Many UK business owners treat statutory deadlines as flexible suggestions rather than legal obligations. Missing these dates triggers penalties starting at £150, escalating rapidly to £1,500 or more for prolonged delays. Worse, persistent non-compliance risks company strike-off. This guide clarifies what statutory deadlines mean, identifies critical dates you must track, explains penalty structures, and provides practical strategies to maintain compliance and protect your business from avoidable financial consequences.

Table of Contents

- Understanding Statutory Deadlines: Definition And Legal Context

- Common Statutory Deadlines Relevant To UK Business Owners

- Consequences And Penalties Of Missed Statutory Deadlines

- Common Misconceptions About Statutory Deadlines And Compliance

- Comparison Of Statutory Deadlines For Private Vs Public Companies

- Modifying Statutory Deadlines: Can You Change Your Accounting Reference Date?

- Implementing Compliance Strategies To Meet Statutory Deadlines

- How Concorde Company Solutions Supports Your Compliance Needs

- Frequently Asked Questions About Statutory Deadlines

Key Takeaways

| Point | Details |

|---|---|

| Legal Foundation | Statutory deadlines are fixed by Companies Act 2006 and determine when accounts and tax returns must be filed. |

| Company Type Matters | Private limited companies get 9 months to file accounts while public companies have only 6 months from year end. |

| Penalties Escalate Fast | Late filing penalties start at £150 and increase to £1,500 based on delay length, with tax penalties adding further costs. |

| ARD Changes Allowed | You can modify your accounting reference date by filing form AA01, but this affects future deadlines and extension eligibility. |

| Proactive Tracking Works | Businesses implementing deadline tracking systems reduce late filing penalties by up to 50%. |

Understanding Statutory Deadlines: Definition and Legal Context

Statutory deadlines are legally mandated dates by which UK companies must file specific documents with Companies House and HMRC. These obligations stem from the Companies Act 2006, which establishes the framework for corporate compliance. Understanding this legal foundation helps you recognize why these deadlines carry serious consequences rather than mere administrative inconvenience.

The accounting reference date (ARD) sets the statutory deadline for preparing annual accounts and determines when you must file with Companies House. Your ARD is typically the last day of the month in which your company was incorporated, though you can change it. This date anchors your entire compliance calendar, triggering a cascade of related deadlines throughout your financial year.

For limited company compliance, key statutory deadlines include:

- Annual accounts filing with Companies House

- Corporation Tax returns submission to HMRC

- Corporation Tax payment obligations

- Confirmation statement updates

- VAT returns if registered

Each deadline operates independently but relates to your ARD. Private limited companies typically have 9 months from their ARD to file accounts, while Corporation Tax returns are due 12 months after the accounting period ends. Payment deadlines differ again, creating a complex compliance landscape that demands careful tracking.

Your company’s legal structure and operational choices affect which deadlines apply. A dormant company faces different requirements than an active trading business. Understanding your specific obligations based on your circumstances prevents confusion and ensures you meet every relevant deadline without gaps that could trigger penalties.

Common Statutory Deadlines Relevant to UK Business Owners

UK business owners must track multiple overlapping deadlines throughout the year. Missing any single deadline can trigger penalties, so comprehensive awareness of each obligation is essential for maintaining good standing with regulatory authorities.

Corporation Tax Return deadlines fall 12 months after the end of the accounting period, while Corporation Tax payment is due 9 months and 1 day after the accounting period ends. This creates a timing mismatch where you must pay tax before filing the full return, requiring accurate advance calculations to avoid underpayment penalties.

For tax deadlines for UK businesses, here are critical dates:

- Annual accounts to Companies House: 9 months after ARD for private companies, 6 months for public companies

- Corporation Tax payment: 9 months and 1 day after accounting period ends

- Corporation Tax return: 12 months after accounting period ends

- Confirmation statement: At least once every 12 months from the last filing

- PAYE and National Insurance: Monthly by 22nd if paying electronically, 19th if paying by cheque

VAT registered businesses face additional quarterly deadlines. Your VAT return and payment are typically due one month and seven days after the end of each VAT period. This adds four extra compliance dates annually, each carrying its own penalty structure for late submission or payment.

