TL;DR:

- Financial reporting provides essential business insights beyond mere compliance, aiding decision-making and credibility.

- Threshold changes in 2025/2026 impact account standards and disclosure requirements for UK SMEs.

- Properly leveraging statutory accounts transforms them into strategic tools for cash flow, profitability, and growth management.

Financial reporting is not simply a box-ticking exercise for Companies House. For UK small and medium-sized businesses, it sits at the intersection of statutory obligation and genuine business intelligence. Many owners treat their annual accounts as a chore to be handed off and forgotten, yet the same documents that satisfy HMRC and Companies House can reveal cash flow patterns, profitability trends, and strategic opportunities. With significant threshold increases and amended standards taking effect in 2026, now is exactly the right moment to understand what financial reporting actually demands of you and what it can do for your business.

Table of Contents

- What is financial reporting and why is it essential?

- How UK SME financial reporting standards work

- What UK SME statutory accounts must include

- Navigating nuances, recent changes and practical management use

- Why effective financial reporting is a strategic asset, not just a compliance chore

- Get support for your next reporting cycle

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal reporting basics | UK SMEs must produce statutory accounts that present a true and fair financial view for compliance. |

| Choose the right standards | Select FRS 102 or FRS 105 based on your business size and stakeholder requirements. |

| Simplified filing | Small and micro-entities benefit from reduced reporting requirements and increased thresholds from 2026. |

| Beyond compliance | Effective reporting helps with managing cash flow, profitability and strategic business decisions. |

| Stay updated | Recent changes mean extra disclosures and clearer management benefits—review rules annually. |

What is financial reporting and why is it essential?

Financial reporting is the process of producing statutory accounts that give a true and fair view under the Companies Act 2006. In plain terms, it means presenting your business finances in a way that is accurate, complete, and structured according to recognised standards. It is not optional. Every UK limited company must prepare and file accounts, regardless of size or activity.

But the obligation goes beyond ticking a legal box. Your accounts are read by HMRC, lenders, potential investors, suppliers offering credit, and sometimes prospective buyers of your business. Each of those audiences is asking a simple question: can I trust this company? A well-prepared set of accounts answers that question before anyone has to ask it.

The statutory basis sits firmly within the UK regulation overview established by the Companies Act 2006, which sets out the obligations for all UK-registered companies. Alongside this, UK GAAP (Generally Accepted Accounting Practice) provides the technical framework your accountant uses to prepare the figures.

Here is why financial reporting matters beyond compliance:

- Statutory compliance: Avoids penalties, late filing surcharges, and potential director disqualification

- Business credibility: Demonstrates transparency to banks, lenders, and trade creditors

- Informed decision-making: Gives directors a structured view of financial performance

- Tax accuracy: Supports correct corporation tax calculations and reduces HMRC enquiry risk

- Stakeholder confidence: Reassures employees, partners, and investors about business stability

“Every company must keep adequate accounting records and prepare annual accounts that give a true and fair view of the company’s financial position.” — Companies Act 2006

Pro Tip: Review your company’s size classification every year. A business that grows beyond a threshold mid-year may need to upgrade its reporting regime the following period. Staying ahead of this avoids rushed compliance. An accounting compliance checklist can help you track these obligations systematically.

