Many UK business owners assume dividends are a simple, tax-free way to extract profits from their company. This belief often leads to unexpected tax bills and compliance issues. Dividend tax applies after your company pays corporation tax, affecting your personal income as a shareholder. Understanding how dividend tax works, the rates you’ll face, and the legal requirements for declaring dividends is essential for managing both your corporate finances and personal tax position effectively. This guide explains dividend tax basics, current rates, allowances, declaration rules, and the serious risks of getting it wrong.

Table of Contents

- Key takeaways

- What is dividend tax and how does it work in the UK?

- Dividend tax rates, allowances and thresholds for UK business owners

- How dividends are declared, reported and taxed in practice

- Risks and legal considerations of dividend payments for UK companies

- How Concorde Company Solutions supports your payroll and dividend tax needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Dividend tax after corporation tax | Dividend tax is charged after the company pays corporation tax on profits, affecting your personal tax as a shareholder. |

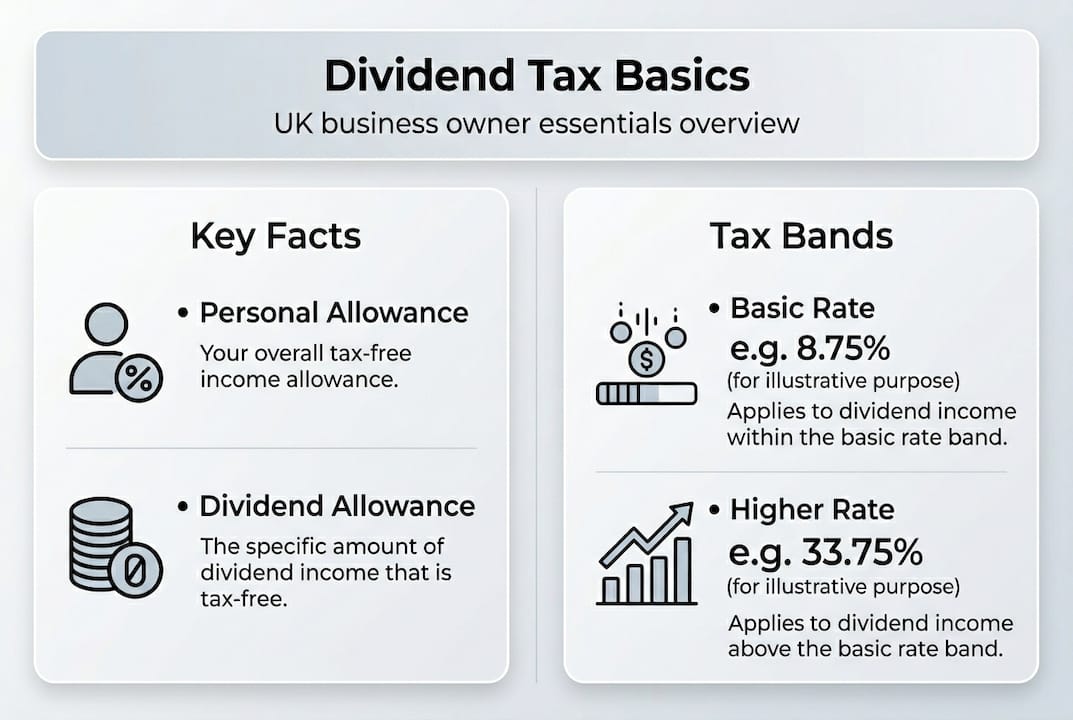

| Tax free allowance and bands | There is a £500 tax free dividend allowance and your personal allowance of £12,570 applies before calculating dividend tax. |

| Declaration and Self Assessment | Dividends must be declared properly and reported via Self Assessment, with penalties for non compliance. |

| 2026 rate changes | From 2026 basic and higher rate dividend tax rise by two percentage points, while the dividend allowance stays at £500. |

What is dividend tax and how does it work in the UK?

Dividend tax is a personal income tax on dividend payments received by shareholders from UK companies, charged at special rates after corporation tax has been paid at company level. This creates a two-tier taxation system: your company pays corporation tax on profits first, then you pay dividend tax on distributions from those after-tax profits.