The annual returns filing importance cannot be overstated. Your confirmation statement updates Companies House on director details, shareholder information, and company structure changes. While less complex than accounts, missing this deadline still triggers penalties and can create administrative complications if information becomes outdated.

Payroll obligations create the most frequent deadlines. If you employ staff, you must submit RTI (Real Time Information) to HMRC on or before each payday and pay PAYE and National Insurance by the 22nd of each month. These monthly commitments require consistent processes, as HMRC deadlines for small businesses leave little room for delays.

Consequences and Penalties of Missed Statutory Deadlines

Missing statutory filing deadlines with Companies House results in penalties starting at £150, increasing with the length of delay. Understanding the penalty structure helps you prioritize compliance and appreciate the financial impact of procrastination.

The penalty escalation works as follows:

- Up to 1 month late: £150

- 1 to 3 months late: £375

- 3 to 6 months late: £750

- Over 6 months late: £1,500

These penalties apply to each set of accounts filed late. If you run multiple companies and miss deadlines across several entities, penalties multiply quickly. A business owner with three companies missing deadlines by four months would face £2,250 in penalties from Companies House alone.

Corporation Tax penalties follow a different structure but compound the financial damage. HMRC charges penalties based on how late you file your return and whether tax remains unpaid. An immediate penalty of £100 applies if your return is one day late, increasing to £200 if three months late. After six months, HMRC adds penalties calculated as a percentage of unpaid tax, which can reach 20% for persistent non-compliance.

Pro Tip: Set reminders for 30 days before each deadline rather than on the deadline itself. This buffer gives you time to gather information, resolve unexpected issues, and file comfortably ahead of the due date without last minute stress.

Beyond financial penalties, persistent non-compliance puts your company at risk of strike-off. Companies House can initiate dissolution proceedings if you fail to file required documents. Once struck off, your company ceases to exist legally, you lose limited liability protection, and assets can vest in the Crown. Restoring a struck-off company involves legal costs and administrative burden far exceeding any penalty you might have paid for timely filing.

Reputation damage compounds financial costs. Late filing appears on the public register, visible to potential clients, suppliers, and lenders. This creates perception problems about your business management capabilities and financial stability. How to file company accounts on time protects both your finances and your professional reputation.

Common Misconceptions About Statutory Deadlines and Compliance

Many business owners mistakenly believe missing a statutory deadline only causes minor inconvenience rather than financial penalties and legal risks. This dangerous assumption leads to casual attitudes about compliance that ultimately cost businesses thousands in avoidable penalties.

One prevalent myth suggests all companies share identical deadlines. In reality, your specific dates depend on your accounting reference date, company type, and registration choices. A company incorporated in January faces completely different deadlines than one incorporated in July. Assuming your deadlines match other businesses in your network creates dangerous gaps in your compliance calendar.

Another misconception treats deadline extensions as readily available safety nets. While you can change your accounting reference date under certain circumstances, this is not an extension for late filing. Extensions are rarely granted and require exceptional circumstances like serious illness or natural disasters. Planning to request an extension as a routine compliance strategy will fail, leaving you facing penalties you assumed you could avoid.

Some business owners believe dormant companies escape statutory obligations entirely. While dormant companies have reduced requirements, they still must file annual accounts and confirmation statements. The accounts may be simpler, but the deadlines remain legally binding. Assuming dormancy eliminates compliance entirely leads to unexpected penalties and potential strike-off proceedings.

Confusion between different regulatory bodies creates further problems. Business owners sometimes assume filing with Companies House satisfies HMRC requirements, or vice versa. These are separate obligations with distinct deadlines. Your accounts filing with Companies House does not substitute for your Corporation Tax return to HMRC, and each carries its own penalty regime.

The compliance checklist approach helps counter these misconceptions. Rather than relying on assumptions or partial information, maintain a comprehensive list of every deadline specific to your company. Cross-reference this list against official guidance from Companies House and HMRC to ensure accuracy.

Pro Tip: Create a master calendar at the start of each financial year listing every statutory deadline you face. Include Companies House filings, HMRC submissions, VAT returns if applicable, and payroll obligations. Review this monthly to ensure nothing slips through gaps in your attention.

