Selecting the right accounting method shapes how your business records income, tracks expenses, and reports financial performance to HMRC. Many UK SMEs struggle to understand which approach suits their operations, leading to compliance risks and poor financial visibility. This guide walks you through the key considerations, preparation steps, and implementation process to help you choose and maintain an accounting method that supports both regulatory requirements and business growth in 2026.

Table of Contents

- Understanding The Accounting Method Options

- Preparing To Choose The Right Accounting Method

- How To Select And Implement Your Accounting Method

- Verifying And Maintaining Your Accounting Method

- How Concorde Company Solutions Can Support Your Accounting Method Choices

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Method choice impacts compliance | Cash basis and accrual accounting serve different business needs and statutory obligations. |

| Preparation requires business assessment | Evaluate turnover, industry requirements, and internal management needs before deciding. |

| Implementation follows structured steps | Select, configure systems, train staff, and document your chosen approach systematically. |

| Ongoing verification ensures accuracy | Regular reviews and updates maintain compliance as your business evolves. |

Understanding the accounting method options

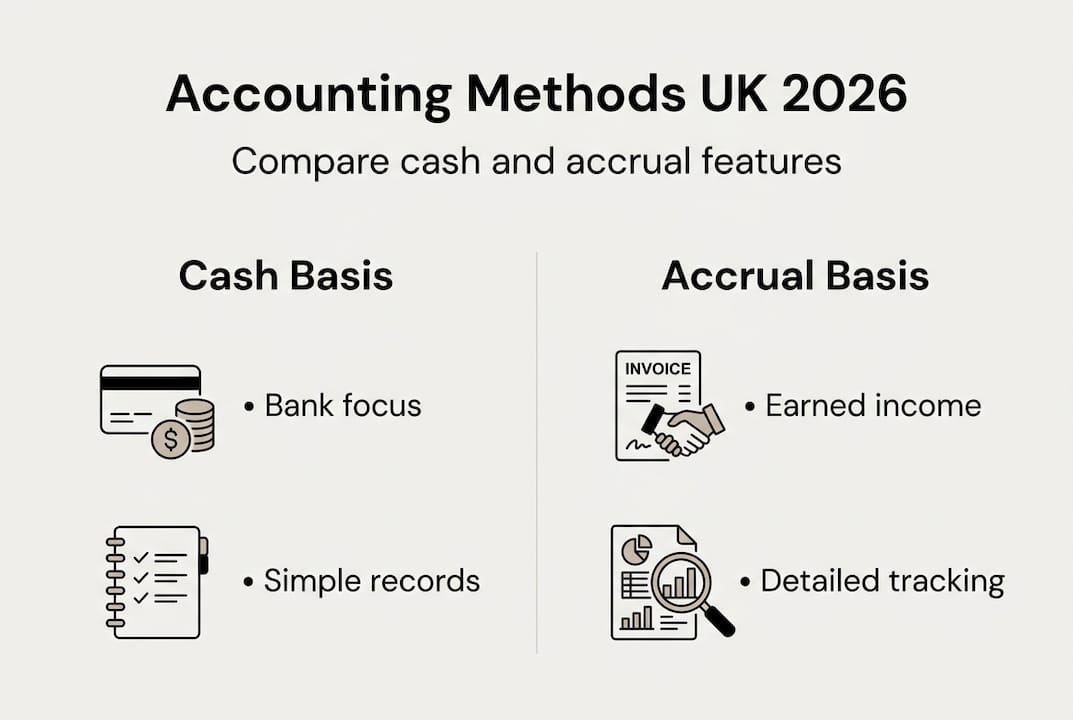

UK SMEs commonly choose between cash basis and accrual accounting, each with distinct advantages. Cash basis accounting records income when you receive payment and expenses when you make payment. This method tracks actual money movement through your business accounts.

Accrual accounting recognises income when you earn it and expenses when you incur them, regardless of when cash changes hands. You record sales when you issue invoices and purchases when you receive supplier bills, creating a more complete picture of business activity.