How UK SME financial reporting standards work

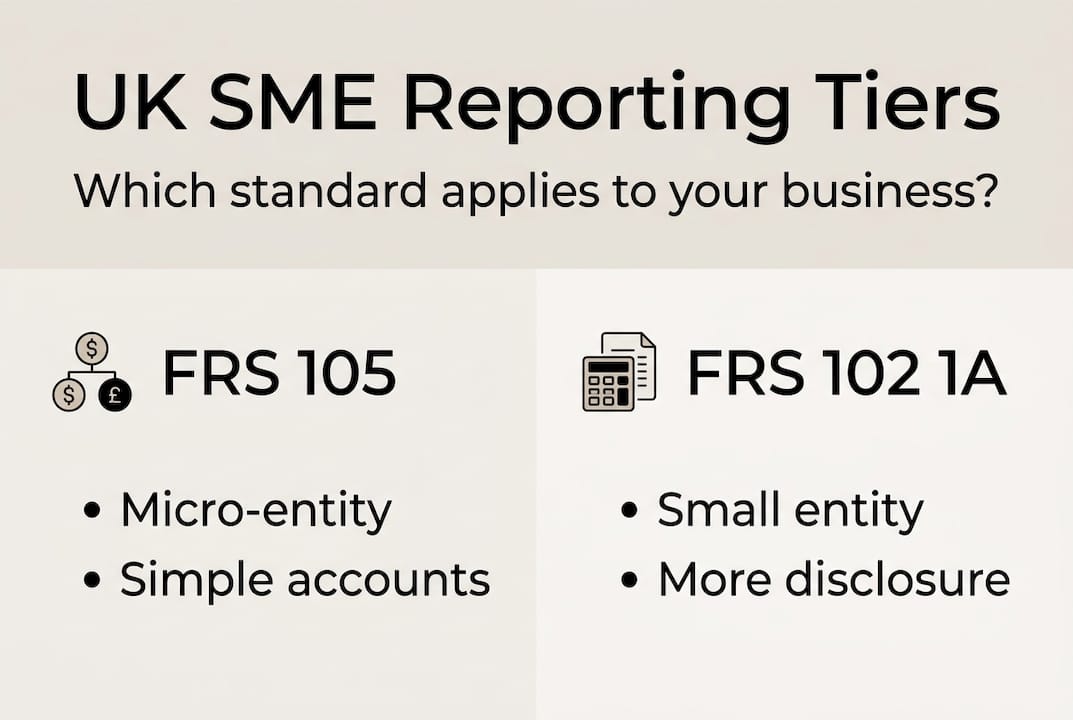

Not every business prepares the same accounts. The UK uses a tiered system, and the standard that applies to you depends on your company’s size. For UK SMEs, FRS 105 applies to micro-entities while FRS 102 Section 1A applies to small entities, each with different disclosure requirements and levels of detail.

The thresholds that determine your category changed significantly from April 2025. These are not minor adjustments. Many businesses that previously filed as small entities now qualify as micro-entities, which means simpler accounts and reduced disclosure obligations.

Here is a comparison to help you identify where your business sits:

| Feature | Micro-entity (FRS 105) | Small entity (FRS 102 Section 1A) |

|---|---|---|

| Turnover limit | Up to £1m | Up to £10.2m |

| Balance sheet limit | Up to £500k | Up to £5.1m |

| Employee limit | Up to 10 | Up to 50 |

| Profit and loss required | No (abridged balance sheet only) | Yes (can be omitted from public filing) |

| Notes to accounts | Minimal | More detailed |

| OCI statement | Not required | Required from 2026 |

To choose the right reporting regime, you must meet at least two of the three criteria for your chosen category. Meeting only one is not sufficient. This is a detail that catches some businesses out when they assume they qualify for the simpler micro-entity route.

FRS 105 is the simpler standard. It strips back disclosures to a minimum and is designed for the smallest businesses. FRS 102 Section 1A offers more flexibility but requires additional notes and, from 2026, an Other Comprehensive Income statement where relevant.

Reviewing a statutory accounts checklist before your year-end will help you confirm which standard applies. Understanding the tailored accounting advantages of each regime can also inform your choice.

Pro Tip: Even if FRS 105 is technically available to you, your bank or lender may request accounts prepared under FRS 102 Section 1A because they contain more financial detail. Always check what your key stakeholders expect before defaulting to the simplest option.

What UK SME statutory accounts must include

Once you know which reporting regime applies, you need to understand what your accounts must actually contain. The requirements differ between small and micro-entities, but the core documents are consistent.

Here are the essential components of statutory accounts:

- Balance sheet: A snapshot of assets, liabilities, and equity at the year-end date

- Profit and loss account: A record of income and expenditure over the financial year

- Notes to the accounts: Explanatory detail supporting the figures in the main statements

- Directors’ report: Required for small entities; covers principal activities and any significant events

- Cash flow statement: Required only for larger entities; small and micro-entities may omit this

- Strategic report: Optional for small entities; not required for micro-entities

Small and micro-entities benefit from meaningful simplifications. Small companies can omit the cash flow statement and strategic report, and until recently could also file abridged or filleted accounts. However, the option to file filleted accounts (where the profit and loss is excluded from the public filing) has been removed for financial years beginning on or after 1 January 2025. This is a significant change. Your full accounts are now filed publicly at Companies House.

Filing deadlines are fixed. Private limited companies must file within 9 months of year-end with Companies House. Missing this deadline triggers automatic penalties, starting at £150 for accounts up to one month late and rising sharply thereafter. Repeat late filing doubles the penalty.

Research suggests a notable proportion of UK SMEs file late each year, often because the accounts preparation process starts too late. Beginning your accounts filing process at least three months before the deadline gives you adequate time to gather records, review drafts, and respond to any queries. Reviewing examples of statutory accounts can also help you understand what a complete set looks like before you start.