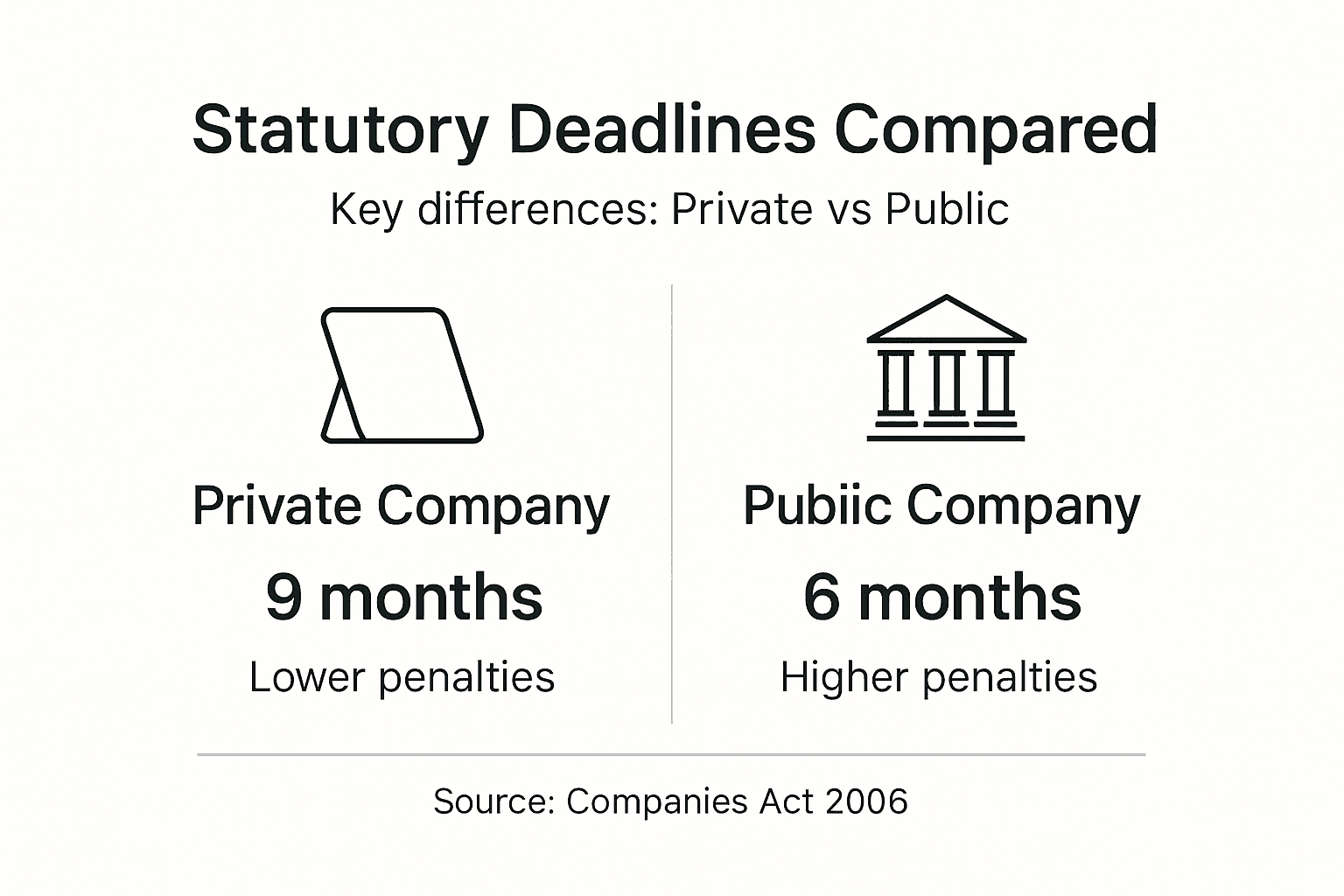

Comparison of Statutory Deadlines for Private vs Public Companies

Statutory deadlines vary significantly between private limited companies and public limited companies, with public companies facing tighter timeframes that reflect their greater regulatory scrutiny and public accountability.

| Aspect | Private Limited Company | Public Limited Company |

|---|---|---|

| Accounts Filing Deadline | 9 months after ARD | 6 months after ARD |

| Corporation Tax Return | 12 months after accounting period end | 12 months after accounting period end |

| Corporation Tax Payment | 9 months and 1 day after period end | 9 months and 1 day after period end (installments for large companies) |

| Late Filing Penalty (up to 1 month) | £150 | £750 |

| Late Filing Penalty (over 6 months) | £1,500 | £7,500 |

The three month difference in accounts filing deadlines creates significantly less preparation time for public companies. This tighter schedule demands more rigorous internal processes and often requires larger finance teams or more intensive accountant involvement to meet the compressed timeline.