Cash basis accounting offers simplicity that appeals to many small businesses. You focus on bank transactions, making bookkeeping straightforward and cash flow management intuitive. However, eligibility limits restrict this method to businesses with turnover below £150,000, and it may not reflect true business performance when significant invoicing delays occur.

Accrual accounting provides accuracy that larger businesses require. This method complies with generally accepted accounting standards and gives stakeholders a realistic view of financial health. The complexity increases significantly, requiring more sophisticated bookkeeping and deeper financial knowledge.

Pro Tip: Review your customer payment terms and supplier arrangements before choosing a method, as these patterns significantly influence which approach works best.

| Feature | Cash Basis | Accrual Basis |

|---|---|---|

| Recording principle | Money received/paid | Income earned/expenses incurred |

| Complexity | Simple, bank-focused | Complex, requires tracking |

| Turnover limit | Under £150,000 | No limit |

| Financial accuracy | Limited during delays | Comprehensive view |

| Best suited for | Sole traders, micro businesses | Growing SMEs, limited companies |

Preparing to choose the right accounting method

Evaluate your annual turnover first, as this determines whether cash basis accounting remains available to you. Businesses exceeding £150,000 turnover must use accrual accounting, whilst those below this threshold can choose either method based on operational needs.

Consider your industry characteristics carefully. Service businesses with immediate payment often thrive with cash basis accounting. Manufacturing or wholesale operations with extended payment terms benefit from accrual accounting’s ability to match revenue with associated costs across reporting periods.

Check statutory obligations related to VAT registration, corporation tax submissions, and financial reporting deadlines. VAT-registered businesses typically require accrual accounting to track output and input tax accurately, whilst unregistered businesses enjoy more flexibility.

Assess your internal management needs for financial decision making. Growing businesses planning to seek investment or financing typically need accrual accounting to present accurate financial positions to lenders and investors. Stable operations focused purely on cash management may prefer the simplicity of cash basis.

Pro Tip: Consult with an accountant early to align your choice with compliance requirements and growth goals, preventing costly method changes later.

Document your business profile systematically:

- Current and projected annual turnover figures

- Industry sector and typical payment terms

- VAT registration status and threshold proximity

- Plans for growth, investment, or business structure changes

- Internal reporting needs for management decisions

- Staff capability for maintaining chosen accounting processes

Your preparation phase should also include reviewing bookkeeping best practices to understand the operational requirements of each method. This groundwork prevents misalignment between your chosen approach and practical implementation capacity.

How to select and implement your accounting method

Review your business profile against method characteristics systematically. Compare your documented turnover, payment terms, and reporting needs with the features and limitations of cash and accrual accounting outlined earlier.

Consult with an accountant or financial advisor to validate your choice. Professional guidance helps identify compliance issues you might overlook and ensures your selection aligns with HMRC expectations for your business type and size.

Adjust bookkeeping systems or software to align with your chosen method. Cash basis accounting requires simpler bank reconciliation features, whilst accrual accounting demands invoice tracking, aged debtor reports, and accrual journals. Configure your accounting software settings to match your selected approach.

Train staff or bookkeeping resources on specific accounting processes. A structured approach to selecting accounting methods reduces errors and improves financial clarity. Everyone handling financial records must understand when to record transactions and how to categorise them correctly.

Monitor ongoing accuracy and compliance with periodic reviews. Schedule monthly reconciliations to catch discrepancies early and quarterly reviews to assess whether your chosen method still serves business needs effectively.

Pro Tip: Maintain clear documentation of the method chosen for audits and HMRC submissions, including the date of adoption and reasons for selection.

| Step | Purpose | Expected Outcome |

|---|---|---|

| Profile review | Match business characteristics to method requirements | Clear understanding of suitable options |

| Professional consultation | Validate choice against regulations | Confirmed compliance and strategic fit |

| System configuration | Align software with recording principles | Accurate transaction capture |

| Staff training | Build capability for consistent application | Reduced errors and improved data quality |

| Periodic monitoring | Ensure ongoing accuracy and relevance | Maintained compliance and informed decisions |

Implementing effective bookkeeping tips during this transition ensures your new accounting method delivers expected benefits from day one. Take time to test processes with sample transactions before processing actual business data.