Dividends represent your share of company profits distributed to shareholders. Unlike salary payments, dividends are paid gross with no tax withheld at source. You receive the full amount, but you’re responsible for reporting and paying any dividend tax owed through your Self Assessment tax return.

The structure differs significantly from employment income:

- No National Insurance contributions apply to dividend income

- Tax rates are lower than standard income tax rates

- Personal allowance applies before dividend tax calculations

- No PAYE deductions occur at payment

This makes dividends attractive for business owners extracting profits, but you must understand your obligations. Every pound of dividend income above your allowance faces taxation based on your total income band. Failing to report dividends or miscalculating your liability creates problems with HMRC that can result in penalties and interest charges on unpaid amounts.

Dividend tax rates, allowances and thresholds for UK business owners

For the 2025/26 tax year, you benefit from a £500 tax-free dividend allowance at 0% rate, with your personal allowance of £12,570 applying first to other income. Once you exceed these thresholds, dividend tax rates depend on which income band your total taxable income falls into.

| Income band | Total taxable income | Dividend tax rate 2025/26 | Rate from April 2026 |

|---|---|---|---|

| Basic rate | £12,571 to £50,270 | 8.75% | 10.75% |

| Higher rate | £50,271 to £125,140 | 33.75% | 35.75% |

| Additional rate | Over £125,140 | 39.35% | 39.35% |

The 2026 rate changes increase basic rate dividend tax by 2 percentage points and higher rate by 2 points, whilst additional rate remains unchanged. Your dividend allowance stays at £500.

Calculating your liability requires understanding how income stacks:

- Personal allowance covers the first £12,570 of all income

- Employment income, rental income, and other sources fill bands first

- Dividend income sits on top of other income

- The band where your dividends fall determines the rate

Suppose you earn £40,000 salary and receive £15,000 dividends. Your salary uses £27,430 of basic rate band (£40,000 minus £12,570 personal allowance). The remaining basic rate space is £22,840. After your £500 dividend allowance, £14,500 of dividends are taxable. The first £22,840 falls in basic rate at 8.75%, but you only have £22,840 of space and £14,500 of taxable dividends, so all dividends stay in basic rate.

Pro Tip: Track your total income throughout the year to anticipate which band your dividends will fall into. Strategic timing of dividend payments can sometimes keep you in a lower band, reducing your overall tax liability. Consider consulting tax trends for 2025 to plan effectively.

How dividends are declared, reported and taxed in practice

Dividends must originate from distributable company profits verified in your accounts. The process follows strict legal requirements to protect both the company and shareholders from invalid payments.

Declaration and payment mechanics work as follows:

- Directors verify distributable profits exist in company accounts

- Board meeting declares dividend proportional to shareholdings

- Dividend vouchers issued to each shareholder

- Payment made gross without tax deduction

- Shareholders report dividends on Self Assessment returns

- Tax payment due by 31 January following tax year end

Dividends are paid gross with no tax withheld, meaning you receive the full amount and must calculate and pay any tax owed through Self Assessment. This differs from salary where PAYE deducts tax before you receive payment.

You must file a Self Assessment tax return if your dividend income exceeds £10,000 in a tax year, regardless of whether tax is owed. Even if your dividends fall within your allowance, crossing this threshold triggers the reporting requirement. Missing this obligation results in penalties from HMRC.

Timing matters significantly. Dividends declared in one tax year but paid in the next are taxed in the year of payment, not declaration. This creates planning opportunities but also potential traps if you’re not tracking payment dates carefully.

Pro Tip: Maintain detailed records of all dividend declarations, board minutes, and payment dates. These documents prove your dividends were legal and properly authorised if HMRC queries your tax return. Understanding why filing tax returns matters helps you stay compliant.

Risks and legal considerations of dividend payments for UK companies

Illegal dividends create serious financial and legal consequences for both companies and shareholders. Understanding these risks protects you from costly mistakes that can threaten your business and personal finances.