Penalty structures amplify the difference. Public companies face penalties five times higher than private companies for equivalent delays. This reflects the greater public interest in timely financial reporting from entities that can sell shares to the general public. A public company filing accounts three months late pays £3,750 compared to £750 for a private company.

Corporation Tax obligations remain identical for payment timing but differ in payment method for large companies. Companies with taxable profits exceeding £1.5 million must pay Corporation Tax in quarterly installments starting before the accounting period even ends. This advance payment requirement demands sophisticated cash flow forecasting not required of smaller private companies.

Understanding these distinctions matters when considering company structure changes. Converting from private to public status (or vice versa) immediately shifts your compliance calendar and penalty exposure. Planning such transitions requires careful attention to how deadline changes will impact your administrative capacity and financial planning.

Modifying Statutory Deadlines: Can You Change Your Accounting Reference Date?

Statutory deadlines can sometimes be adjusted by changing the accounting reference date, but this must be done before the filing deadline and may affect penalty eligibility. Understanding the rules governing ARD changes helps you make strategic decisions about your compliance calendar.

You can change your accounting reference date by filing form AA01 with Companies House. This form allows you to shorten or extend your accounting period, effectively moving your future deadlines. Companies can shorten their accounting period as many times as needed, but can only extend once every five years unless specific conditions apply.

Key rules for ARD changes include:

- You must file AA01 before the current accounts deadline expires

- Shortening periods have no frequency restrictions

- Extending periods limited to once every five years

- Extensions cannot exceed 18 months total for any single period

- Special rules apply for newly incorporated companies

Strategic reasons for changing your ARD might include aligning financial years with peak business cycles, coordinating with parent company reporting periods, or spreading workload more evenly across your finance team’s calendar. Some businesses prefer year ends outside typical peak seasons like March or December to access accountant time more readily and reduce pressure on internal resources.

Pro Tip: Consider your industry’s seasonal patterns when setting your accounting reference date. Retail businesses might avoid January year ends that fall immediately after the crucial Christmas trading period, while agricultural businesses might align with harvest cycles.

Changing your ARD affects more than just accounts filing deadlines. Your Corporation Tax return and payment dates shift correspondingly. If you extend your accounting period, you create a longer period before the next filing deadline, but you also delay when you can offset losses or claim reliefs. This creates tax planning implications that require careful consideration beyond simple deadline management.

Critically, changing your ARD purely to avoid an imminent penalty will fail. Companies House requires you to file the current period’s accounts before accepting an ARD change. You cannot use this mechanism as a last minute escape from approaching deadlines. The compliance guide emphasizes planning ARD changes well in advance as strategic decisions rather than reactive deadline dodging.

Implementing Compliance Strategies to Meet Statutory Deadlines

Successful deadline management requires systematic approaches rather than relying on memory or last minute scrambling. Studies show that businesses implementing proper deadline tracking reduce late filing penalties by up to 50%, demonstrating the tangible value of proactive compliance systems.

Implement these practical strategies to strengthen your compliance:

- Create a comprehensive compliance calendar listing every statutory deadline for the full year ahead

- Set automated reminders for 30 days, 14 days, and 7 days before each critical deadline

- Establish monthly review meetings with your accountant to confirm upcoming obligations

- Maintain organized records throughout the year rather than scrambling to compile information at deadline time

- Build buffer time into your internal deadlines to accommodate unexpected complications

- Document your compliance processes so staff absences do not create knowledge gaps

Cloud accounting software transforms deadline management by automating much of the tracking burden. Modern platforms integrate with HMRC and Companies House systems, pulling your specific deadlines based on your company details. These tools send automatic alerts and often enable direct filing from within the software, reducing administrative friction that causes delays.