Verifying and maintaining your accounting method

Schedule periodic financial reviews to check for discrepancies or compliance gaps. Monthly bank reconciliations catch recording errors quickly, whilst quarterly management accounts reveal whether your method provides useful decision-making information.

Stay updated on changing tax laws and reporting deadlines relevant to your chosen accounting method. HMRC periodically adjusts thresholds, allowances, and submission requirements that may affect how you apply cash or accrual principles.

Ensure bookkeeping accuracy by cross-referencing bank statements with ledgers regularly. Cash basis accounting requires matching every bank transaction to a corresponding entry, whilst accrual accounting demands reconciling invoice records with payment receipts.

Regularly reviewing financial reports supports compliance and timely tax submissions, preventing penalties and maintaining good standing with HMRC.

Timely submissions to HMRC avoid penalties and interest charges that erode profitability. Mark key deadlines for self-assessment, corporation tax, and VAT returns in your business calendar, allowing sufficient time for year-end adjustments.

Adjust your accounting method if business size or operations change significantly. Crossing the £150,000 turnover threshold requires switching from cash to accrual basis, whilst incorporating your business or registering for VAT may necessitate method changes.

Common mistakes to avoid when maintaining accounting methods:

- Mixing cash and accrual principles within the same accounting period

- Failing to update software settings after changing methods

- Recording personal transactions in business accounts

- Neglecting to reconcile accounts monthly

- Missing HMRC notification requirements when switching methods

- Assuming last year’s approach automatically applies to current circumstances

Maintaining accurate bookkeeping for UK SMEs requires consistent application of your chosen method and prompt correction of any deviations. Set reminders for key review dates and establish clear procedures for handling unusual transactions.

How Concorde Company Solutions can support your accounting method choices

Choosing between cash and accrual accounting affects every aspect of your financial management. Concorde Company Solutions offers expert guidance tailored to UK small and medium businesses on accounting methods, helping you navigate HMRC requirements whilst supporting business growth.

Benefit from personalised consultation that aligns accounting choices with both compliance obligations and strategic goals. Our team assesses your specific business profile, industry requirements, and growth plans to recommend the most suitable approach. We handle the technical configuration and staff training needed for smooth implementation.

Access resources including bookkeeping best practices to maintain accurate financial management throughout the year. Reach out to streamline your accounting processes and ensure peace of mind in 2026.

FAQ

What is the best accounting method for small businesses in the UK?

The best method depends on your specific business circumstances, including turnover, industry, and payment terms. Cash basis accounting suits sole traders and micro businesses with straightforward transactions and turnover below £150,000. Accrual accounting better serves growing SMEs needing accurate financial reporting for stakeholders or planning to seek investment. Consultation with an accountant helps identify which approach aligns with your compliance obligations and business goals.

Can I switch my accounting method after choosing one?

Switching accounting methods is possible but subject to HMRC rules and approval requirements. You must notify HMRC when changing methods and may need to make transitional adjustments to prevent double-counting or omitting transactions. The switch typically occurs at the start of a new accounting period to maintain clear records. Early consultation with a tax professional ensures you follow correct procedures and understand the implications for your tax calculations and reporting obligations.

What records do I need to keep for my chosen accounting method?

Cash basis accounting requires records of all money received and payments made, including bank statements, receipts, and payment confirmations. Accrual accounting demands more comprehensive documentation, including sales invoices, purchase invoices, credit notes, and accrual journals showing income earned and expenses incurred regardless of payment timing. All records must be kept for at least six years from the end of the accounting period they relate to, supporting audit trails and HMRC enquiries. Digital record-keeping through accounting software simplifies retention and retrieval.

How does choosing the correct accounting method affect my tax filings?

Accounting methods determine when income and expenses are recognised, influencing tax calculations and timing. Cash basis calculates taxable profit on actual cash movements, potentially deferring tax on unpaid invoices. Accrual method recognises profit when transactions occur, regardless of payment status, providing a more accurate but sometimes less cash-friendly tax position. Incorrect method choice can cause cash flow issues when tax bills arrive before receiving payment from customers, or compliance risks if you use an ineligible method for your business size and structure.

No responses yet