Unlawful dividends occur when payments are made without sufficient distributable profits. These dividends are void by law. Recipients who knew or should have known must repay the amounts. Those who received dividends in good faith face treatment as loans, attracting a 33.75% tax charge if unpaid within nine months. Directors face personal liability if the company becomes insolvent.

The most common cause of illegal dividends is paying based on cash availability rather than accounting profits. Your bank balance doesn’t determine distributable reserves. Only properly prepared accounts showing retained profits after all liabilities can support dividend declarations.

Key risks include:

- Personal liability for directors in insolvency proceedings

- Repayment obligations for shareholders who received illegal dividends

- Section 455 tax charges treating dividends as loans

- HMRC penalties for incorrect tax reporting

- Potential disqualification for directors in serious cases

Many illegal dividends arise from paying based on cash rather than profits. Verifying reserves through accounts and board minutes is critical to avoid penalties and insolvency claims.

Protecting yourself requires proper procedures. Always prepare or review accounts before declaring dividends. Hold board meetings with proper minutes recording the decision and confirming distributable profits exist. Issue dividend vouchers documenting each payment. Never declare dividends exceeding verified retained profits, even if the company holds substantial cash.

If you discover you’ve paid illegal dividends, act immediately. Consult your accountant to determine the extent of the problem. Consider whether shareholders should repay amounts or whether other solutions exist. Addressing issues proactively minimises penalties and legal exposure. Understanding corporate tax planning helps prevent these situations.

How Concorde Company Solutions supports your payroll and dividend tax needs

Managing dividend tax alongside employment income creates complexity that many business owners find overwhelming. Getting calculations wrong, missing deadlines, or failing to maintain proper documentation exposes you to penalties and unexpected tax bills.

Concorde Company Solutions provides professional payroll services that handle both salary and dividend taxation accurately. We ensure your Self Assessment reporting captures all dividend income correctly and calculate your exact liability based on your total income position. Our team tracks changing rates and thresholds, including the April 2026 increases, so you’re always compliant with current regulations.

We help you plan dividend payments strategically to optimise your tax position whilst ensuring every declaration is legal and properly documented. Our dedicated support means you can focus on running your business whilst we handle the technical compliance requirements. Whether you need ongoing payroll management or specific dividend tax guidance, Concorde Company Solutions delivers the expertise you need to navigate these obligations confidently.

Frequently asked questions

What is dividend tax?

Dividend tax is a personal income tax charged on dividend payments you receive as a shareholder from UK companies. It applies after your company has paid corporation tax on profits. The tax uses special rates lower than standard income tax but higher than capital gains tax. You pay dividend tax through Self Assessment based on your total income band.

How is dividend tax calculated for shareholders?

Calculation starts with your personal allowance of £12,570 covering all income types. Other income fills your tax bands first, then dividend income sits on top. You get a £500 dividend allowance at 0% rate. Remaining dividends are taxed at 8.75%, 33.75%, or 39.35% depending which band they fall into. From April 2026, basic and higher rates increase by 2 percentage points each.

What happens if a company pays an illegal dividend?

Illegal dividends must be repaid to the company. Shareholders who knew or should have known the dividend was unlawful face immediate repayment obligations. Those who received payments in good faith have them treated as loans, attracting a 33.75% tax charge if unpaid within nine months. Directors may face personal liability if the company becomes insolvent. Proper verification of distributable profits before declaration prevents these serious consequences.

Do I need to file a Self Assessment if I receive dividends?

You must file Self Assessment if your dividend income exceeds £10,000 in a tax year, regardless of whether any tax is owed. Below this threshold, filing may not be required unless you have other reasons to submit a return. Even if your dividends fall within your £500 allowance, crossing the £10,000 threshold triggers the reporting obligation. Missing this requirement results in penalties from HMRC.

How will dividend tax rates change from April 2026?

From 6 April 2026, basic rate dividend tax rises from 8.75% to 10.75%, and higher rate increases from 33.75% to 35.75%. Additional rate remains unchanged at 39.35%. The dividend allowance stays at £500. These changes mean business owners in basic and higher rate bands will pay more tax on the same dividend income. Planning for these increases now helps you adjust your profit extraction strategy and avoid surprises.

No responses yet