Collaborating closely with your accountant creates accountability and expertise access. Rather than viewing your accountant as someone you contact only at year end, establish regular check-ins throughout the year. This ongoing relationship ensures your accountant understands your business circumstances and can flag potential issues before they become deadline crises.

The compliance checklist approach provides structure for businesses without dedicated finance teams. A simple checklist covering all annual obligations, updated as each task completes, prevents items from falling through cracks. Review your checklist monthly to maintain awareness of upcoming requirements rather than being surprised by imminent deadlines.

Common pitfalls to avoid include relying solely on memory, assuming accountants will remind you of everything, waiting until the deadline week to gather information, and failing to account for bank holidays that might affect payment processing times. Each of these behaviors increases your risk of late filing despite good intentions.

Pro Tip: Treat your compliance deadlines like client commitments with the same priority and planning. If you would not miss a major client deadline, apply that same discipline to your statutory obligations.

Real world example: A Leeds-based consultancy reduced its penalty costs from £1,125 annually to zero by implementing a simple shared calendar with color-coded deadline alerts and quarterly accountant reviews. The modest time investment of 30 minutes per month eliminated years of recurring penalties and stress.

Understanding essential HMRC deadlines specific to your business structure ensures you capture all relevant obligations rather than focusing only on high profile deadlines like annual accounts while missing monthly payroll or quarterly VAT requirements.

How Concorde Company Solutions Supports Your Compliance Needs

Meeting statutory deadlines becomes significantly easier with expert support tailored to your specific business circumstances. Professional accounting services transform compliance from a stress-inducing burden into a managed process that protects your business from penalties while freeing your time for revenue-generating activities.

Bespoke accounting support provides personalized deadline tracking based on your company’s unique compliance calendar. Rather than generic reminders, you receive specific guidance on exactly what you must file, when it’s due, and what information you need to compile. This tailored approach eliminates confusion about which deadlines apply to your particular business structure and operational choices.

Payroll services for UK businesses handle the complex monthly obligations of PAYE and National Insurance contributions. Professional payroll management ensures accurate RTI submissions on each payday and timely payments to HMRC by the 22nd of each month. This removes the administrative burden and penalty risk of managing payroll compliance internally, particularly valuable for growing businesses adding employees.

Comprehensive accounting services for businesses cover the full spectrum of statutory obligations. From preparing annual accounts that meet Companies House requirements to filing Corporation Tax returns accurately with HMRC, expert accountants ensure every deadline is met with properly completed documentation. This professional approach protects you from both late filing penalties and the potential for errors that could trigger inquiries or investigations.

Frequently Asked Questions About Statutory Deadlines

What happens if I miss a Corporation Tax payment deadline?

HMRC charges interest on late Corporation Tax payments from the due date until you pay, currently around 7.5% annually. If your return is also late, additional penalties apply starting at £100 for returns up to three months late, increasing to £200 at six months, plus percentage-based penalties on unpaid tax after that point.

Can I get an extension to file my annual accounts?

Companies House rarely grants extensions except in exceptional circumstances like serious illness or natural disasters affecting your ability to prepare accounts. You cannot extend deadlines simply because you are busy or disorganized. The proper approach is changing your accounting reference date well before the current deadline, though this only affects future periods, not imminent filings.

How do I know my company’s accounting reference date?

Your accounting reference date appears on your incorporation certificate and on all correspondence from Companies House. You can also check your company’s public record on the Companies House website by searching your company name or registration number. This free service shows your ARD and all upcoming statutory deadlines.

Are statutory deadlines the same for all UK companies?

No, deadlines vary significantly based on company type, accounting reference date, and operational choices. Private companies get nine months to file accounts while public companies have only six months. Your specific ARD determines the exact calendar dates for your filings. VAT registration, payroll obligations, and other factors create additional deadlines specific to your circumstances.

What tools can help me track deadlines effectively?

Cloud accounting software like Xero, QuickBooks, or FreeAgent automatically tracks your statutory deadlines and sends alerts. Companies House and HMRC also offer free email reminder services. A simple shared calendar with your accountant, color coded by deadline type and urgency, provides effective tracking without expensive software for smaller businesses.

No responses yet