Navigating nuances, recent changes and practical management use

The reporting landscape for UK SMEs shifted considerably in 2026. The FRC announced measures to support small business growth, including increased size thresholds and new transparency rules designed to reduce administrative burden while improving public accountability.

Here is a comparison of old and new thresholds:

| Category | Old turnover limit | New turnover limit (from Apr 2025) |

|---|---|---|

| Micro-entity | £632k | £1m |

| Small entity | £10.2m | £10.2m (unchanged) |

| Micro balance sheet | £316k | £500k |

| Small balance sheet | £5.1m | £5.1m (unchanged) |

Beyond thresholds, FRS 102 amendments introduce a five-step revenue recognition model and new lease accounting rules, bringing UK GAAP closer to international standards. These changes affect how you recognise income and report leased assets on your balance sheet. The expanded related party disclosures under amended FRS 102 also require small entities to disclose a broader range of transactions with connected parties, a change that catches some owner-managed businesses by surprise.

From 2026, OCI statements and broader disclosures are required for small entities applying FRS 102 Section 1A where a true and fair view demands it. This is not a bureaucratic addition. It reflects the reality that financial statements must fully represent the economic position of the business.

Smart SMEs are already using their statutory reporting cycle as a management tool. Here is how financial reporting supports real business decisions:

- Tracking monthly cash flow trends to anticipate shortfalls before they become crises

- Monitoring gross and net profit margins to identify underperforming products or services

- Comparing year-on-year figures to measure genuine growth rather than inflation-driven turnover increases

- Supporting loan applications with credible, professionally prepared financial data

- Informing pricing decisions based on actual cost analysis

Pro Tip: Pair your statutory accounts with monthly management accounts. Statutory accounts look backwards; management accounts look forwards. Together, they give you a complete picture. Reviewing your cash flow management steps alongside your annual figures is one of the most practical things you can do as a business owner.

Why effective financial reporting is a strategic asset, not just a compliance chore

Most SME owners we speak with view their annual accounts as something that happens to them rather than something that works for them. That mindset is understandable. Accounts arrive after the year is over, the figures describe decisions already made, and the filing deadline creates a pressure that feels purely administrative.

But here is the uncomfortable truth: businesses that treat reporting as a strategic exercise make better decisions. When you understand your numbers at a structural level, you stop reacting to cash flow surprises and start anticipating them. You stop guessing at profitability and start managing it deliberately.

It is worth noting that over 90% of UK audits are handled by firms outside the Big Four. That means the quality of financial reporting for most SMEs depends entirely on the relationship between the business owner and their accountant. A good accountant does not just file your accounts. They interpret them, flag anomalies, and connect the statutory picture to your actual business goals.

The 2026 changes, particularly the end of filleted accounts, are a nudge in the right direction. More transparency in public filings means more accountability, and accountability, when embraced rather than resisted, sharpens financial discipline.

Use your reporting cycle as a strategic checkpoint, not just a compliance deadline.

Get support for your next reporting cycle

Understanding your reporting obligations is one thing. Meeting them accurately and on time, while also extracting genuine management value, is another challenge entirely.

At Concorde Company Solutions, we work with UK SMEs to prepare statutory accounts, manage payroll, and keep your compliance on track throughout the year. Whether you need support with your next set of accounts or want to set up a more structured reporting process, we are here to help. Our payroll solutions keep your team paid accurately and on time, while our broader SME accounting support covers everything from bookkeeping to year-end filing. Get in touch to find out how we can take the pressure off your next reporting cycle.

Frequently asked questions

What documents are included in statutory accounts for small UK businesses?

Statutory accounts typically feature a balance sheet, profit and loss account, and notes to the accounts. Small and micro-entities may omit cash flow statements and strategic reports from their filings.

How do I know if my business qualifies as micro or small for reporting?

Qualification depends on meeting at least two of three criteria: annual turnover, balance sheet total, and employee numbers. From April 2025, micro-entity thresholds rise to £1m turnover, £500k balance sheet, and 10 employees.

What is the deadline for filing statutory accounts?

Private limited companies must file statutory accounts within 9 months of year-end at Companies House. Missing this deadline triggers automatic financial penalties that increase the longer you delay.

Can I use financial reports for business management as well as compliance?

Absolutely. Robust financial reporting helps you track profitability and cash flow and supports strategic decision-making well beyond what statutory compliance alone requires.

No responses yet