitally and accessible within your accounting system

Pro Tip: The penalty reforms were designed to encourage behaviour change, but HMRC compliance data shows that late submissions remain stubbornly common. Setting up automated reminders in your accounting software takes minutes and removes the single biggest cause of points accumulating.

What most MTD for VAT guides miss

Most articles on MTD for VAT focus on the rules themselves. What they rarely address is the gap between understanding the rules and actually operating compliantly day to day.

Software does not solve everything. Many business owners install MTD-compatible software, tick a mental compliance box, and carry on with workflows that are not actually compliant. For instance, copy-paste is not a digital link, even though HMRC took a pragmatic approach in the first year of rollout. That leniency is not guaranteed going forward.

The deeper issue is that most VAT errors are not technical. They are basic: wrong VAT codes applied, invoices filed in the wrong period, or partial exemption calculations done incorrectly by hand. Digital systems reduce transcription errors, but they cannot fix a VAT code that was wrong from the start.

Staff training is where many SMEs underinvest. If the person entering transactions does not understand the difference between standard-rated and zero-rated supplies, no software will catch that mistake automatically. Training is not an optional extra; it is a core part of a compliant process.

We have seen businesses spend weeks setting up sophisticated software integrations while ignoring the fact that their bookkeeper was still emailing figures across manually. The setup is only as strong as the habits around it. If you want to build something that actually holds up to scrutiny, professional tax support for SMEs is often the most efficient route, not because you cannot do it alone, but because an experienced adviser spots the gaps that software never will.

Get support for Making Tax Digital for VAT

For many business owners, the fastest route to confident compliance is having an expert in your corner.

At Concorde Company Solutions, we work with small and medium-sized businesses across the UK to take the confusion out of MTD for VAT. From software setup and digital record reviews to ongoing bookkeeping and VAT return submissions, we make sure your processes hold up to HMRC scrutiny. We do not do generic advice. We look at your specific workflows, identify the weak points, and put practical solutions in place. If you want straightforward Making Tax Digital support from people who understand both the rules and the realities of running a small business, get in touch with our team in Garforth, Leeds today.

Frequently asked questions

Does every VAT-registered business in the UK have to follow Making Tax Digital now?

Yes, all VAT-registered businesses must comply with MTD for VAT since April 2022, unless formally exempted by HMRC following a successful application.

What software can I use for MTD for VAT submissions?

You need HMRC-recognised MTD-compatible software for both record-keeping and submission; spreadsheets are only permissible if properly linked via bridging software with no manual data transfer.

What kinds of records must I keep digitally for MTD for VAT?

Digital records must include details of supplies made and received, VAT invoice information, and a summary VAT account that links directly to your return.

Are there penalties if I submit my VAT return late under MTD?

Yes, HMRC operates a points-based penalty system where late submissions earn points that convert to a £200 fine at the relevant threshold, with additional charges for late payment.

How do I apply for an exemption from MTD for VAT?

Contact HMRC by phone or in writing, explaining your grounds clearly, whether that is age, disability, religious belief, remoteness, or insolvency, and wait for HMRC’s formal decision before assuming you are exempt.

No responses yet